Last week, we argued that various methodologies point to a rising—though still moderate—probability of a short-term recession in the U.S. ( https://www.fynsa.cl/newsletter/evaluando-los-riesgos-de-recesion-en-ee-uu/), but that high inflation is forcing the Fed to abandon its countercyclical policy, which could effectively lead to a recession, and that it is now less likely that “the Fed will eventually save the market,” since, if the Fed is determined to bring inflation down to its target, it is likely to cause significant economic pain first.

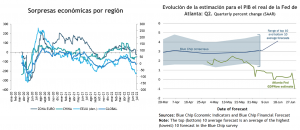

In this regard, the latest data continue to point to a sharp slowdown, and negative economic surprises have increased. What’s more, judging by the Atlanta Federal Reserve’s GDP estimates for Q2 2022, the U.S. economy may already be in a recession, as its latest update points to a 1.0% contraction in GDP—on top of the already revised official figures for Q1 2022, which showed a 1.6% contraction.

Market prices, meanwhile, are also beginning to reflect a growing risk of recession. In addition to the more than 20% decline in equities from their January highs, there has been a sharp correction in commodities (copper prices, for example, have fallen nearly 20% in the last 4 weeks), and U.S. Treasury yields have already fallen more than 50 basis points from their mid-June highs (the 10-year Treasury yield is back below 3.0%), and expectations for the federal funds rate now factor in nearly three rate cuts for 2023 (from the 3.5% it is projected to reach by December of this year—a level that, given current developments, may not be reached).

But if there were indeed a recession, what would it be like?

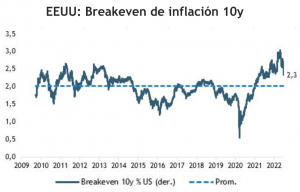

What we have today, however, is that while most survey-based measures of inflation remain at multi-decade highs, market-based readings do not indicate a further unanchoring of inflation. In fact, they have even moderated considerably recently. Ten-year inflation breakevens have returned to 2.3%, within their range of 1.5% to 2.5% over the past two decades. If they fall to 2% or below, the Fed will likely soften its tone and slow the pace of rate hikes.

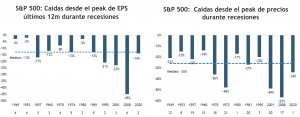

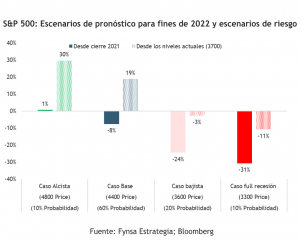

All in all, recent developments do not significantly alter our conclusions: that the markets—and equities in particular—already largely price in an “average recession,” and that the market’s potential bottom may not be that far from the lows already reached. Of course, volatility will persist for some time, and there is a risk that corporate earnings expectations will be “revised downward,” since it is inconsistent—given the growing risks of a recession—for the market to continue pricing in around 10% growth in corporate earnings for this year. Nor should you expect corporate earnings to suffer a major collapse, since—as is generally the case during periods of inflation— “nominal prices cushion the weakness in real volume.”