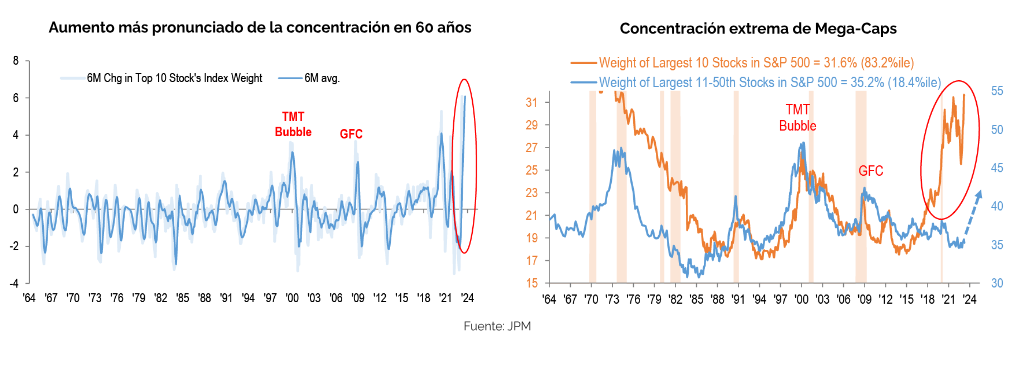

The recent increase in market capitalization concentration has been the most pronounced in more than 60 years of history, with an even narrower leadership than that observed during the TMT bubble. (JPM)

So far this year, six mega-cap LLM Innovation companies (MSFT, GOOGL, AMZN, META, NVDA, and CRM) account for 51% of the S&P 500’s return, 54% of the Nasdaq 100’s return, and 63% of the growth factor’s return.

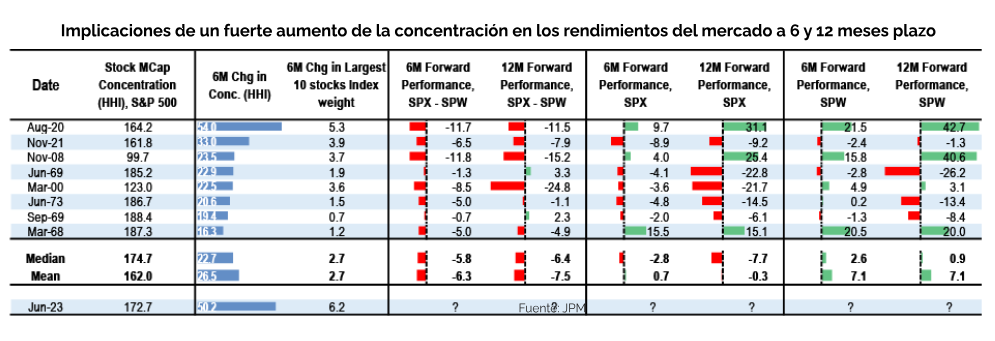

In the past, a sharp increase in concentration and concentrated leadership has always been reversed, with the S&P 500 equal-weighted index outperforming the market-cap-weighted index.

Of course, this alone is not a sufficient reason to sell the U.S. market, since reversing this extreme concentration would require a catalyst in the form of an additional inflationary shock (similar to 2022) or a hard landing for the economy—and that is not part of our base-case scenario. Otherwise, corporate earnings have continued to surprise on the upside, and economic data continues to point to a more resilient economy.

But if history is any guide, we believe it is warranted to consider a “different approach” to maintaining exposure to the U.S. market, given that a sharp increase in concentration is generally followed by superior performance of the equal-weighted index relative to the market-capitalization-weighted index, resulting in a reversal of concentration. (See attached table.)

In the first 6 months of the year, the market-cap-weighted index (SPX) outperformed the equal-weighted index (SPW) by ~10%; since then (and particularly in recent weeks), the SPW index has outperformed the SPX index by ~1%. Historical data suggests that further growth in market share is likely to continue for several more months.

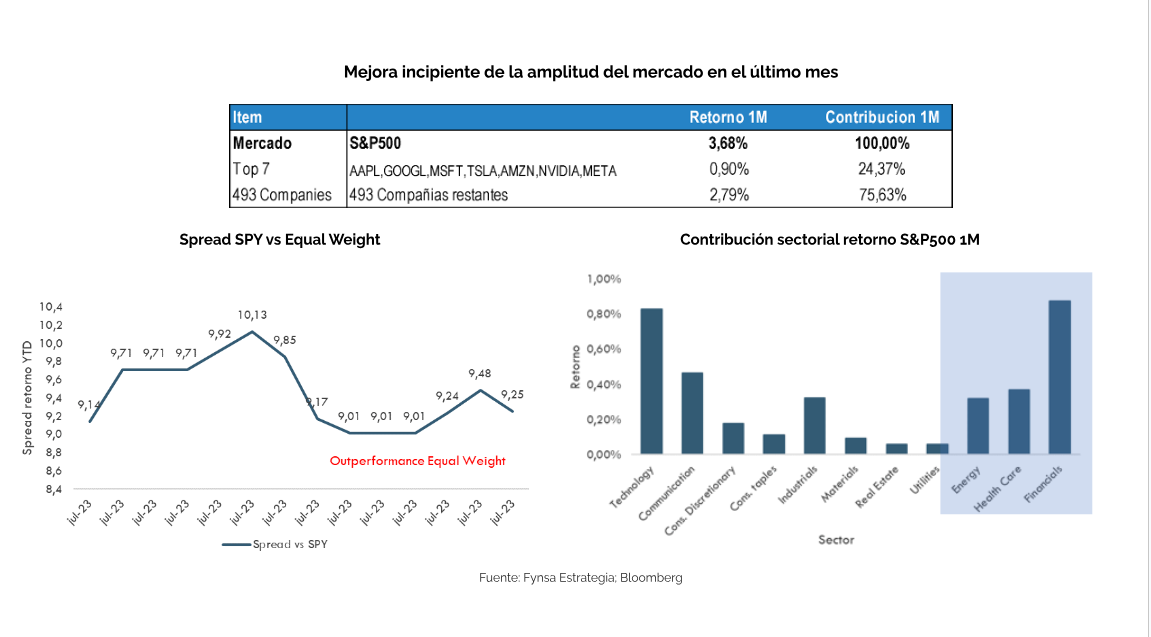

We recommend a more balanced allocation to address the heavy concentration in the U.S. market and overweight non-U.S. markets, where valuations are more attractive and dividend yields are higher. In the U.S., consider an equal-weighted index (RSP ETF). In terms of sectors, our strongest convictions are in Technology (XLK ETF) and Health Care (XLV US ETF), although we believe small- and mid-cap companies (IWM ETF) should also be considered to complement large-cap holdings (SPY ETF) and to diversify with some cyclical value stocks, such as lagging Financials (XLF ETF) and Energy (XLE ETF).