We are starting a new year, a period in which both individuals and companies reflect on their next steps. It is common to dedicate this time to future planning, but it is just as crucial to look back, as it is a fundamental pillar of planning. In this context, as you explore the future outlook for private debt, we urge you to examine your track record, especially over the past year.

Before looking into the behavior of private debt, it is important to clarify the basis on which private debt investment is based. So, what is private debt? What is private debt?

Private debt emerged as a response to the financial crisis a response to the financial crisis, a period in which large banks, in search of greater stability, reduced their leverage and reduced the availability of financing. This restructuring of resources and the implementation of new restrictions on access to liquidity created a gap in the market that was not being filled. As a result, private debt emerged as a solution to cover these needs, offering alternative financing channels through investment funds.

Since its inception, private debt has operated mainly in low interest rate environments, especially during the period of reactivation of the U.S. economy, during which they were reduced to levels close to 0% (0% to 0.25%). However, in recent years, specifically since March 2022, when the U.S. Federal Reserve announced the first rate hike since the recovery period, private debt has been exposed to new circumstances.

Given this change, it is essential to review the current state of this market and analyze how private debt has reacted over the past year.

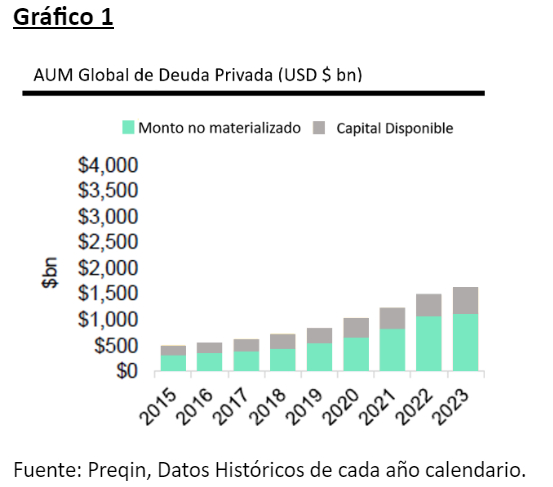

A major uncertainty that accompanied private debt during 2022 and 2023 was its ability to survive and yield during a period of high rates. However, since this increase, assets under management in this type of strategy have increased and reached USD $1.6 trillion, as can be seen in Graph N°1. This is mainly due to the growth factors that are driving the demand for alternative financing.

One of the factors that has driven the growth of private debt is the high entry barriers to access loans imposed by large banks, which have made it difficult for small and medium-size companies to access financing, as they have had to seek alternative ways of acquiring liquidity and, therefore, have increased the need for private debt. These have made it difficult for small and medium-sized companies to access financing, which have had to seek alternative ways of acquiring liquidity and, as a result, have increased the need for private debt.

Additionally, with the implementation of Basel 3, and its delimitation of an increase in banks' reserve requirements, the barriers to entry into this market have increased even more, This reinforces the need for private debt through an increase in demand for it, and also increases their participation in the capital market.

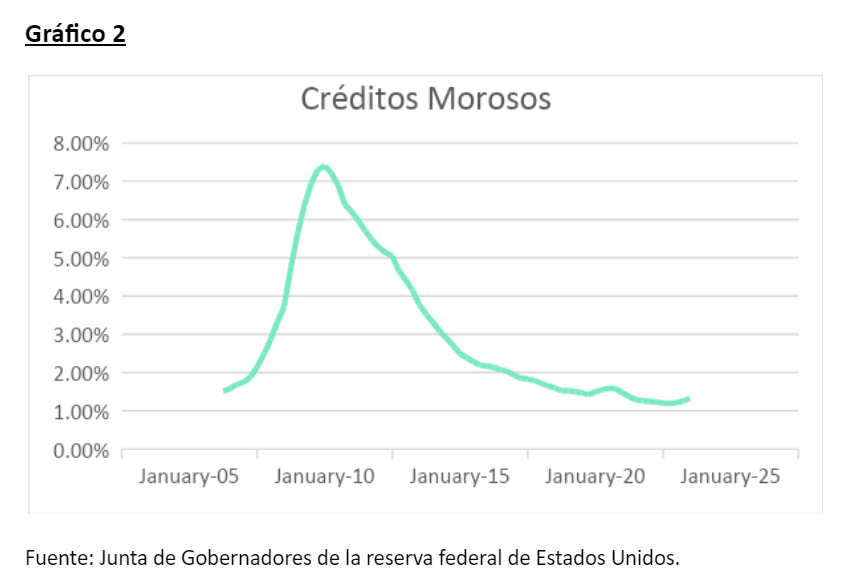

Finally, returning to the rise in rates, and the uncertainty that accompanies this event, especially with respect to debtors' ability to pay, it is important to emphasize that the percentage of non-performing debt has remained constant and declining, as can be seen in Graph 2, reaching levels of 1.32% in November, as reported by the board of governors of the U.S. Federal Reserve, thus demonstrating that borrowers are able to meet their obligations even in high inflation scenarios accompanied by high rates, giving greater security and support to private debt investors. borrowers are able to meet their obligations even in high inflation scenarios accompanied by high rates, providing greater security and support to private debt investors.

Despite its origins in a context of low interest rates, private debt has demonstrated a remarkable capacity for adaptation and resilience in the face of challenging financial conditions. This resilience has been driven by two crucial factors. First, the tight lending situation by banks has created an opportunity for private debt to fill the unmet gap. Second, difficulties in accessing traditional financing have led both companies and investors to turn to private debt as a viable and flexible alternative.

In summary, the persistence and success of private debt in challenging environments is not only due to its low rate beginnings, but also to its ability to fill the gaps left by the banking constraint and provide accessible and flexible alternatives in a constantly changing financial landscape.its ability to fill the gaps left by the banking crunch and provide accessible and flexible alternatives in an ever-changing financial landscape.

Martina Jauregui

International Funds Analyst Fynsa AGF