In May, we argued that the forces driving stock prices lower might begin to subside: it no longer seemed likely that the war in Ukraine would escalate into a broader conflict; the number of new COVID cases in China was declining; and global inflation might be peaking. Read more. In that context, we believed that the stock markets were pricing in too much recession risk and that the probability of a recession over the next 6 to 12 months, while rising, was still low; therefore, we maintained a risk-on stance. See more.

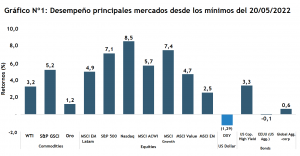

Fast-forward to today, and the easing of concerns about monetary policy and the risk of a recession which has helped fuel a relief rally in recent weeks—one that has been broad-based across all asset classes and regions. (See Chart No. 1.)

Source: Fynsa Estrategia; Bloomberg. Data as of June 2, 2022

Source: Fynsa Estrategia; Bloomberg. Data as of June 2, 2022

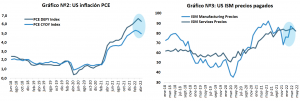

We believe the market has already largely factored in and priced the change in monetary policy and the significant tightening of financial conditions as inflation may be peaking or, at the very least, stabilizing to some extent (see Charts No. 2 and No. 3). In this context, temporary and base effects are likely to cause inflation to decline, which—optimistically speaking—would allow the Fed to take a breather before the important U.S. midterm elections this coming November.

Source: Fynsa Estrategia; Bloomberg

Source: Fynsa Estrategia; Bloomberg

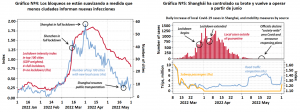

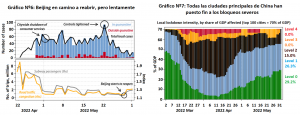

As for China, the two largest cities are taking significant steps toward reopening, as COVID-19 outbreaks have been brought under control. As of June 1, most of Shanghai’s 25 million residents were allowed to leave their homes and neighborhoods, subject to frequent COVID testing. Beijing began easing restrictions in most districts on May 29, although it continues to battle sporadic outbreaks and has no timeline for the citywide reopening. (See Charts No. 4, No. 5, and No. 6.)

Most cities, including Shanghai and Beijing, will continue to enforce several relatively strict COVID-19 prevention measures for the foreseeable future, which will affect consumer spending. However, with the end of Shanghai’s strict lockdown, the most severe disruption to supply chains should be over for now, and manufacturers can begin to recover.

The rest of the country continues to see gradual improvement. Just over half of the 100 major cities have lifted all restrictions, and some localities announced further reopening measures following Premier Li Keqiang’s teleconference with local officials last week. (See Chart No. 7.)

Source: Gavekal

Source: Gavekal

Regarding the market’s future trajectory, higher inflation and slower growth are now the consensus view, which will likely continue to drive greater volatility. Our best estimate remains that the U.S. economy will manage to avoid a recession—at least not an imminent one—so expected earnings growth would not be compromised (see Chart No. 8). Under these assumptions, S&P 500 levels significantly below 4,000 points remain unjustified, and we maintain our fair value estimates closer to 4,500 points (+10%).

Source: Fynsa Estrategia; Bloomberg

Source: Fynsa Estrategia; Bloomberg