En los últimos meses hemos visto que la inflación en el país ha ido disminuyendo, lo que en gran parte se debe a que la TPM se ha mantenido contractiva por varios trimestres. Si bien en 2022 la inflación terminó el año en 12,8%, actualmente se encuentra en 7,6% y con tendencia descendente. Con esto, ya se puede percibir que el Banco Central vaya a bajar la TPM luego de que se haya mantenido en 11,25% desde el último aumento en octubre del año pasado. De hecho, en la última Encuesta de Expectativas Económicas, los resultados indican que podría existir un recorte de 75 puntos base en la siguiente reunión.

La reducción de la TPM, y expectativas de inflación más normalizadas, generan una economía que empezará a presentar tasas más bajas en la parte corta de la curva, lo que implicaría en que los retornos en la renta fija tradicional de más corto plazo ofrecerían un menor rendimiento a futuro, impactando a los inversionistas que se mantengan en este tipo de activos. Ante esta situación, será esencial buscar alternativas que permitan obtener mayores retornos.

Con esto, la deuda privada se convierte en una opción atractiva para los inversionistas en este contexto de bajas tasas de interés. Debido a sus características, la deuda privada suele ofrecer rendimientos más altos que la renta fija tradicional. Factores como la ausencia de mercado secundario, que implica menor liquidez, y el mayor riesgo crediticio asociado a las empresas privadas, generan una compensación para los inversionistas en forma de tasas de interés más elevadas. Aun así, estos riesgos pueden ser bien administrados con diversificación, pólizas de seguros, y buenos activos como garantías, entre otras medidas.

Las tasas de interés de los instrumentos de deuda privada, que tienen plazos de vencimiento mayores a un año, suelen estar vinculadas a la Tasa Máxima Convencional (TMC), que están más relacionadas a las tasas de largo plazo que a las de corto plazo. Debido a esto, una reducción en la TPM impactará de manera más moderada en este tipo de activos de deuda privada, en comparación con la deuda de más corto plazo.

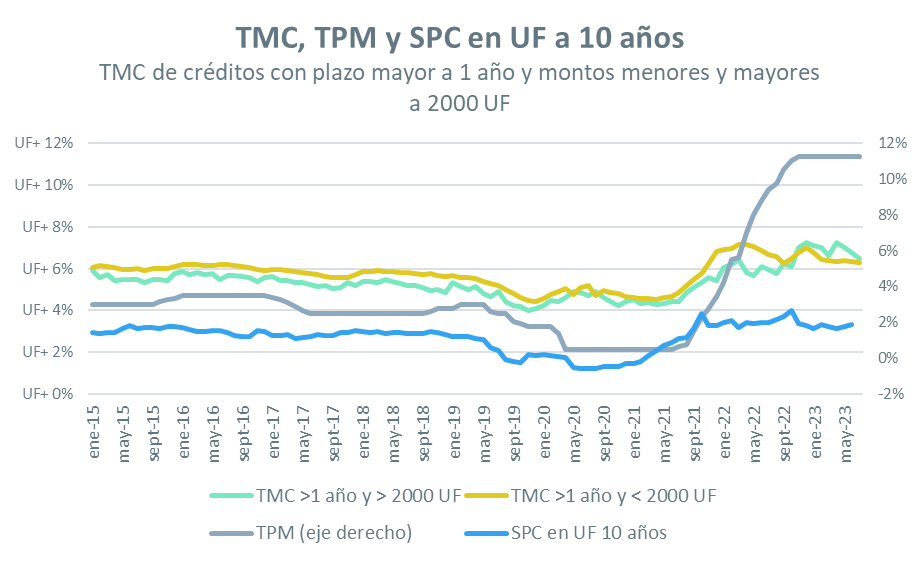

Tal como se ve en el gráfico, actualmente la TPM se encuentra en su nivel más alto de los últimos años, mientras que las TMC en UF, que define la ley por plazos mayores a 1 año, no se han elevado en la misma proporción, debido a que el mayor determinante del aumento de las tasas más largas ha sido la incertidumbre política y económica local, y no la política monetaria. Sin embargo, a medida que se observen recortes de la TPM, se deberán buscar mayores retornos en otro tipo de activos, en los que podría destacar la deuda privada.

La ausencia de un mercado secundario para la deuda privada implica que los inversionistas no enfrentan la volatilidad asociada con la variación en las tasas de interés. Con esto, los inversionistas pueden obtener un retorno más estable en sus inversiones, en comparación a la deuda fija tradicional.

En un ambiente de tasas más bajas, la búsqueda de oportunidades de inversión que permitan obtener rendimientos más altos se vuelve esencial. La deuda privada se destaca como una opción atractiva para que los inversionistas incluyan en sus portafolios de inversión, ya que ofrece tasas de interés más altas que la renta fija tradicional debido a factores como menor liquidez y mayor riesgo crediticio. En este escenario, considerar la deuda privada como parte de una estrategia de inversión de largo plazo puede ser una decisión prudente para aquellos que buscan obtener retornos estables y más altos en un contexto de bajas tasas de interés.

Vicente Dourthé

Analista de Activos Alternativos Fynsa AGF