Last week's Fed meeting revealed the high level of uncertainty facing policymakers in the wake of the banking crisis, and that recent developments are likely to result in tighter credit conditions for households and businesses and weigh on economic activity, hiring, and inflation. Read more.

It will take time for the economic impact of a potential tightening of bank lending to be reflected in economic data. The Fed's H8 report (see here) will help us continue to track the trend in bank lending more frequently over the coming weeks.

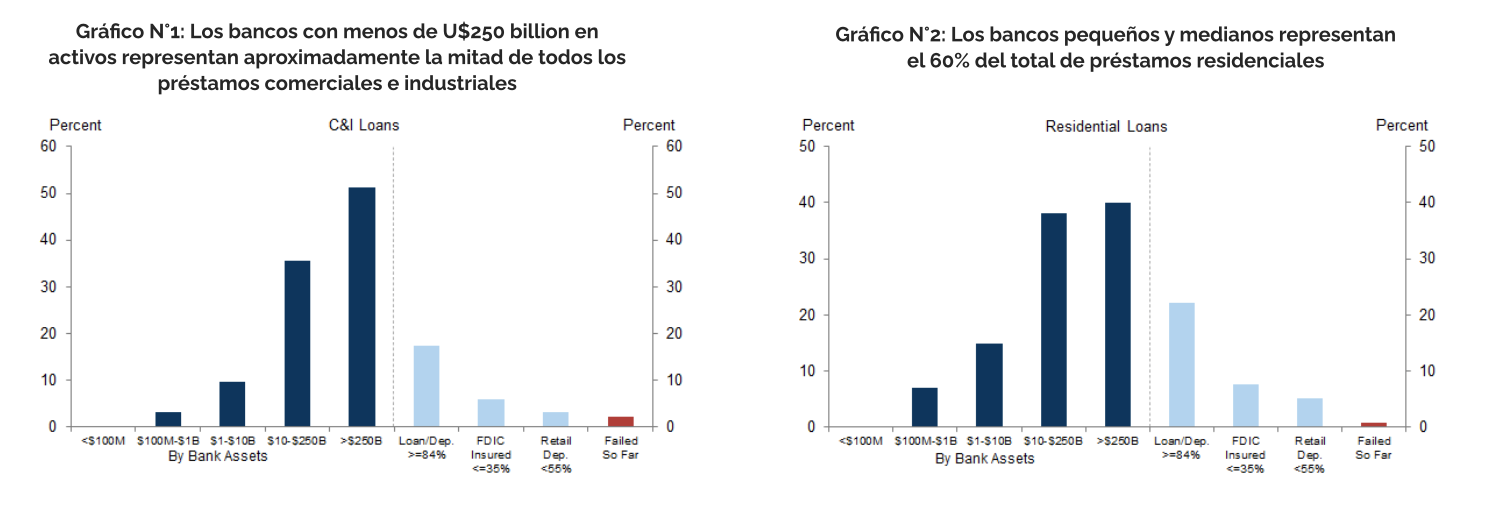

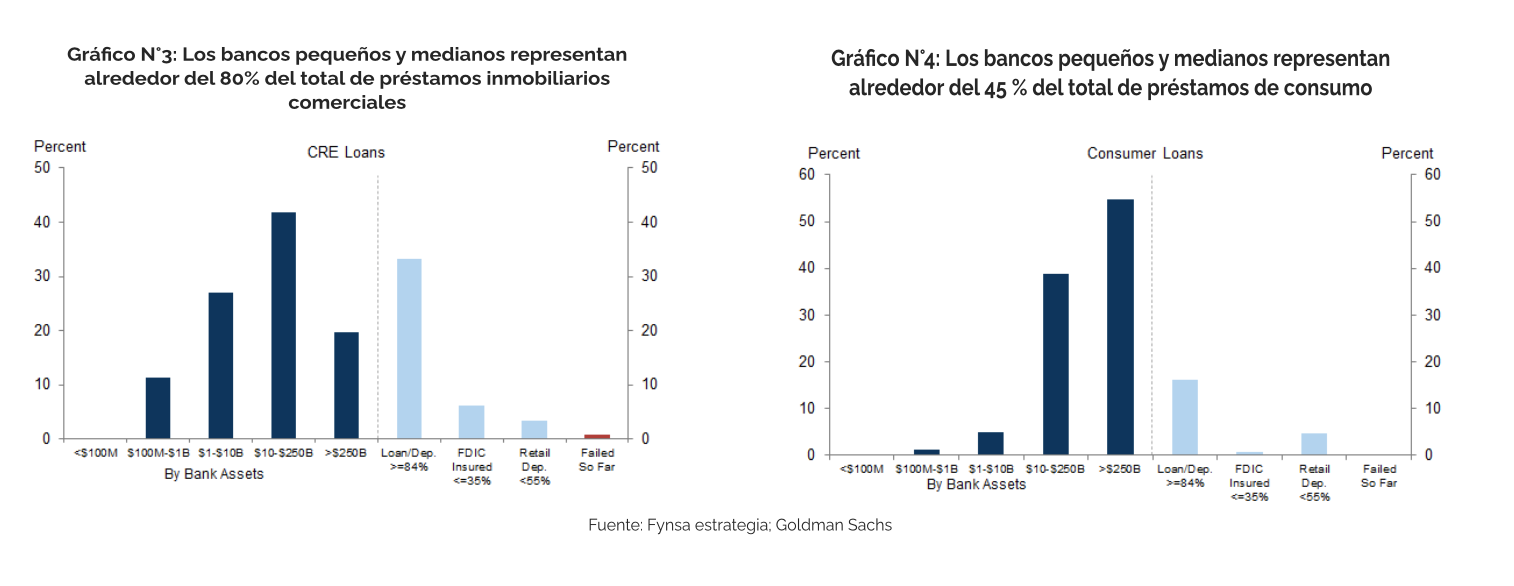

The risk going forward is that the uncertainty caused by deposit shifts will lead banks to become more cautious about lending. This risk is exacerbated by the fact that small and medium-sized banks play a very important role in U.S. bank lending (see Charts 1 through 4).

The bank lending channel is potentially a major obstacle to the economic outlook.

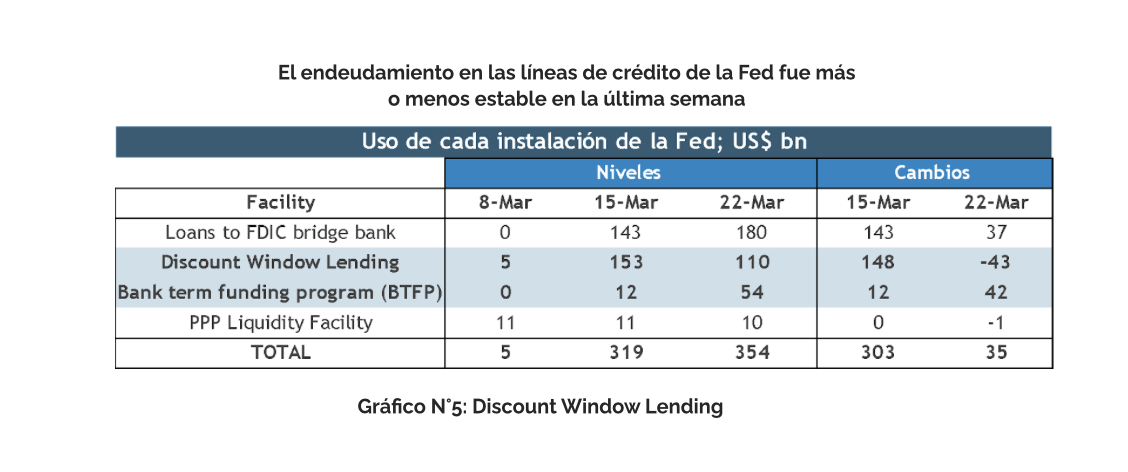

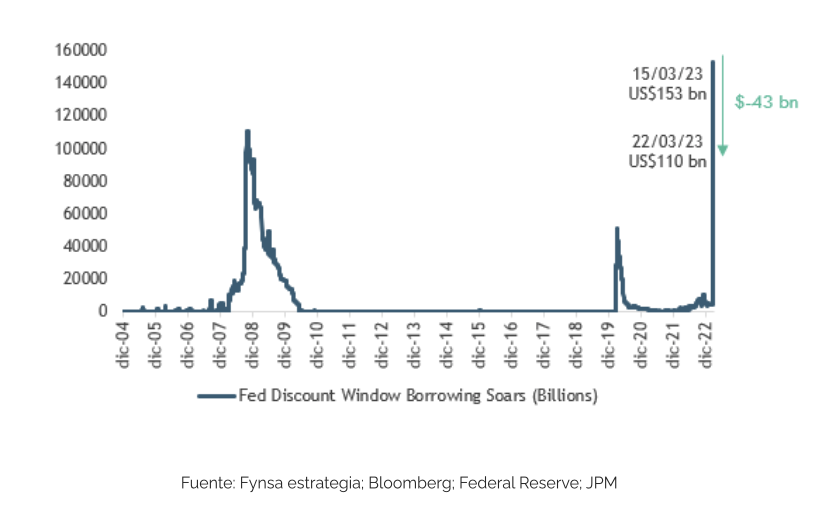

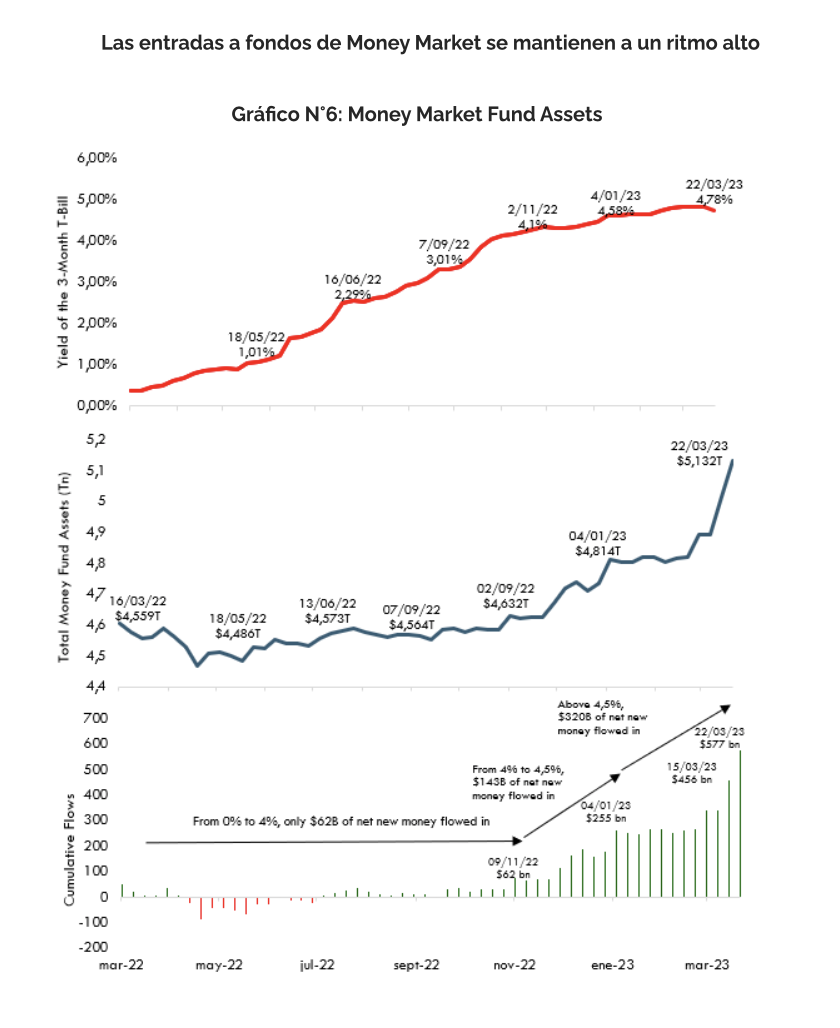

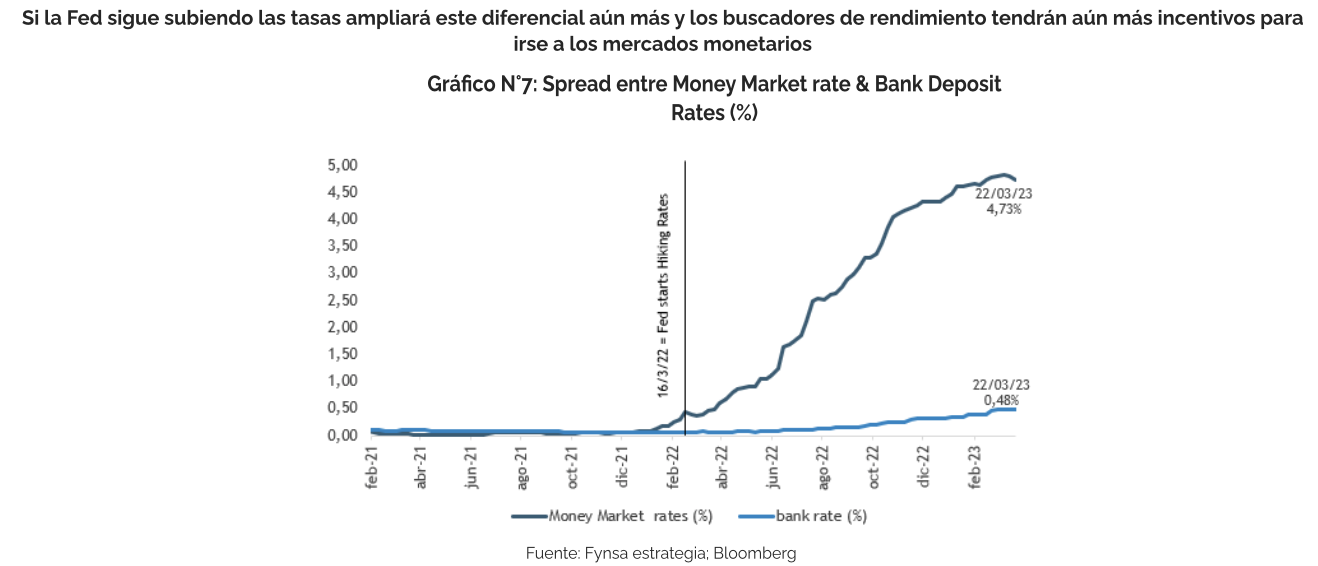

The banking liquidity crisis appears to be easing, but it may be far from over.Although the Fed’s latest H4.01 reportshowed a sharp slowdown in the pace at which U.S. banks are borrowing from Fed credit lines (see table below and Chart No. 5), banks seem to continue losing deposits to money market funds. In fact, money market assets grew by another $120 billion in the week ending March 22 (see Chart No. 6) , and, as we also noted last week, the Fed’s latest rate hike will likely make it even more difficult for U.S. banks to compete with the nearly 5% yield offered by money market funds(see Chart No. 7).

Even if a severe systemic shock is contained, tighter credit conditions on the part of banks are likely to pose a new obstacle to growth in the coming months, and while this disinflationary pressure from the banking system reduces (and potentially reverses) the need for monetary policymakers to slow the economy through rate hikes, there is still considerable uncertainty about just how large and widespread the drag on growth will be.

Consequently, the level of uncertainty caused by the banking crisis is leading us to adopt a more defensive stance in terms of asset allocation, and we reaffirm our recommendation to overweight fixed income in a balanced portfolio. You can find more details here.

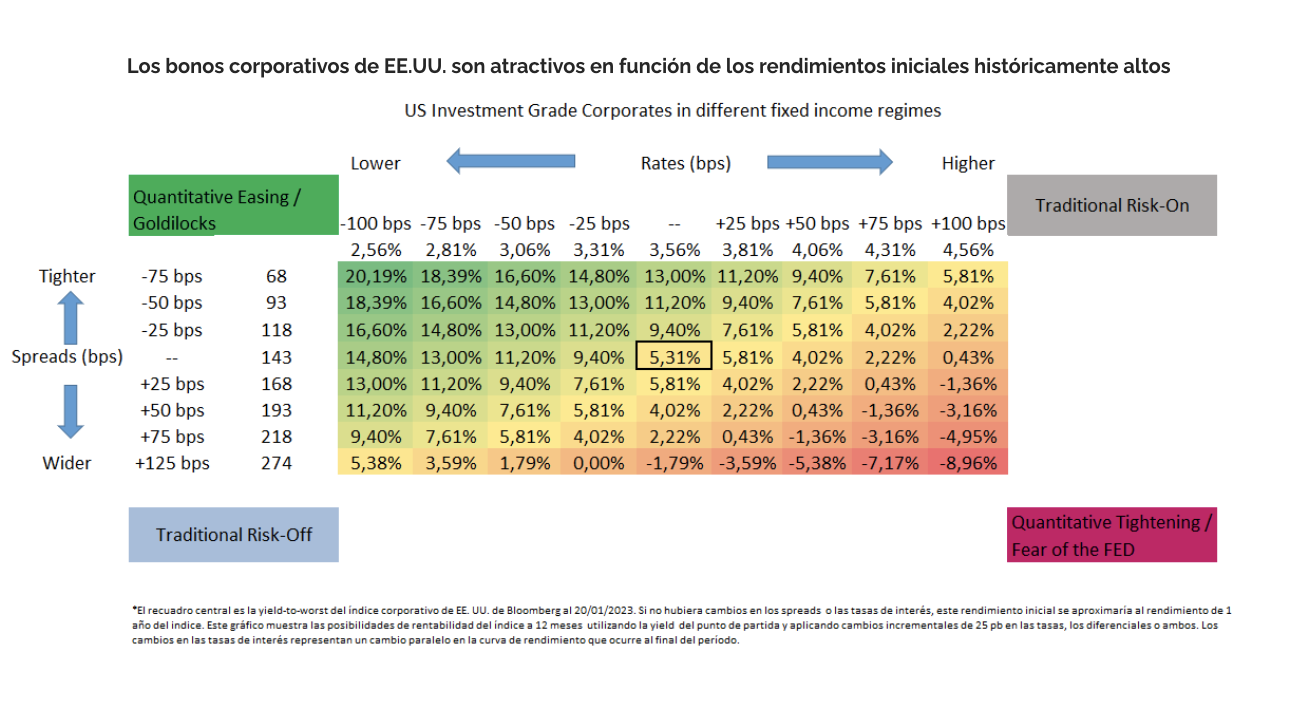

Specifically, in fixed income, we are focusing on high-quality assets—U.S. Treasuries, U.S. investment-grade corporate bonds—and a more neutral duration (around 4 years).