In prepared remarks at an event at the Economic Club of New York (SEE), Federal Reserve Chair Jerome Powell emphasized that recent data “show continued progress” toward the Federal Reserve’s dual mandate goals of maximum employment and price stability, and stressed that the FOMC “is proceeding with caution,” in light of “the uncertainties and risks, and how far we have come” in the tightening cycle.

On the economic front, the most notable change in Powell’s remarks comes when he states that “wage growth indicators show a gradual decline toward levels that would be consistent with 2% inflation over time.”

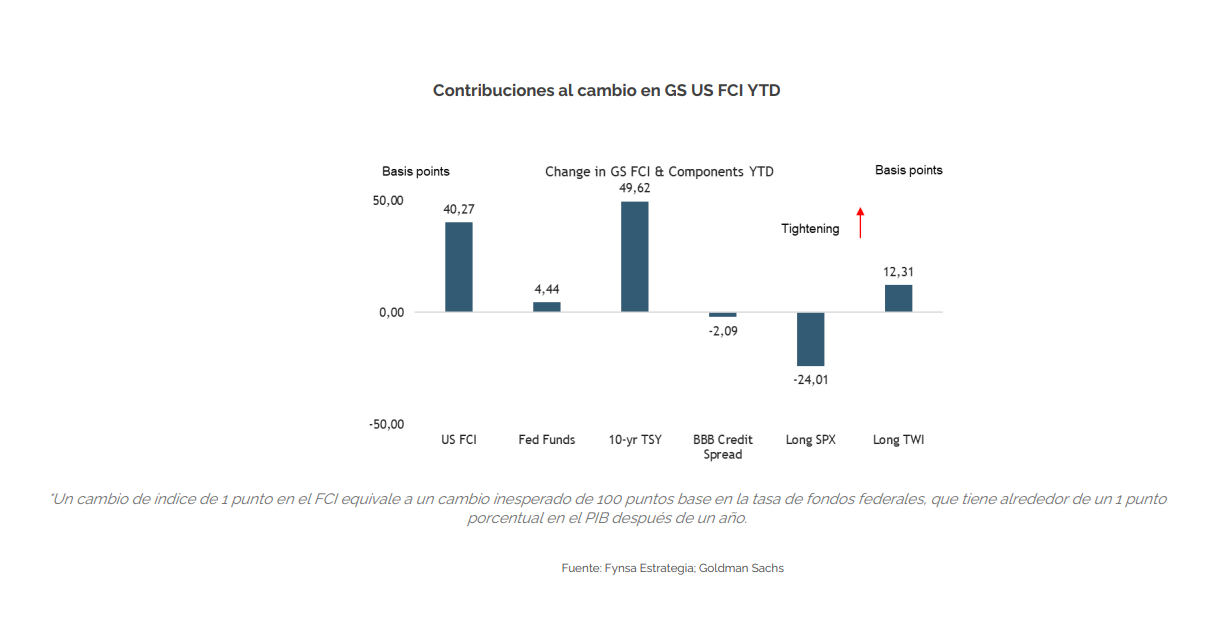

Regarding market conditions, during the question-and-answer session following the speech, Powell interpreted the recent rise in long-term yields as being primarily due to the term premium (a view we share: SEE MORE) rather than a shift in expectations regarding the path of short-term interest rates. As such, it represents a pure tightening of financial conditions not driven by an improvement in the economic outlook. Because of this, “at the margin,” the Federal Reserve may need to do less to tighten financial conditions (see charts).

Looking ahead, although Powell “kept open” the possibility of raising rates at subsequent meetings in light of further evidence of growth persistently above trend, or that labor market tightness is no longer easing, given that there will be little significant “further evidence” between now and the November 1 meeting, it appears that rates will remain unchanged after the next meeting.

This is also supported by recent comments not only from Chairman Powell, but also from other FOMC participants, including Vice Chair Jefferson and Presidents Williams, Barkin, Harker, Bostic, Daly, and Goolsbee, who have suggested that the FOMC was likely to leave the federal funds rate unchanged at its November meeting, and that the federal funds rate had likely peaked in this tightening cycle.

Finally, with the 10-year U.S. Treasury yield hovering around 5%, we reaffirm our belief that current interest rate levels are attractive by historical standards and recommend considering a gradual shift away from cash toward longer maturities and corporate bonds (SEE)