This year marks a special milestone for the fields of finance and financial derivatives: the iconic Black-Scholes financial model turns 50. You may have heard of it in college, at work, or perhaps because a friend mentioned it to you. Over the course of this past half-century, this model has transformed the entire industry and paved the way for countless professionals and academics. We invite you to learn about the legacy that continues to shape our world today.

How did the Black-Scholes model come about?

In 1973, Fischer Black and Myron Scholes introduced their paper “The Pricing of Options and Corporate Liabilities” to the financial world , revolutionizing the financial sector of the 1970s. The scholars’ work introduced a mathematical model that would make it possible to calculate the fair price of call and put options. Years later, the financial economist Robert Merton would expand this model to include other derivative products.

What impact did it have on finance as we know it today?

This model has been important for various reasons, but primarily because of the expansion and development of the options and derivatives market, where it allows for the management and transfer of various risks, such as exchange rates, interest rates, and commodity prices, among others. When considering large corporations, the topic of derivatives is always important.

By enabling the valuation of options with a solid fundamental basis, it has been of great help to companies in terms of financial innovation, increased liquidity, and other areas.

A simple example:

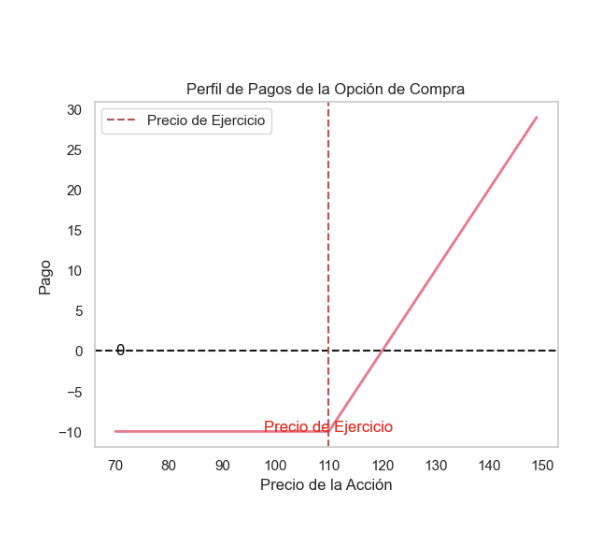

Imagine you own a company that imports technology in Chile, and your main business is selling cell phones. You don’t want to worry about the price at which you’ll have to buy the phones in the future, as this could affect your revenue and the stability of your business. To protect yourself against potential price fluctuations, you decide to purchase a European call option that allows you to buy a specific number of phones at an exercise price of $110 per unit on a specific date within the next year—say, exactly one year from now. At this point, certain questions arise, but this is also where the Black-Scholes model shines.

Let’s assume that the risk-free interest rate is 3% (for example, the yield on a one-year Chilean government bond) and annual volatility is 25%. The risk-free rate represents the return we could earn by investing in a risk-free asset, while volatility represents the variability in the stock price over time. Both factors are essential for calculating the fair value of a European call option using the Black-Scholes model.

By using it, we can calculate the fair price of the European call option. For example, if the model indicates that the option price is $10, this means that we should be willing to pay up to $10 per unit to acquire the right to buy the phones for $110 each in one year.

A year later, if the price of the phones rises to $130 per unit, we could exercise the call option and purchase the phones for $110. Although our goal was to protect ourselves against price fluctuations, we actually made a profit—in this case, $20 per unit ($130 – $110)—minus the $10 we paid, leaving us with a net profit of $10 per unit.

Now, let’s suppose the price of the phones drops to $90 per unit. In this case, we would not exercise the call option, since it wouldn’t make sense to buy the phones at $110 when the market price is $90. In this scenario, we would indeed incur a loss, but we would have the peace of mind that it would be limited to the $10 premium we paid. This is one of the advantages of using call options: our losses are limited to the premium paid, while our potential gains are unlimited if the price of the underlying asset rises significantly.

All of this may seem very simple, but without the Black-Scholes model, it would be very different. Without this model:

The Black-Scholes model benefits us by providing a solid and widely accepted framework for valuing options, which facilitates informed decision-making and improves the efficiency of the options market. This allows you to focus on your core business of selling phones without worrying about fluctuations in the purchase price.

In conclusion, we can say that the Black-Scholes-Merton model has transformed the financial industry by enabling the accurate valuation of options and financial derivatives. It has been used by prominent investors and hedge fund managers, such as Warren Buffett, George Soros, and Paul Tudor Jones, to manage risk and generate profits in financial markets. The model has facilitated the expansion and development of the options and derivatives market, improving market efficiency and enabling informed decision-making in the financial world. Its widespread acceptance in the financial industry has made it an essential tool for risk management and profit generation.

Cristóbal Martínez, Alternative Assets Portfolio Manager at Fynsa AGF