Saving and investing may seem like a complex task to many (even investment professionals). However, following a simple, yet well thought-out strategy can help you make good financial decisions and build long-term wealth, following a simple but well-thought-out strategy can help you make good financial decisions and build long-term wealth.

In this article, we will explore in detail how I believe you should not only invest your own money, but also manage your personal finances, starting with financial security and moving toward maximizing your long-term returns.starting with financial security and moving toward maximizing your returns over the long term.

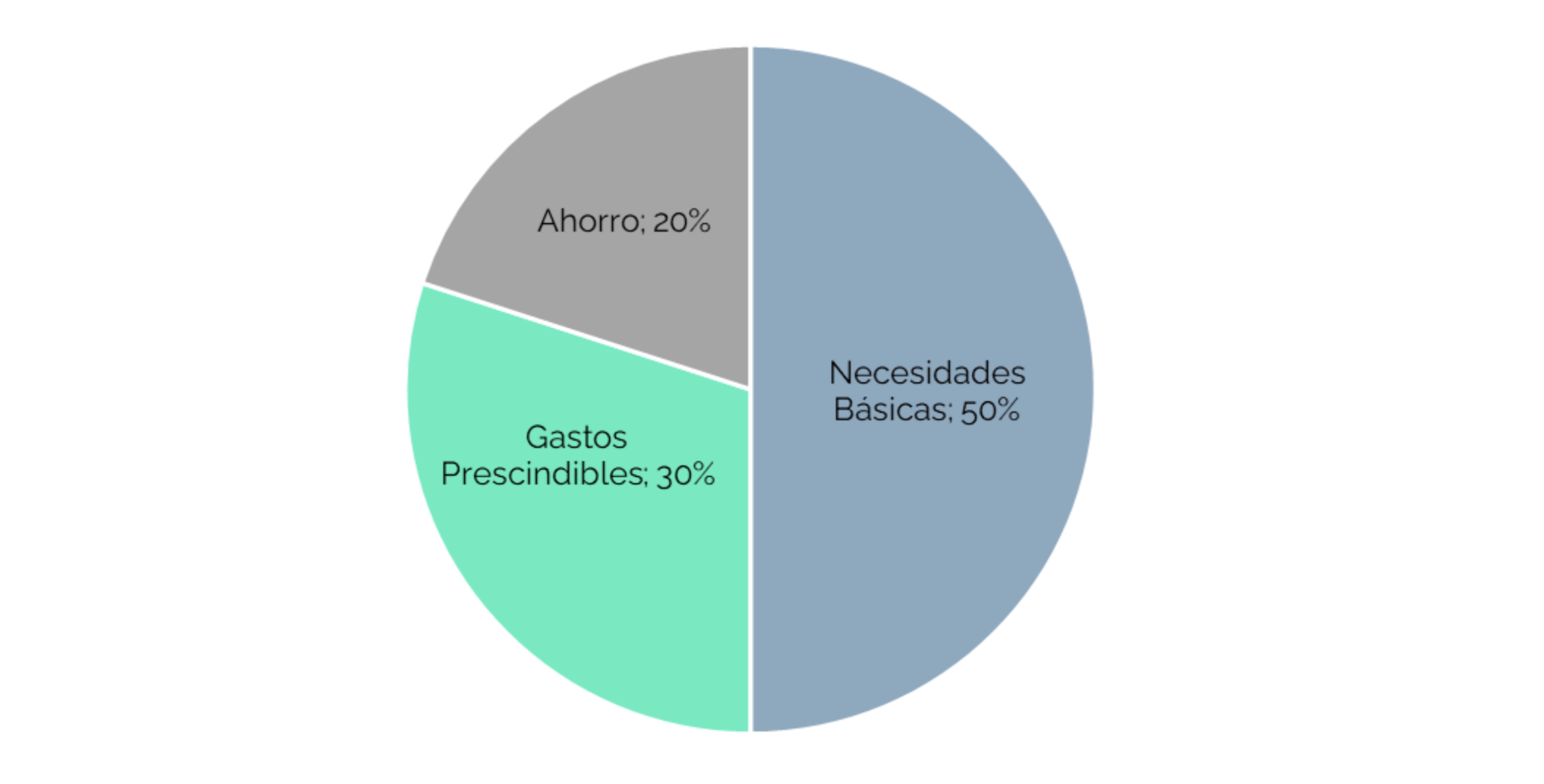

Before you start investing, the first thing you need to focus on is saving. It sounds easier than you think, but there are several methods that can help you achieve this goal. Personally, I follow a well-known rule in the world of personal finance: the famous 50-30-20 rule. It's an easy way to manage your money, which consists of dividing your net income you receive each month into three groups: 50% of your income for basic needs, 30% for expendable expenses such as going out to eat, and finally, the remaining 20% for savings.

Following this rule allows you to organize your money easily, since each month you will be able to each month you will have in mind the amount you want to save and thus balance your expenses to reach your savings goal, no matter how much your income is.regardless of how much your income is.

Once you're already saving and starting to accumulate resources, you need to think about your first investment objective. From my perspective - and this is something that is generally agreed upon in the world of investment advisors - your first investment objective should be an emergency fund, which can cover at least 3 to 6 months of expenses. your first investment objective should be an emergency fund, which can cover at least 3 to 6 months of basic expenses, including housing, food, basic utilities, and other necessities.including housing, food, utilities and other expenses that you consider essential in your day-to-day life.

This first investment objective serves two main purposes. The first is to provide peace of mind and financial security in case of unforeseen events, such as loss of employment or unexpected medical expenses. And the second, to have a "cushion" to fall back on when you want to spend a more significant amount on something specific, without having to go out and liquidate your other investments which should be longer term and may be more volatile (note, if you draw from this "cushion", your number 1 priority after this should be to refinance the emergency fund).

Although this is an "emergency" fund, this does not mean that it should be sitting in your current account waiting for an emergency to arise, especially in an environment of high inflation and high interest rates as in recent years, where very low risk investments, such as time deposits, reached yield levels above 10% per annum and inflation continues to be an issue. In my opinion, this fund should be invested in a type of instrument that is low risk, liquid and protects you from inflation. In my particular case, this is a Local Fixed Income fund that has a significant exposure to the UF, low credit risk, with a limited duration of less than 3 years, that is cheap and that allows you to have liquidity quickly.

Now that you have your emergency fund established and invested, it is time to address any high-interest debts you may have, such as credit cards or consumer loans. These debts can represent a significant burden on your finances and can diminish your ability to save because of the high interest payments that accumulate over the long term, so it would be desirable to avoid them or, if you already have them, to pay them off as soon as possible.

With your emergency fund established and your debts in order, you will feel more relaxed and secure, so you can start thinking about an investment portfolio. you can start thinking about an investment portfolio.

The first thing to consider when designing your portfolio is your investment horizon and your risk tolerance, so knowing what you are investing for and having self-knowledge is key at this early stage. For example, if you are young, as I am, and you are investing for retirement, you can afford to take on more risk to try to achieve higher returns. But if you are investing for shorter-term goals, for example, a vacation or a car, you may want to adopt a more conservative strategy.

According to theory - and for many in practice - a key characteristic of a well thought-out portfolio is that it should be diversified. That is, investing in a variety of asset classes such as currencies, stocks, bonds, real estate, alternative assets and an increasingly long etc., with the aim of reducing risk and maximizing long-term returns.

Today, diversification is easier than ever before. The mutual fund industry and local investment funds or ETFs (Exchange-Traded Funds) have made it much easier to diversify, The process of investing and allocating resources in specific instruments within the same asset class can be delegated to professionals, who can "buy" a single asset (fund share or ETF) that best represents or replicates the movement of an entire market.

Once you have defined your diversified investment strategy, it is important to regularly review and adjust your portfolio according to market conditions, your objectives and your financial situation. Rebalancing and adding to your portfolio periodically allows you to maintain an appropriate asset allocation and take advantage of investment opportunities that may arise, as well as to ensure that your investment strategy remains in line with your investment objectives, whether they are short, medium or long term.

Investing regularly and effectively involves following a scale of priorities that ensures your financial security in the short term, while maximizing your returns in the longer term. By establishing an emergency fund, eliminating expensive debt, getting to know yourself and having a diversified portfolio in line with your goals (that you review regularly) you will be well on your way. Remember, this is an ongoing process, in which you must always be willing to learn and adapt as your personal circumstances and the market environment change. At least that's how I, an investment professional, do it in my own personal finances.

Gabriel Méndez C.

Portfolio Manager Financial Funds, Fynsa AGF