This week's monetary policy decision in the U.S. was particularly complex, given recent developments in the financial system and persistently high inflation.

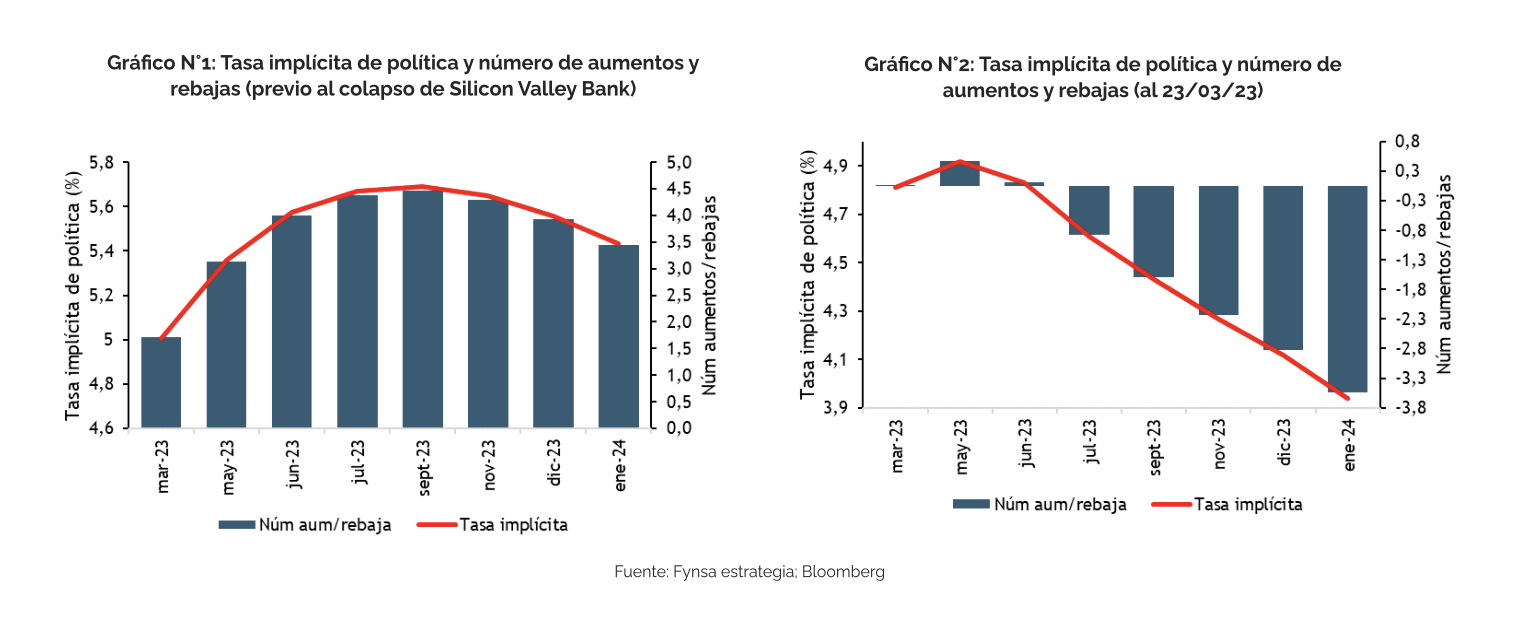

Keep in mind that, following a series of upward surprises in economic data throughout February, the market began to lean toward a more aggressive cycle of monetary tightening than previously priced in, to the point of pricing in up to 100 basis points more in federal funds rate hikes, bringing the rate to levels near 6%.

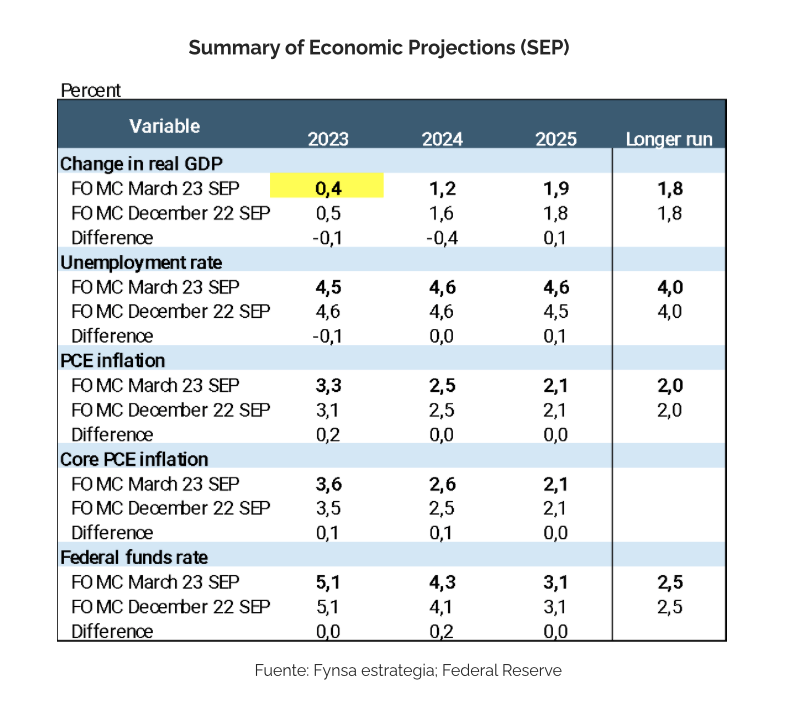

That said, things have changed dramatically since the collapse of Silicon Valley Bank and the subsequent liquidity crisis, including a record outflow of deposits from the system, which has caused the market to shift from pricing in an additional 100 basis points of rate hikes for this year to pricing in nearly 100 basis points of cuts. (See Charts 1 and 2.)

In this context, the Federal Reserve opted this week for a delicate balance by continuing to emphasize its commitment to a 2.0% inflation target, raising the federal funds rate by 25 basis points to a range of 4.75%–5.0%, but “toned down the language slightly” in its statement, shifting from “ongoing increases” to the less aggressive and less committed phrasing that “further policy tightening may be appropriate.”

With regard to the financial system, the statement notes that the “U.S. banking system is sound and resilient” and that recent developments are likely to result in tighter credit conditions for households and businesses and weigh on economic activity, hiring, and inflation. And at the press conference, when discussing the various bank rescue policies, Powell said that “these actions demonstrate that all depositors’ savings in the banking system are safe.”

This would seem to suggest that the authorities are willing to invoke the systemic risk exception whenever a bank fails. When asked to clarify his comment, Powell was terse and repeated that “depositors should assume that their deposits are safe.” Powell also noted that “deposit flows in the banking system have stabilized over the past week.” Given that the Fed has a more up-to-date view of bank balance sheets than the public does, this was encouraging news.

With regard to the economic projections (see table below), there are signs of a potential further rate hike before the Fed enters “pause mode,” after which the next move will most likely be a rate cut, in our view. Although Powell himself dismissed expectations of a rate cut, the poor growth outlook projected for this year (+0.4%)—which practically “implies a potential recession”—leads us to believe that rate cuts are likely this year.

A growing debate regarding monetary policy centers on whether the mandates to control inflation and maintain financial stability can be addressed differently and separately.

In this regard, Powell endorsed the idea of separating financial stability from monetary policy tools, albeit with limitations. When asked if he was concerned that a rate hike might exacerbate the problem at banks, he said that the decision on rates was “focused on macroeconomic outcomes” and that the situation at banks would be addressed through their credit lines. That said, it is difficult to separate these issues, and the statement also notes that recent developments in the banking sector are likely to “result in tighter credit conditions.”

In our view, the two objectives are closely linked: Higher monetary policy rates increase banks’ funding costs and reduce demand for loans, thereby lowering bank profits and tightening financial conditions, which in turn cools economic activity and, ultimately, inflation. It is highly likely that the buildup of financial tensions will require the Fed to be much more cautious about future monetary tightening.

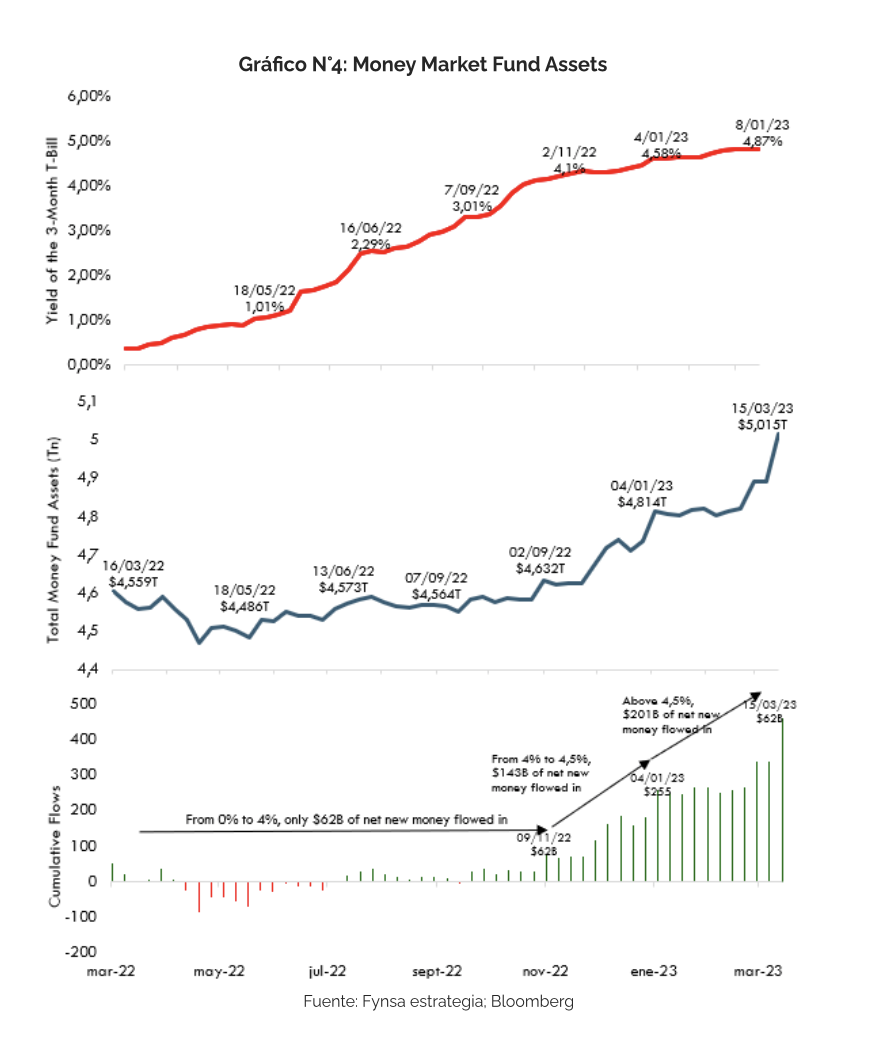

Furthermore, higher interest rates have contributed to financial stress by eroding banks’ deposit bases: U.S. depositors are moving their money out of banks and into money market funds to take advantage of the higher rates. Recent bank failures may have accelerated these outflows, risking a credit crunch that could trigger a recession and deflation. If the Fed’s high funds rate is the ultimate cause of the current financial stress, then the easiest solution is for the Fed to stop raising rates and start cutting them.

“A central bank’s credibility also depends on doing what makes the most sense for the economy, depending on the circumstances.”

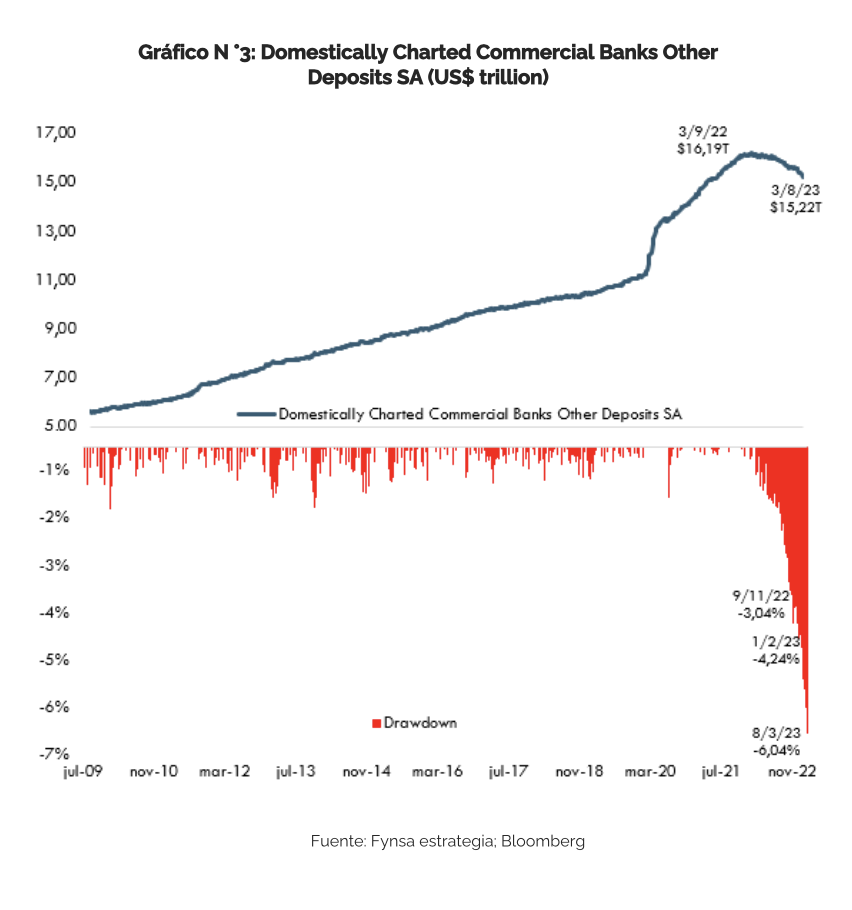

Chart No. 3 is taken from the Fed H8 report. It is updated with the latest data available as of March 8, two days before Silicon Valley Bank failed. What has been the largest deposit outflow since the financial crisis? The weeks leading up to the bank failures of recent weeks.

So why was there a massive outflow of deposits from banks prior to the bankruptcies? As shown in Figure 4, as rates rose from 0% to 4% between March and November 2022, inflows into money market mutual funds totaled US$62 billion. This changed when rates rose above 4%. US$ 143 bn flowed into money market funds as rates rose from 4% to 4.5%. Another US$ 201 bn flowed into money market funds as rates rose above 4.5%. Once again, the public’s attitude toward the movement of money changed when rates crossed the 4% threshold.

We invite you to review more details on how the banking liquidity crisis has unfolded in an update to the report published last week: The Collapse of Silicon Valley Bank: Causes and Consequences