The last time we wrote about the dollar was earlier this year, when it was 13% cheaper than it is today. Our bullish thesis was based primarily on the Federal Reserve being well ahead of other developed-market central banks in terms of monetary normalization (especially Europe), and that, as a result, interest rate differentials would shift even further in favor of the dollar. See HERE

It’s true, we’ve been surprised by the magnitude of the dollar’s appreciation (and that’s doubly true at the local level), but we must understand that the dollar’s upward trend has been feeding on itself event after event, from the war in Ukraine, the lockdowns in China, the higher-than-expected inflation figures in the U.S., and, more recently, fears of a recession, especially in Europe.

For educational purposes, I think it’s helpful to understand what we’re talking about when we refer to the dollar on a global scale, which is essentially the basket of currencies used to measure the U.S. Dollar Index (DXY Index)—the measure most commonly used on a daily basis, unlike other measures such as the Federal Reserve’s trade-weighted dollar index.

The U.S. Dollar Index is composed mainly of “hard currencies,” with the euro alone accounting for nearly 60% of the index, followed by the Japanese yen, with a weighting of about 14%, and the British pound, with 12%.

You can understand, then, that with a war in Europe and the ECB (European Central Bank) practically “stuck” in terms of policy (even though Europe has as much inflation as the U.S.), it’s no coincidence that the euro is “struggling” to reach parity with the dollar. The situation with the Japanese yen is also striking—a currency traditionally considered a “safe haven,” but one that has depreciated substantially against the dollar this year (-16%), against the backdrop of the Bank of Japan’s yield curve control monetary policy, which has, of course, widened interest rate differentials in favor of the dollar. (See Charts 1 and 2.)

Another very important factor to consider is liquidity. Keep in mind that the Fed is not only raising interest rates but also reducing its balance sheet—which is essentially withdrawing dollars from the market—and other developed-country central banks are doing the same. (See Charts 3 and 4.)

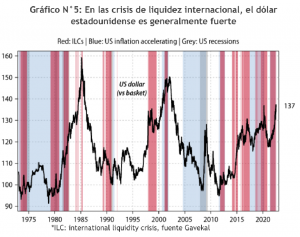

As a recent Gavekal report points out, what we may be facing is a liquidity crisis (see Figure 5). The U.S. dollar is the currency in which international loans are most easily obtained. If it is excessively easy and cheap to borrow in U.S. dollars over an extended period—that is, if real U.S. Treasury bill rates remain negative for a long time—foreign investors will take on heavy debt in U.S. dollars, effectively creating a massive short position in the U.S. currency.

And if foreign borrowers build up a massive short position in the U.S. dollar, something will eventually happen (for example, a sharp rise in oil prices) that will trigger a wave of short-covering. This will drive up the US dollar exchange rate, triggering even more short-covering.

Here’s what we’re seeing today: The current liquidity crisis is nothing more than an attempt to cover a historically large short position in the U.S. dollar. The result is a marked shift in the relative price of the U.S. dollar against the currencies of the rest of the world. This price adjustment has nothing to do with the fundamentals of the affected currencies and everything to do with market positioning, which in turn is the result of the ultra-loose policies pursued by the Fed and other central bankers over the past decade and beyond.

Recent developments, such as the larger-than-expected inflation readings in the U.S., which clear the way for the Fed to implement another 75-basis-point rate hike at its meeting later this month, and the inversion of the yield curve (increasing the risk of a recession), can only lead to a stronger dollar going forward, so the euro’s loss of parity may be only a matter of time.

This is significant because, as is often the case in such situations, a break below such key levels (sometimes referred to as “psychological” levels) tends to lead to increased volatility. Technically speaking, if the euro consistently falls below parity against the dollar, there are no major support levels until the 0.85–0.90 range, which could potentially translate into an additional 8% to 10% appreciation of the dollar, up to its highs at 120.

A reversal of this trend is only expected around Q4 2022 (unless, of course, the war in Ukraine ends), by which time inflation will likely have become less of a concern, thereby giving the Fed some room to maneuver to “recalibrate monetary policy.”

With regard to the dollar in Chile following the foreign exchange intervention announced by the central bank, some convergence with the performance of international benchmarks is to be expected. If the exchange rate were more in line with its benchmarks, the fair value should be closer to $900.