September is shaping up to be the worst month of the year for risky assets, but also for the bond market, amid renewed interest rate pressures, given the possibility that rates will remain higher for longer—due to fears that rising energy prices and a still-resilient economy will lead to more persistent inflation, keeping central banks in a restrictive stance. This trend has also been fueled by the growing supply of U.S. debt issued to finance large budget deficits.

As early as the beginning of August, we noted that Treasury bonds appeared poised to fall again, amid still-high long-term inflation expectations, which—combined with concerns over a potential downgrade of the U.S. credit rating by Fitch Ratings and a flood of Treasury bond sales to cover the federal deficit—could lead to a rise in term premiums. (SEE MORE)

The “still restrictive” tone set by the Federal Reserve last week has done little to help; despite keeping rates steady in the 5.25%–5.5% range, it has not ruled out another rate hike and, perhaps more importantly, that rates will remain high for longer than the markets had anticipated.

The widespread caution among central banks in developed markets—which remain reluctant to declare victory in their fight against inflation and are maintaining a restrictive stance—can be justified by the fact that they had to respond to an inflationary shock not seen in decades; therefore, it is necessary to carefully gauge confidence in the effectiveness of monetary policy after a long period of very low interest rates. Second, central banks’ caution in maintaining a restrictive stance also helps anchor inflation expectations. And third, excessive confidence and certainty that the tightening cycle has ended could lead to a premature easing of financial conditions, which could put inflation dynamics to the test.

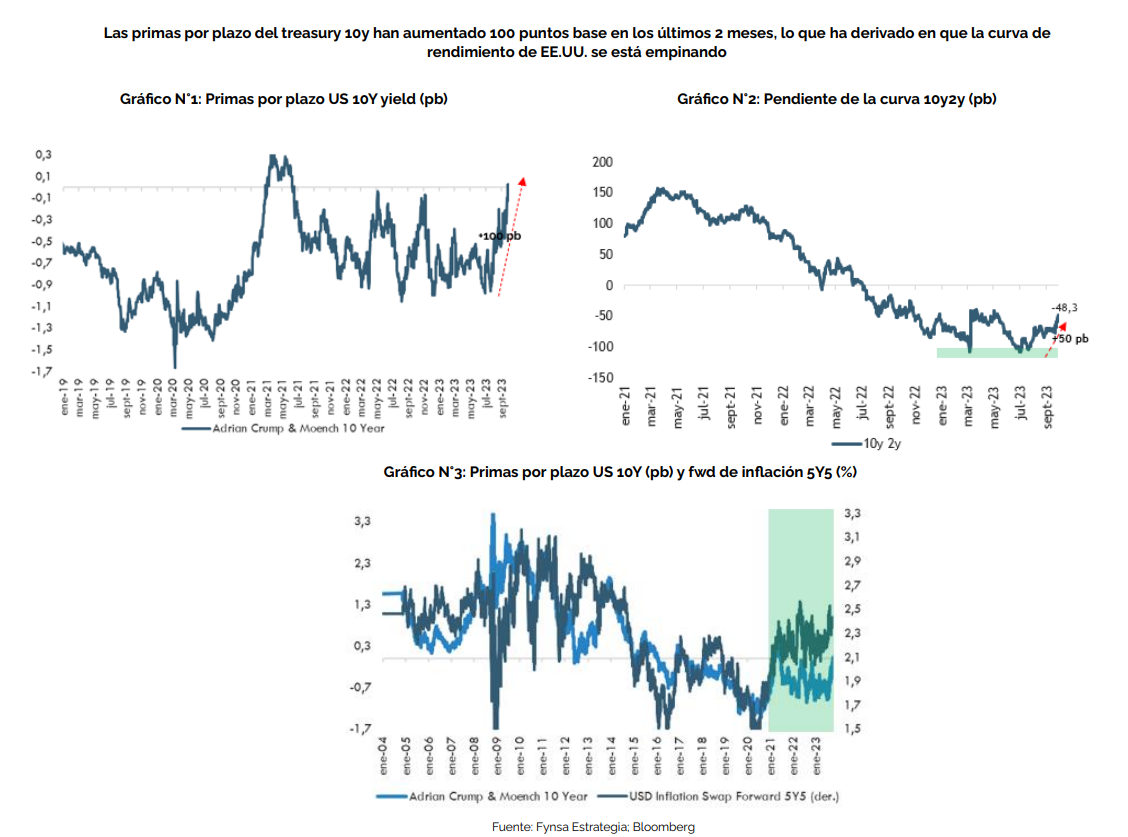

Recent concerns about U.S. federal debt may also be affecting U.S. Treasury bonds and driving up term premiums on long-term bonds. The term premium—a key measure of how much bond investors are compensated for holding long-term debt—turned positive for the first time since June 2021, highlighting the possibility that interest rates will remain higher for longer. (See Chart No. 1).

As a result, the U.S. yield curve is steepening (see chart No. 2) amid expectations that the Fed has nearly finished raising rates, with the 10-year Treasury yield surpassing 4.5% for the first time since 2007.

There could be a much simpler, though related, reason: an “adjustment” of interest rates to slightly more persistent long-term inflation expectations, as shown in Figure 3. That said, inflation expectations would have to “unanchor,” say around 2.5%, to justify higher compensation going forward.

That said, the general narrative from central banks suggests that they are pausing—or are close to doing so—based on a number of considerations. First, central banks in developed markets—with the exception of the Bank of Japan—have implemented between 400 bp and 550 bp of cumulative tightening since the start of the tightening cycle and now consider current levels to be sufficiently restrictive. Second, all central banks are aware of the long and uncertain lag in monetary policy transmission. Restrictive levels have reduced the need for further tightening unless data call into question the path of inflation’s return to target and/or that path appears too slow. Third, they believe that keeping rates higher for longer will eventually help bring inflation back to target.

In particular, in the case of the U.S., given the speed and magnitude of this rate-hiking cycle (+550 bp), which began in March 2022, and the natural lag in monetary policy—which should begin to be felt more strongly in economic activity data starting in Q4 2023—we expect the Fed’s current cycle of monetary tightening to be nearing its end.

Finally, after a 50-basis-point rise in the 10-year Treasury yield in September alone, To what extent are current long-term interest rate levels—or further increases from here on out—beginning to be justified?

Following the logic of the term premium, between 2004 and 2006—at a time when long-term yields were at a level similar to today’s—the term premium between 10-year and 2-year bonds averaged 40 basis points. If the term premium were to return to that level, the 10-year yield would approach 5%, although that would likely only happen if data continues to point to an improvement in the economy’s strength. Otherwise, a rate around 5% represents a “limited downside,” considering recent highs near 4.7%.

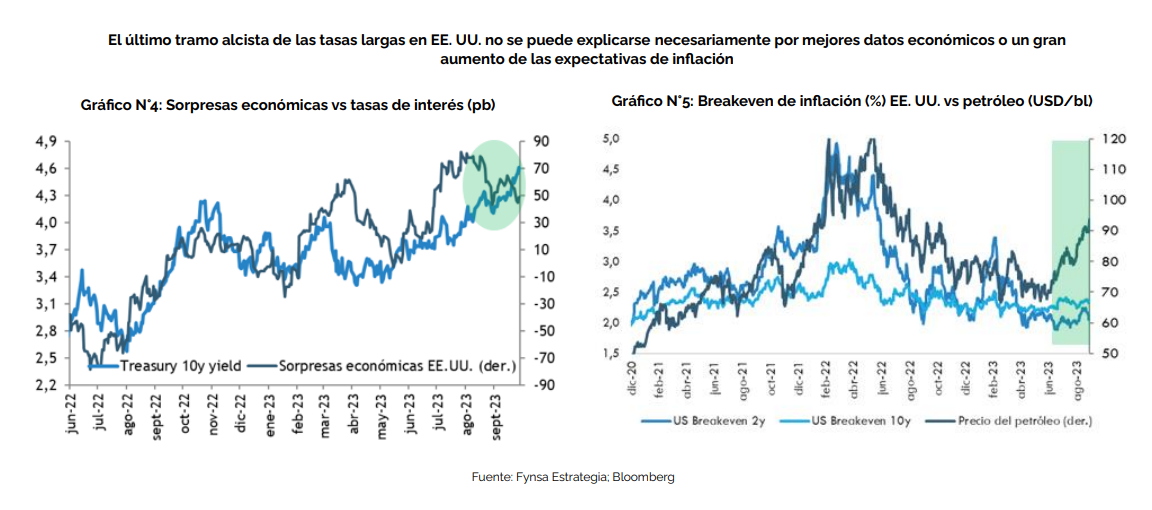

And as shown in Figure 4, long-term rates have continued to rise at a time when economic data has once again begun to come in below expectations in the U.S., and inflation expectations remain firmly anchored despite the sharp rise in oil prices in recent weeks (see Chart No. 5).

In our base-case scenario, we expect yields to moderate somewhat in the coming months and recommend gradually shifting from cash toward longer-term maturities and corporate bonds. We’ll delve deeper into that in a future post.