Banks are essential to the functioning of an economy: they act as intermediaries, connecting savers and borrowers. Put simply, banks accept deposits from their customers, which are immediately available and risk-free (1) and use them to extend riskier, longer-term loans to borrowers. And they do all of this on a leveraged basis.

Therefore, banks create liquidity in an economy and finance all economic sectors. For this very reason, when banks become more restrictive due to monetary policy transmission mechanisms, the economy begins to run at half speed. And that is what is currently happening in Chile: with higher interest rates and weak economic growth, banks are becoming more selective, so they are granting fewer loans, resulting in lower investment and consumption, which in turn leads to weaker production and growth.

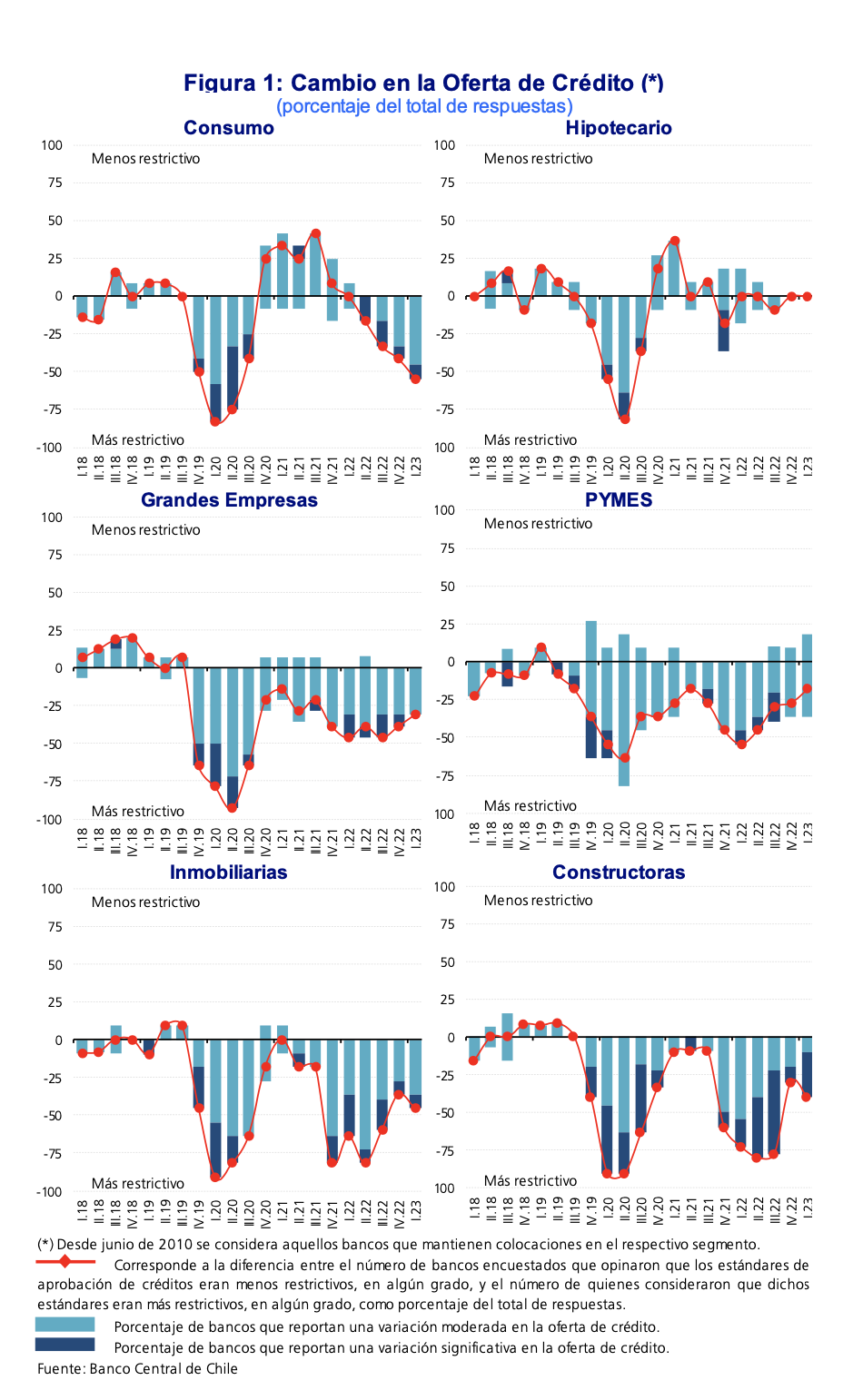

According to the Bank Credit Survey for the first quarter of 2023 conducted by the Central Bank of Chile, banks are becoming more selective when providing financing:

“In the first quarter of 2023, credit standards for the consumer loan portfolio became more restrictive, and once again, no changes were observed in the housing segment. For consumer loans, the share of banks reporting stricter conditions rose from 42% to 55%, and no institution reported more favorable conditions. Meanwhile, for housing loans, for the second consecutive quarter, none of the surveyed banks reported changes in their lending standards.”

“Credit supply conditions remain tight for large firms and, to a lesser extent, for SMEs. The share of institutions reporting stricter lending standards for large firms decreased slightly from 39% to 31%. Meanwhile, for SMEs, the proportion of banks that reported having more flexible standards increased from 9% to 18%—notably, these are institutions with a significant market share in the segment—while the proportion of banks reporting more restrictive standards remained at 36%.”

Meanwhile, loan approval standards for construction and real estate companies reversed some of the easing in credit restrictions observed in the previous quarter. Thus, for the first group of companies, the proportion of institutions reporting tighter credit conditions rose from 30% to 40%, while for real estate firms, it increased from 36% to 46%.”

It is precisely at times like these that private debt extended by non-bank financial institutions becomes more attractive. They serve as a source of credit for high-quality companies that currently do not have access to traditional banking services. Consequently, there are greater investment opportunities in this underserved market, and it leads to market efficiencies, as companies are able to secure financing for their projects, while private debt investors gain access to very attractive risk-adjusted returns that allow them to diversify their portfolios.

If you're interested in this financing strategy, we invite you to learn more about our Investment Fund FYNSA Private Fixed Income II, which has delivered stable and positive returns since its inception.

Vicente Dourthé

Fynsa AGF Private Debt Team