Following the release of the June CPI (which once again came in higher than expected), the U.S. yield curve has begun to price in a higher probability of a recession. While at the beginning of the year the markets primarily reflected inflation risk—as rising bond yields weighed on risk assets— over the past two months, investor concerns have shifted toward the risk of a recession.

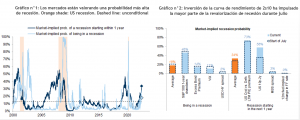

The probability implied by the market of a recession in the U.S. has risen so far in tandem with the sell-off in stocks, particularly in cyclical sectors. Equity and credit markets have traded largely sideways since early July, although the U.S. yield curve has led the rise in the implied probability of a recession. (See Charts No. 1 and No. 2)

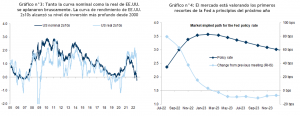

The slope of the U.S. U.S. 2s10s yield curve has reached its steepest investment-grade level since 2000 (see Chart No. 3). The Fed’s desire to “manage risk” around inflation has led the market to price in between 15% and 30% of a 100-basis-point hike at the next FOMC meeting (July 27), further deepening the inversion of the yield curve.

In addition, break-even inflation has continued to decline as the market’s inflation risk has faded (2-year break-even inflation rates are trading near 3.0%, after peaking at around 5% in late March), leading to a sharp flattening of the 2s10 real yield curve, which also points to a deeper price recession. However, the front end of the curve still implies a low probability of a recession: Federal funds futures are pricing in an overall increase in the policy rate over the next 12 months, which is not consistent with an imminent risk of recession; and rate futures indicate further hikes this year, but also expect the Fed to cut the policy rate in 2023 and 2024 (see Chart 4).

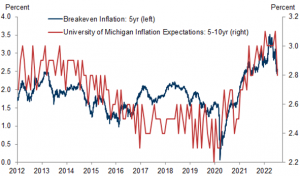

With next week’s Fed meeting in mind, we believe the decline in inflation expectations reduces the case for a 100-basis-point rate hike. 5- to 10-year inflation expectations were revised downward by 0.2 percentage points in the University of Michigan’s final June report and fell by 0.3 percentage points to 2.8% in the preliminary July report; 3-year inflation expectations in the New York Fed survey have declined by 0.3 percentage points since April, and market-based measures of inflation expectations have declined significantly, which should also alleviate concerns about the unanchoring of expectations. (See Figure 5.)

It is precisely this moderation in longer-term inflation expectations, a degree of stability in interest rates, and a 2Q22 corporate earnings season that has so far delivered slightly positive surprises that has driven the rally in equities in recent weeks (+8% from the mid-June lows).

A recurring question these days concerns the resilience of corporate earnings and how inconsistent it seems—given the rising risk of a recession— that the market continues to expect earnings growth of around 10% for S&P 500 companies.

The consensus expects earnings growth of around 6% year-over-year for the S&P 500 in Q2. While companies are likely to beat estimates, cautious commentary is expected to trigger downward revisions to future estimates. Concerns center mainly on margin pressures and the strength of the USD, although earnings weakness is still likely to be limited in the current slowdown, as nominal GDP remains positive (upper range support) and wage growth is lagging behind corporate pricing (margin support).

Based on our baseline scenario—assuming the economy avoids a recession (see HERE) —we expect the S&P 500 to rise to 4,400 points, assuming earnings of US$225 per share this year and single-digit growth next year in the range of US$240–US$245 per share (in line with consensus estimates).

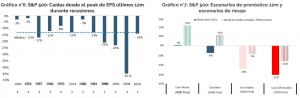

In a “moderate recession,” assuming an “average earnings contraction” would imply an expected EPS of US$200 per share, which would be consistent with our “full recession” scenario of 3,300 points for the S&P 500. (See Charts 6 and 7.)