Agency MBS refers to the purchase of mortgage-backed securities issued by government-sponsored enterprises such as Fannie Mae, Freddie Mac, and Ginnie Mae.

How does this investment vehicle work in practice?

It is common for banks to sell a large percentage of their outstanding mortgages to participants in the secondary mortgage market, including institutional investors, private firms, and government and quasi-government entities. These participants purchase mortgages from banks and bundle them together—a process known as securitization—to create financial securities that can be sold on the market to investors.

Each pool constitutes a security known as a mortgage-backed security (MBS), which represents an interest in the pool of mortgages. Like bonds, MBS make coupon payments to investors. An agency MBS is an MBS issued by one of three quasi-governmental agencies: the Government National Mortgage Administration (GNMA, or Ginnie Mae), the Federal National Mortgage Association (FNMA, or Fannie Mae), and the Federal Home Loan Mortgage Corporation (Freddie Mac).

Now that we understand a little more about this asset class, we can ask ourselves a second question: Why is it attractive to invest in this type of asset today?

Yields on Agency MBS have risen as the Fed has raised rates. MBS offer investment-grade (IG) credit quality and a yield to maturity of around 5%, according to the Bloomberg MBS Index. The prepayment risk on Agency MBS has decreased because many homeowners refinanced their mortgages in 2020–2021 at lower interest rates. In fact, approximately 78% of the index has coupon rates below 3.5%, meaning these homeowners are less likely to prepay those mortgages, given that current mortgage interest rates exceed 6.9%.

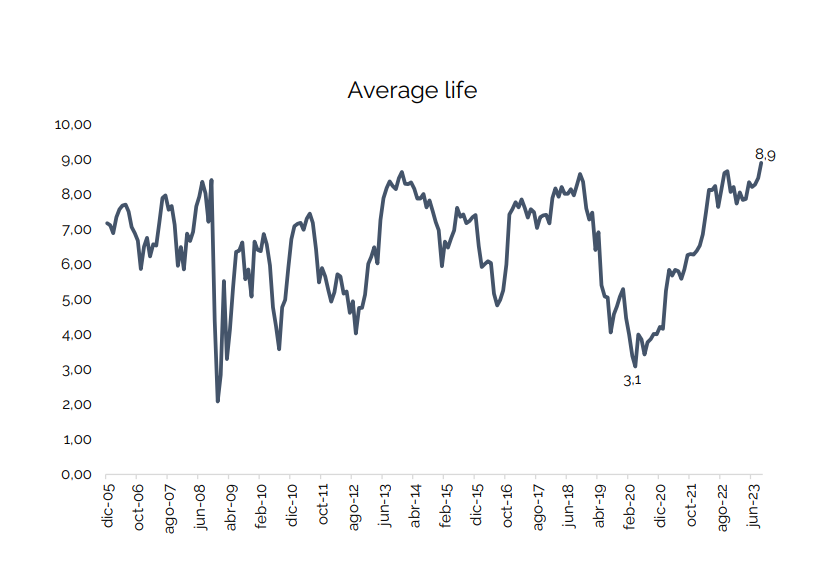

Under these conditions, MBS are likely to exhibit greater predictability in terms of cash flows. In this environment of higher interest rates, homeowners with lower rates are less likely to refinance and pay off their mortgages. Consequently, prepayment estimates are reduced, and the bonds remain outstanding longer at higher yields. With longer average maturities, the average duration of the Bloomberg MBS Index has extended to 8.9 years as of September 2023 from a low of 3.1 years in April 2020 (see chart).

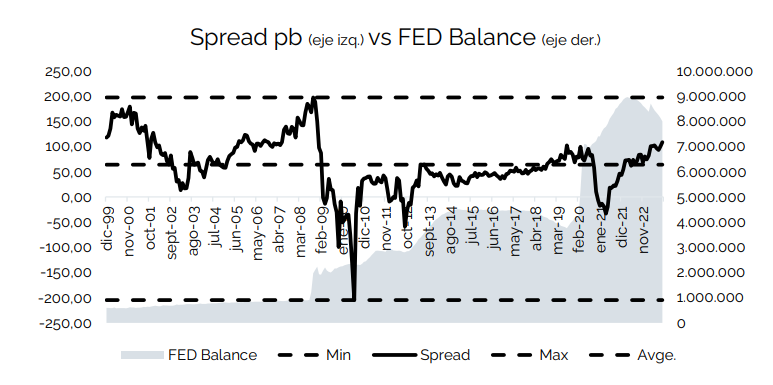

In addition, the yield spread between MBS and U.S. Treasury bonds is near its 10-year high (see the chart below). Over the past year, the Fed has halted quantitative easing (QE) and is reducing its balance sheet (QT), which means it is slowly reducing its holdings of MBS. The Fed holds about 37% of all agency MBS, which has caused the spread between these securities and Treasury bonds to widen as the Fed reduces its holdings of this asset.

With this major buyer out of the market, current investors are demanding a higher premium for holding MBS, so the spread has widened to over 100 basis points above yields on U.S. Treasury bonds of similar duration. Even compared to corporate credit, the additional yield premium on MBS appears relatively attractive.

In summary, Agency MBS valuations are at historically low levels, primarily due to technical factors. TThe strong fundamentals of this asset—which consist of a combination of yield potential, reduced prepayment risk, greater certainty in cash flow, and relative attractiveness compared to other fixed-income options—make Agency MBS an attractive investment at this time.

Felipe de Solminihac

Investment Analyst