Until May 2023, an inverse correlation can be observed between real interest rates and the S&P 500 yield.

Since May 2023, this trend is broken, supported mainly by upward revisions to expected earnings.

Much of the rally in U.S. stocks since last October (almost 30% to recent highs for the S&P 500. (almost 30% to the recent highs of 5,300 points for the S&P 500,) can be explained by the expectation that the Federal Reserve can achieve a soft landing, i.e. an economy that is slowingThe Fed's expectations of a soft landing, i.e. an economy that is slowing as inflation slows, would give the Fed some leeway to cut interest rates.

U.S. companies are likely to pass the test of delivering 1Q24 results, but with inflation showing no further progress in 1Q24, a labor market that remains strong, and rising energy prices, given the backdrop of heightened geopolitical risks. We believe that risks have been leaning towards less monetary easing from the Fed, and that higher rates for longer put the logic of soft-landing at risk.

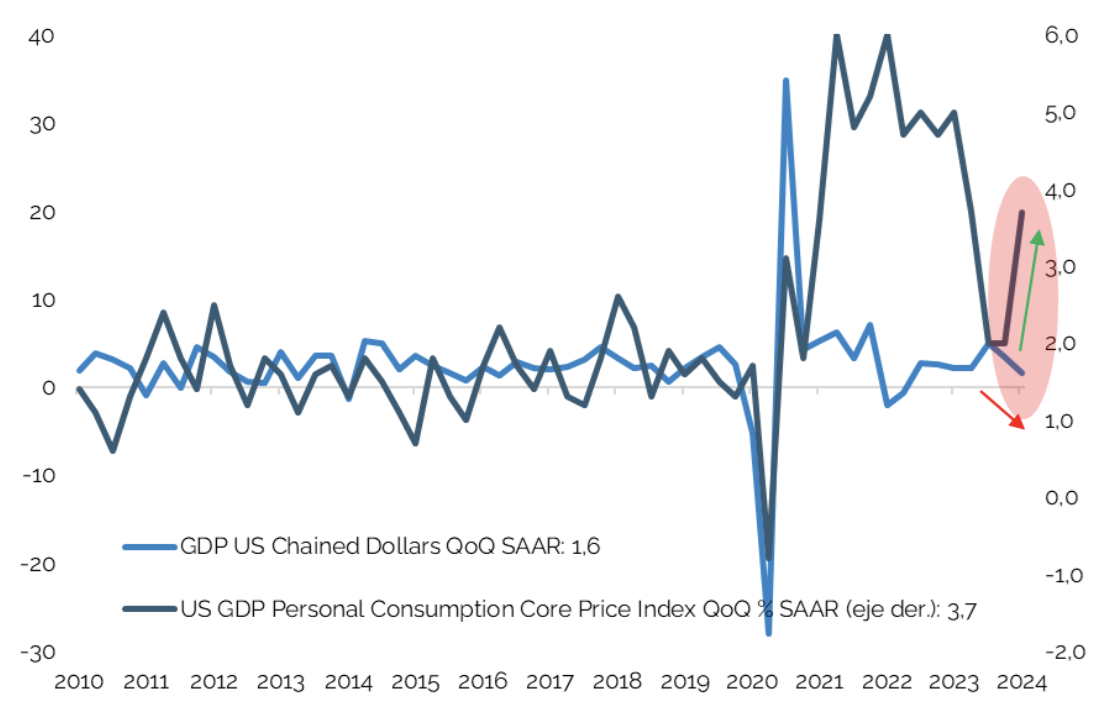

The most recent precedent that the economy and markets may face a more complex scenario going forward is found in the 1Q24 growth figures in the U.S., which showed a further slowdown in the economy and persistent inflationary pressures, which showed a further slowdown in the economy and persistent inflationary pressures.

Indeed, U.S. GDP grew at an annualized rate of 1.6%, below market expectations, which expected growth closer to 2.5% and well below 4Q23's 3.4%, while a measure of core inflation (PCE) rose at a rate of 3.7%, faster than expected and well above 4Q23's 2.0% as well.

1Q24 growth figures in the U.S., which showed a further slowdown in the economy and persistent inflationary pressures. Inflation?

Graph n°3: U.S. Real GDP and Core Inflation (PCE)

Source: Fynsa Strategy; Bloomberg

These latest economic data put an end to a period of strong demand and low price pressures, which is precisely what has fueled hopes for a soft landing.

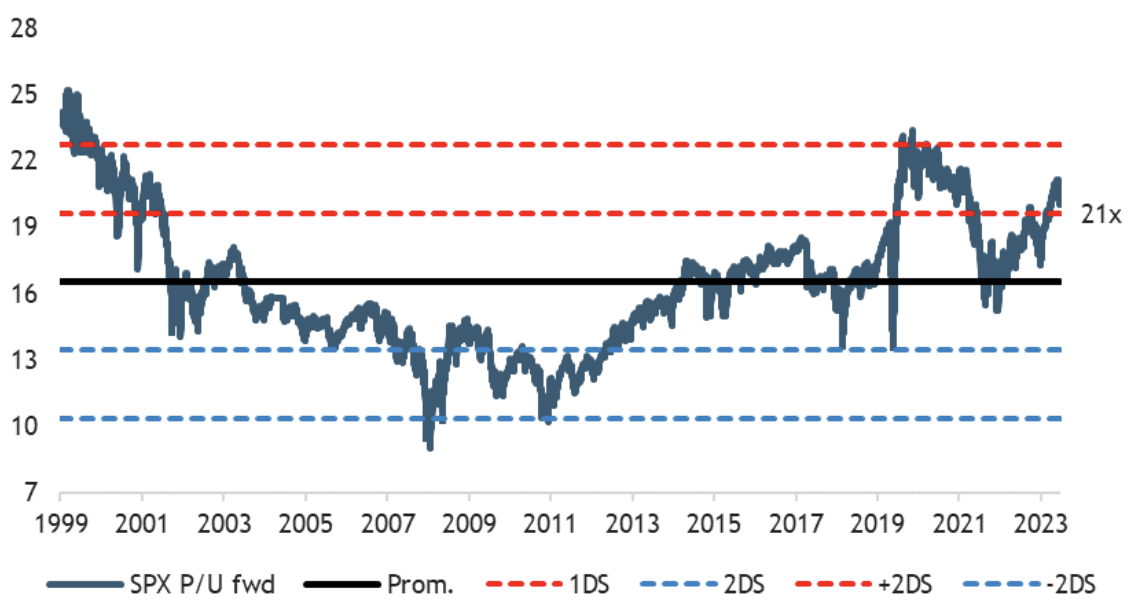

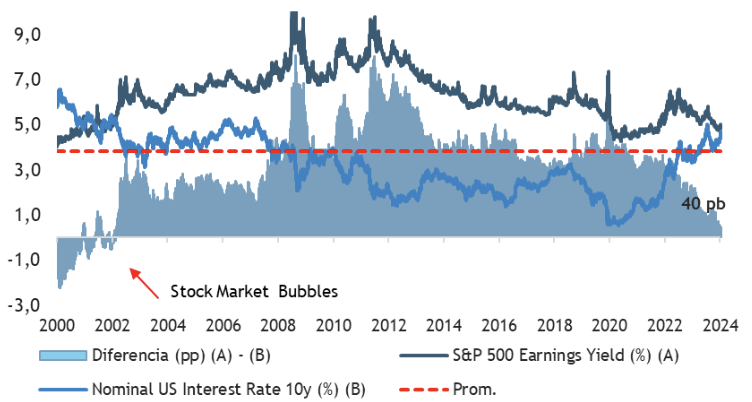

We continue to draw attention to the continued complacency in stock valuations.. The fact that inflation remains too high, further repricing by the Fed (today the market incorporates a single rate cut in 2024, down from 6 in late 2023) and a corporate earnings outlook that may be too optimistic, make it difficult to justify valuations that are at the high end by historical standards and that equities are offering only a 40 basis point premium over the risk-free rate.

Chart N°4: S&P 500. 12m P/U Multiple

Source: Fynsa Strategy; Bloomberg

Chart N°5: S&P 500. ERP

Source: Fynsa Strategy; Bloomberg

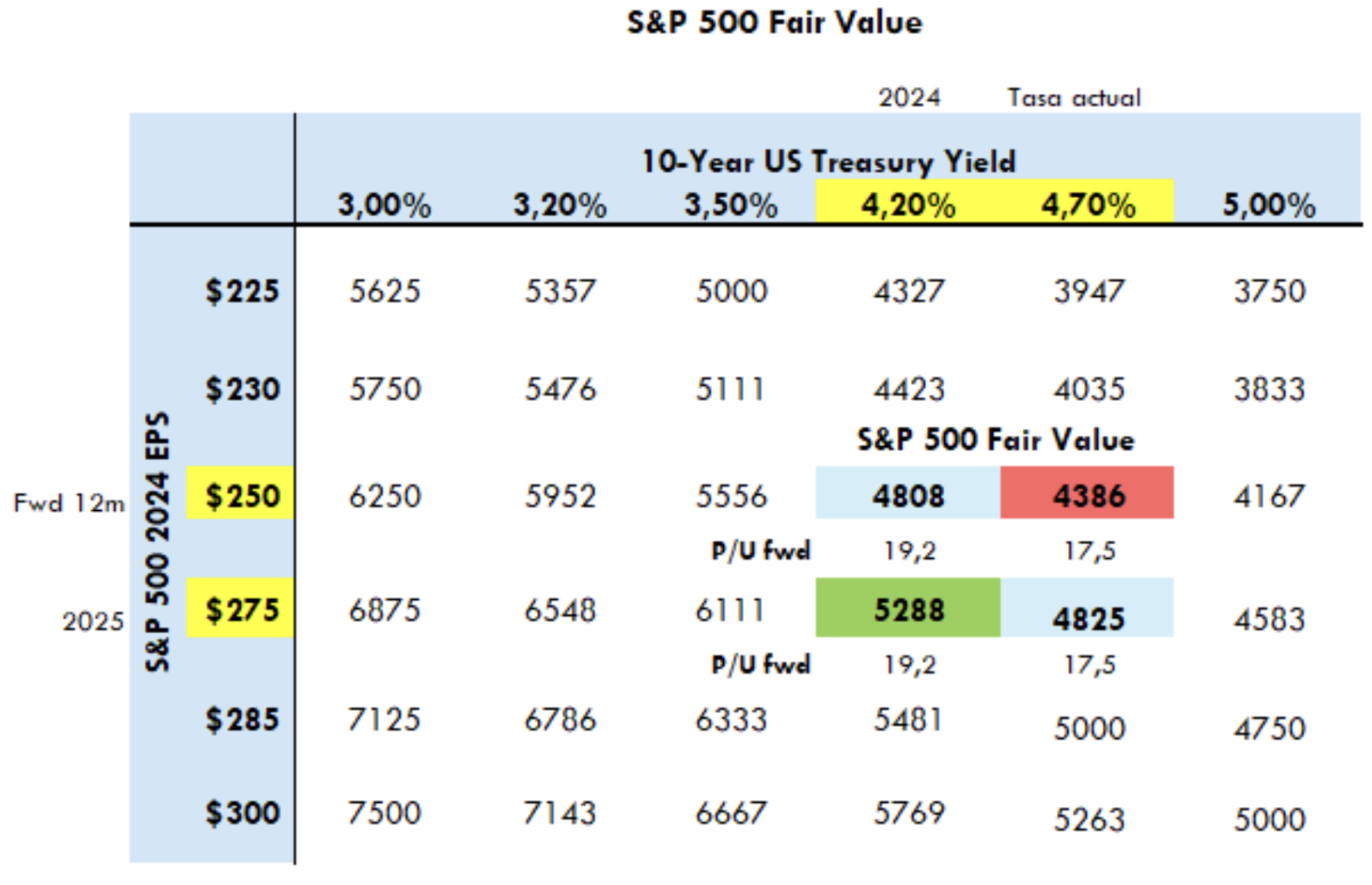

5,300 points, assuming a 10y treasury at 4.2%, an expected EPS of US$275 by 2025 and a risk premium of 100 basis points. If rate pressures remain, it is very likely to see levels closer to 4800 in the near term, while, in our pessimistic scenario, the S&P 500 could visit levels in the range of 4400-4500 points.

All in all, the current market narrative and patterns increasingly resemble the middle of last year, when upside surprises in inflation and aggressive Fed revisions prompted a correction in risk assets.

In this context, we suggest maintaining a more balanced global strategy to address the high concentration of the U.S. market and unattractive valuations, and increasing fixed income exposure, with historically attractive initial rate levels. SEE MORE