Given the current market environment, characterized by an intense fight against inflation, financial conditions have become more restrictive, a significant amount of liquidity has been withdrawn from the markets, and access to credit and debt refinancing has become more difficult and costly for companies. This has also affected private equity, which had been the workhorse of this asset class.

Today we see that the cost of debt used to finance acquisitions has become a major drag on the performance of these funds, so much so that for a company acquisition financed with a 1:1 leverage ratio, the expected return drops from 16% to 11% due solely to the cost of debt. Added to this is the difficulty of securing financing for dealsor finding companies with more modest valuations.

A detailed look at the dry powder accumulated in this asset class—and the increase in this figure over the past 12 months—suggests that managers are having difficulty finding deals. We’ve seen how the market for IPOs, SPACs and M&As over the past 24 months, which could lead to underallocation within the portfolios that remained invested in these vintages. All of this information suggests that this vintage should yield annualized returns lower than what we are accustomed to, closer to 10–15%.

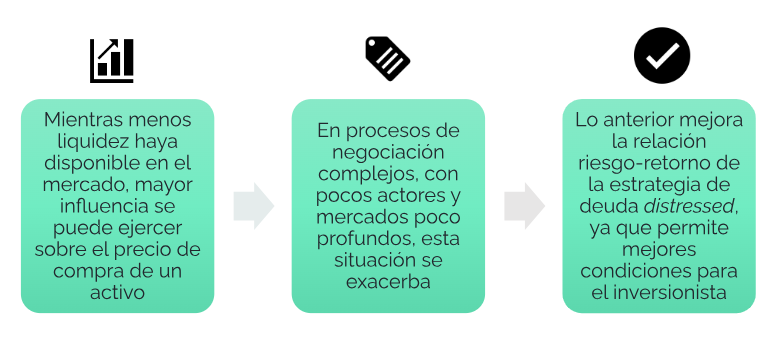

This is where we believe that there is an opportunity for distressed debt, where the less liquidity we find in the market, the greater the pressure these managers can exert on the purchase price of an asset. Generally, these negotiation processes are complex, involving few participants and shallow markets, which amplifies the situation in favor of the manager, improving the strategy’s risk-return profile.

Another factor that exacerbates this situation is the impending “maturity wall”, which will act as a catalyst for the new investment cycle. It is estimated that in 2025, approximately $351 billion in high-yield (HY) bonds and leveraged loans will mature in the U.S.—ten times more than this year’s $35 billion. In addition, the percentage of upcoming maturities from borrowers who generally have more difficulty refinancing—that is, those rated “B” or lower—will also skyrocket. Some of these troubled borrowers may have sustainable business models but suffer from unstable capital structures.

It is important to note that, unlike what happens in “healthy” markets, the purchase prices of corporate debt are around 65 versus 80 below par, respectively. This allows investors to acquire assets with a “cushion” for appreciation and greater potential upside.

Finally, ever since the Fed began its program of rate hikes and adopted the rhetoric of “higher rates for longer,” we have seen an increase in bankruptcy filings, or “Chapter 11” in the U.S. from companies that have failed to navigate this new landscape, which is generating a fairly broad that is broad enough to warrant careful scrutiny and a selective approach.

Given all the factors mentioned above and considering the current market conditions, we can expect net returns of 15–20% for investors in this type of strategy.

Felipe de Solminihac

Investment Analyst