In recent months, there have been several significant events in the financial world, such as the run on Silicon Valley Bank, the Federal Reserve’s intervention that led to the closure of Signature Bank, and UBS’s acquisition of Credit Suisse, among others. These events have raised greater concerns about the solvency of banks and have cast doubt on the effectiveness of current banking regulations.

In this context, the expansion of the asset threshold for banks subject to the Dodd-Frank Act has been criticized. This law regulates banks with more than USD$50,000 million in assets, requiring them to meet higher capital requirements, annual stress tests, and other measures aimed at improving financial stability.

In 2018, this limit was raised to USD$250,000 million, with the justification that it would promote competition between large and small banks and stimulate economic growth, since stricter regulations could limit the amount of credit that banks can offer.

However, banks are not the only institutions that provide loans in an economy. Therefore, this decline in the supply of credit in an economy could be offset by other nonbank financial institutions.

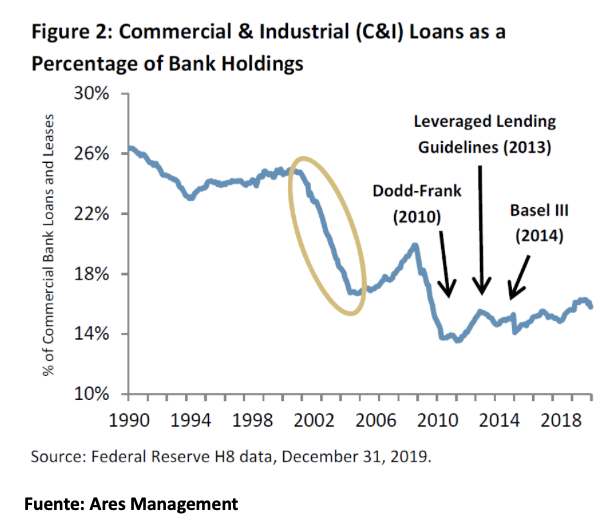

The following chart shows U.S. banks' exposure to commercial and industrial (C&I) loans since 1980.

These loans are used by many companies, especially small and medium-sized ones, because they do not have the same advantage as large companies in terms of accessing the financial market for financing. There are two main declines.

First, the consolidation phase of commercial banks that began in the late 1990s, during which regional banks engaged in mergers and acquisitions, affecting the loans they made to small and medium-sized enterprises. This occurred because commercial banks grew in size, giving them both the capacity and a preference for extending large loans to larger companies.

Second, the banking regulations established after the Great Recession, which include the the Dodd-Frank Act, guidelines for leveraged loans, and Basel III. These three regulations further restricted the growth of bank credit in the United States.

Given the current state of the banking sector and its importance to the economy, there has been discussion about the need for stricter regulation of smaller banks. According to the Financial Times, the Fed is considering imposing stricter regulations on medium-sized banks. Although this could lead to a credit crunch and a slowdown in economic activity, it also opens up opportunities in the private debt market.

While it is not the only factor driving the growth of the private debt industry, stricter regulation of mid-sized banks in the United States could limit private companies’ access to bank credit, which could benefit nonbank financial institutions that provide private debt, since they are not subject to the same regulations.

Vicente Dourthé Orrego – Private Debt Team, Fynsa AGF