Last last week, we highlighted the opportunities emerging in the local equity market, given expectations of aggressive monetary easing going forward.

Well, this week we’ll be discussing opportunities in the fixed-income markets. The latest economic data—which showed weaker-than-expected economic activity and, above all, lower-than-expected inflation—clears the way for the Central Bank to make its first rate cut of 75 basis points (or even 100 basis points) at the end of this month and end the year with a policy rate of 8% (-325 basis points), an adjustment process that would continue into 2024 to a range of 4.25%–4.5%.

Given this, it is necessary to begin adjusting portfolios to take advantage of the declines in the TPM. Corporate bonds have historically outperformed money market instruments and government bonds during periods of falling TPM, therefore, gradually shifting away from time deposits and money market funds and beginning to prioritize fixed-income securities with maturities of 2 to 5 years—with a preference for well-rated bank and corporate bonds—is a first step to consider.

And while there are suggestions to increase exposure to peso-denominated securities, we believe this is not the time to abandon UF, not only for diversification purposes, but also because we believe that UF rates are oversold. Until a few weeks ago, UF forwards were pricing in a year-end CPI closer to 5%, but following the surprise downward revision in June’s inflation figures, this changed drastically, and projections now indicate that inflation will end the year even closer to the BCCh’s 3% target.

How much of this is due to the “flow effect”—investors shifting from real to nominal instruments, which has boosted returns in pesos and reduced those in UF—and how much of it is due to more fundamental factors? Presumably, there is a bit of both, but we believe an imbalance has emerged that is difficult to justify.

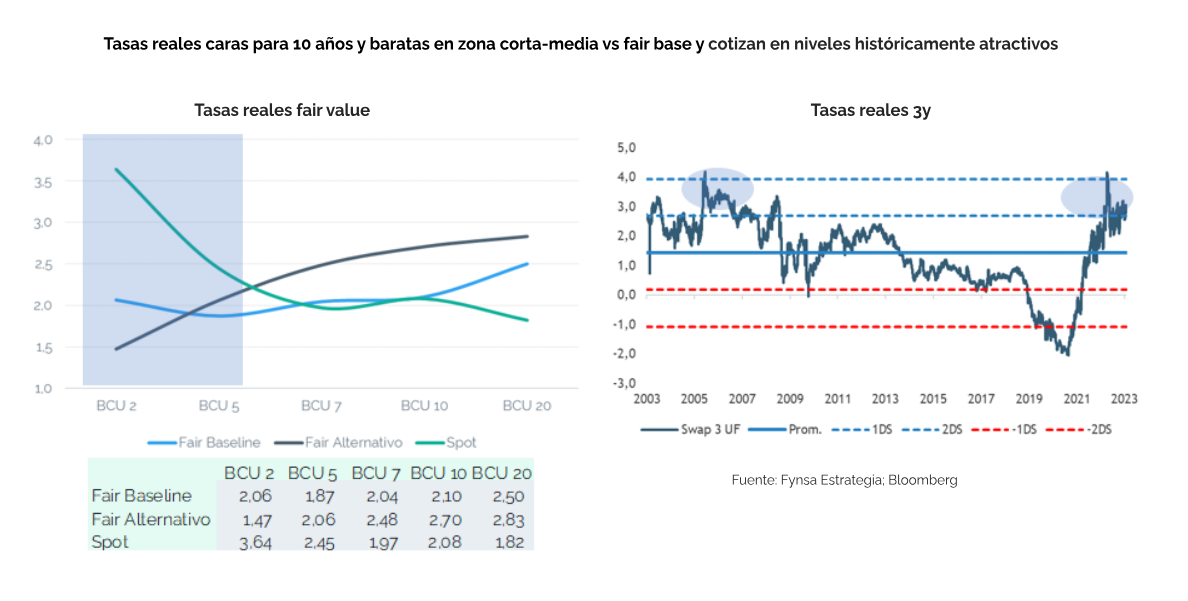

The sale of government securities has pushed yields above what we estimate to be “fair value” levels at the short and medium ends of the curve and we see some overreaction, given that the Economic Expectations Survey (EEE), released following the June CPI data, projects 4.2% inflation by year-end—which is largely in line with our Economics team’s estimates.

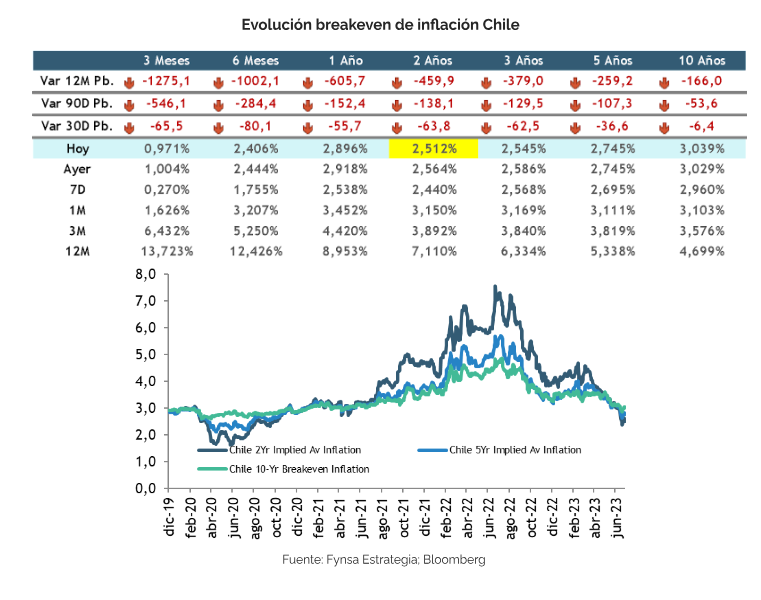

Another way to see that the market may be way ahead of the curve is what inflation breakeven rates show: which have become “unanchored” on the upper end, currently trading below 3% even for 5-year maturities.

In conclusion, the start of the monetary easing cycle will accelerate the shift of portfolios from IIF to IRF. Interest rate levels and accruals boost the value of the short end of the yield curve, but UF-denominated instruments are becoming more attractive, especially for terms of 2 to 5 years.

For more information, please review the sales presentation for the Fynsa Chile Debt Fund.