IPSA Target - Adjusting projections to 5,800 points (+10%)

Share

Amid a challenging start to the year for risky assets, the IPSA has managed to outperform global markets affected by expectations of rate hikes by the Fed and the recent global geopolitical conflict.

The IPSA’s outperformance so far this year (+30% in USD compared with +21% for the MSCI Latam and -14% for the MSCI World) is mainly due to the strength of commodities and its “more value-oriented” composition—a characteristic shared by the rest of the region’s stock markets— which has encouraged greater investment inflows.

While the domestic outlook will remain complex due to the political and institutional challenges we face in the coming months (which are already largely factored into market valuations), the external environment offers some compensation, given the attractive prices of copper and commodities in general (iron ore, pulp, lithium).

The trend in corporate earnings remains extremely positive. Q1 2022 results have far exceeded consensus estimates. Sales came in 8% higher than expected, and earnings were 15% higher, with sales and EBITDA both growing by 44%.

Furthermore, positive earnings surprises are at record highs (over 50%). This has led to further earnings revisions for fiscal years 2022 and 2023 (+10% in the last week for both 2022 and 2023). So far this year, expected earnings have been revised upward by 37% for 2022 and 34% for 2023.

We also highlight the attractive dividend yield offered by the local stock market (+7.0% 12-month forward), with several companies projected to have double-digit dividend yields by 2023.

All in all, despite the IPSA’s strong performance so far in 2022—in contrast to global equities— we see room for further gains given that valuations remain attractive both in absolute terms and relative to emerging markets, and corporate earnings continue to beat expectations.

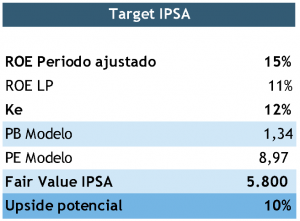

In this context, we are raising our target for the IPSA to 5,800 points (+10%) (previously 5,300). The exceptional earnings environment has resulted in ROEs well above their historical averages (+20%). We assume these levels are not sustainable in the medium term, so we are factoring in returns of around 15% for the next 12 months and a gradual convergence toward long-term averages of 11%. This offsets higher interest rates, which—combined with political and institutional risks—would keep valuations under pressure (we target a P/B multiple of 1.35x, which remains conservative by historical standards). An IPSA at 5,800 points would also be consistent with closing the discount gap we have relative to emerging markets (10%), a scenario that is equally conservative considering that historically we have traded at a 30% premium.

We favor stocks that we believe are undervalued (value), of high quality (solid financial position), and have growth potential. In terms of sectors, we are focusing on commodities, banking, and consumer goods.

Our Fynsa Total Return Fund provides exposure to local equities through an active, high-conviction strategy that maximizes alpha generation. The fund has posted a return of +33% so far this year, outperforming the IPSA by 11%.