The Japanese market has experienced a significant rally since the start of 2024, with the Nikkei 225 reaching a 34-year high. Year-to-date, the TOPIX is up 12% and the Nikkei 225 is up 17%, outperforming the S&P 500 (+9%) and Nasdaq (+9%), reflecting positive Japanese market sentiment. Corporate earnings growth continues steadily, stocks are up across a wide range of sectors and foreign investors are still underweight Japanese stocks, even though inflows have been flowing into the market of late.

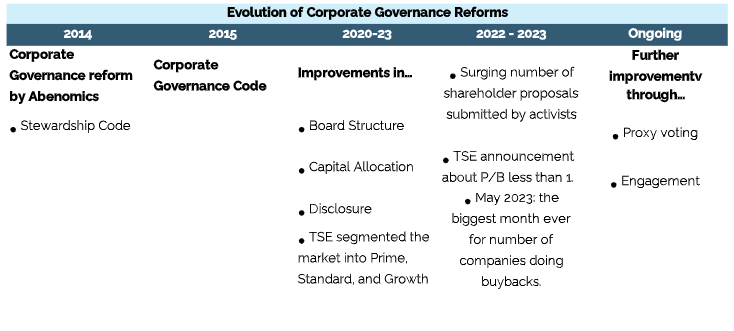

We remain bullish on Japanese equities due to the upside potential for corporate earnings, relative valuations, fund flows and corporate transformation driven by TSE-led reforms. As Japan emerges from the "lost three decades" thanks to structural changes in its economy, we interpret foreign investor fund flows this year as indicative that Japanese equities are shifting from short-term trading ideas to long-term investment targets.

There are several solid reasons to invest in Japan today, which can be summarized in 4 key points:

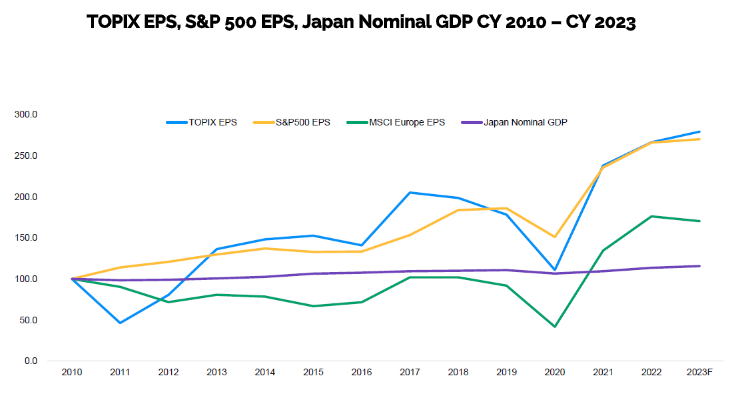

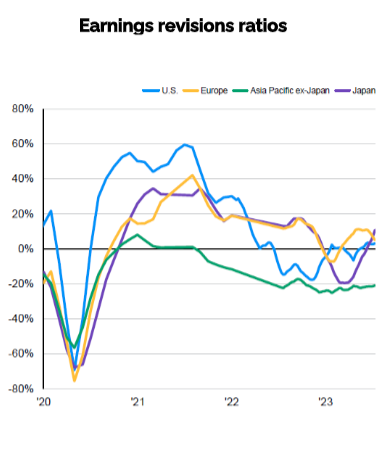

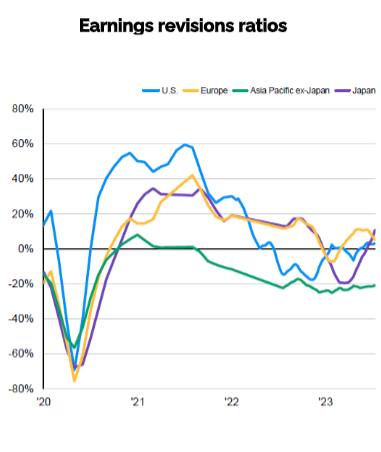

2. Japan's market comes with a very good earnings momentum. Japan and the US have had practically the same EPS increases since 2010, but the US is trading higher and higher, while Japan remains below average.

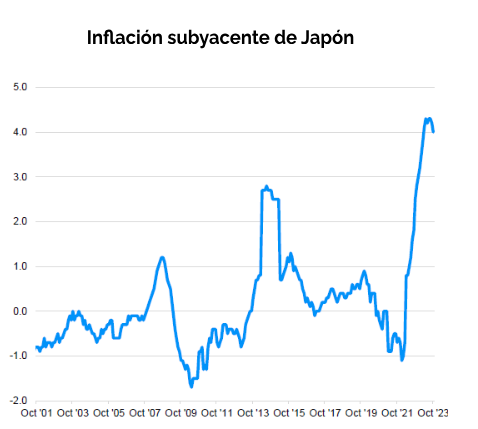

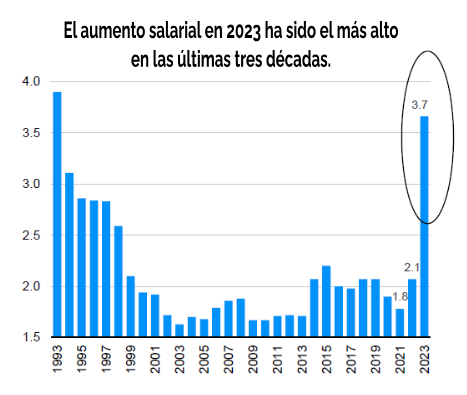

Japan's macro situation is improving. There is growing consensus that Japan will leave behind 3 decades of deflation, with rising inflation data and record wage growth. This has led the Bank of Japan (BOJ) to face crucial decisions in its monetary policy, considering the possibility of implementing interest rate hikes for the first time in almost two decades, thus ending curve control and negative interest rates. These changes are expected to be gradual and depend on the confirmation of a virtuous cycle between wages and inflation.

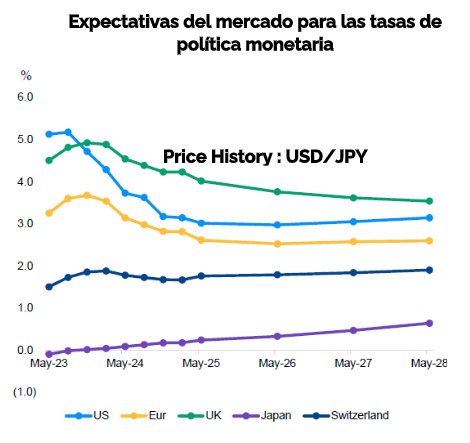

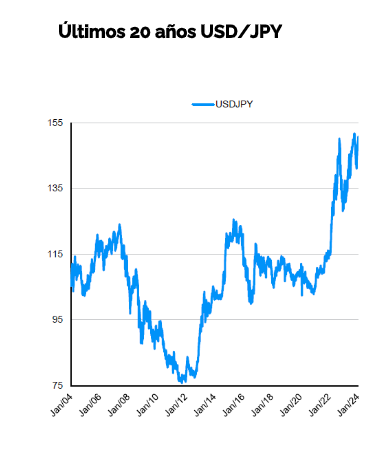

On the Yen side, it is undervalued, at one of the cheapest levels in the last 20 years (the currency has high appreciation potential as the market expects Japan's central bank to raise rates in the coming years, while the rest of the world expects rate cuts).

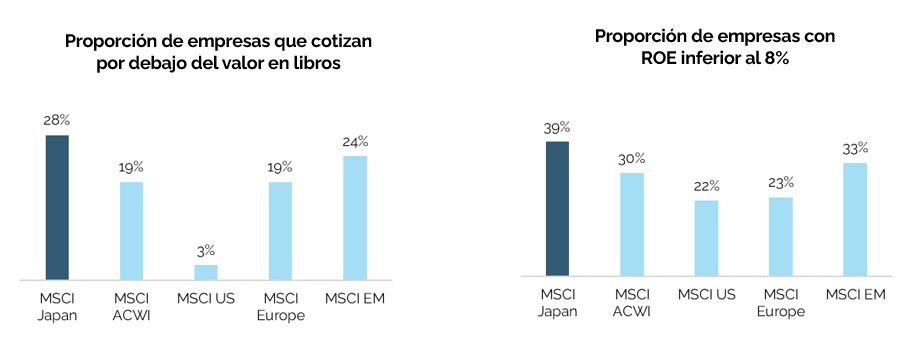

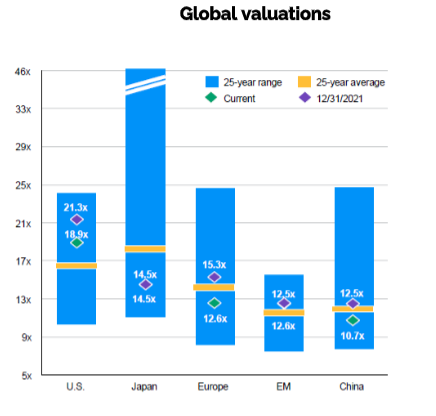

4. Japan's valuations and earnings growth expectations remain favorable.

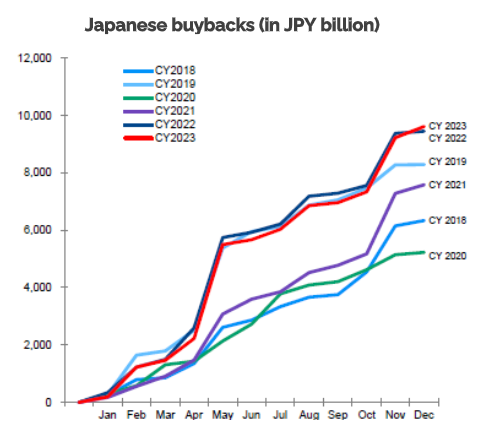

In conclusion, Japanese equities present extremely attractive investment opportunities. Driven by positive structural reforms led by the TSE, solid earnings per share (EPS) momentum, an improving macroeconomic situation and reasonable valuations, the Japanese market is emerging as a promising destination for investors.

Felipe de Solminihac

Investment Strategist

{kind=link}