In recent years, factoring has been fundamental for SMEs to access agile and efficient financing, especially those that have difficulties with traditional credit. There are several modalities, such as factoring with recourse, without recourse, international and electronic, with a notable increase in digital platforms for the automated and secure management of accounts receivable.

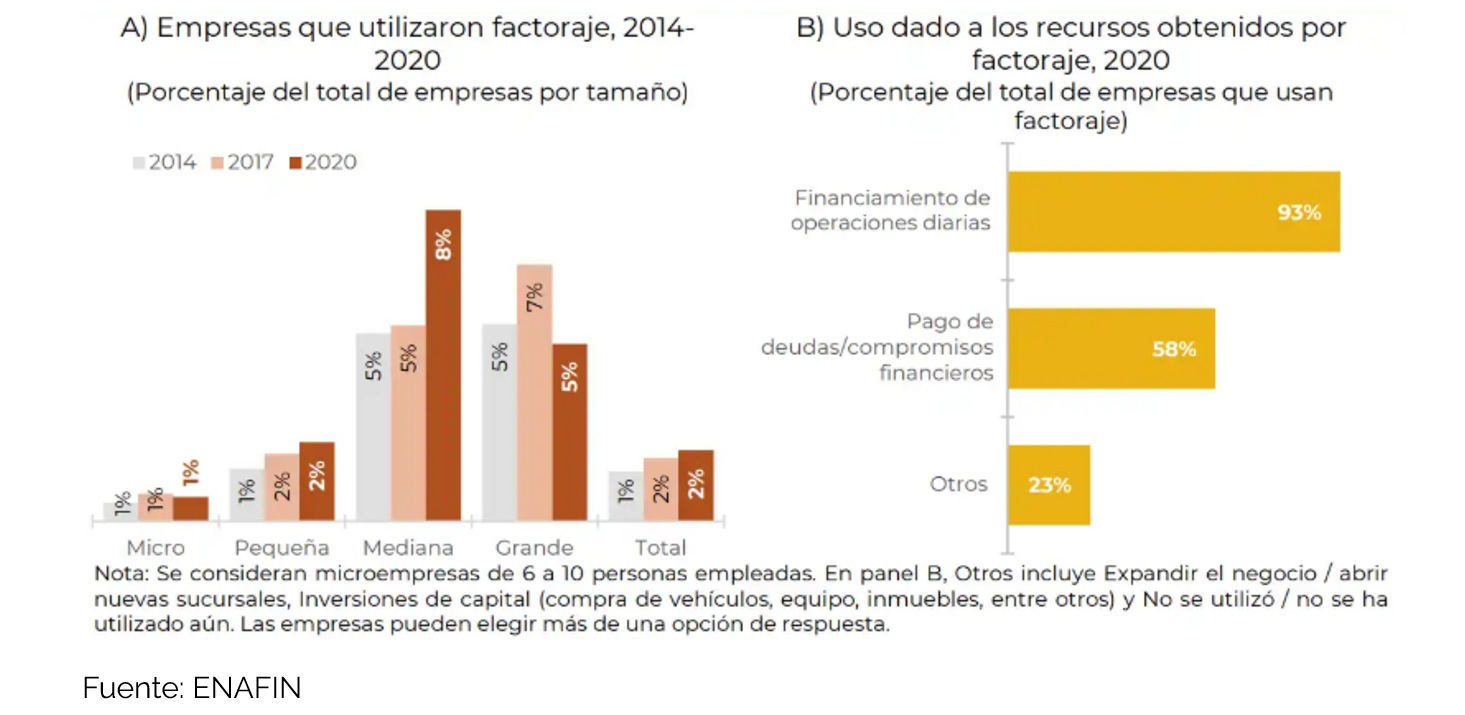

According to the Encuesta Nacional de Financiamiento de las Empresas (ENAFIN) 2021, only 2% of Mexican companies used financial factoring in 2020, a percentage similar to that observed in 2017. However, the growth potential is high, as 97% of companies have never resorted to this tool, often due to lack of knowledge. According to the Asociación de Sociedades Financieras de Objeto Múltiple en México (Asofom), 46.6% of SMEs have resorted to factoring due to lack of access to bank financing.

According to the Mexican Association of Financial Factoring and Similar Activities (AMEFAC), financial factoring in Mexico has grown at an average annual rate of 15% over the last five years. This trend reflects the growing confidence of Mexican companies in this financial tool, especially in times of economic uncertainty.

In 2024, the factoring market size reached US$66.1 billion, with a projected compound annual growth rate of 6.88% for the period 2025-2033, estimated to reach about US$126 billion by 2033. This growth is driven mainly by the demand for working capital from small and medium-sized companies, the integration of digital technologies and the expansion of e-commerce.

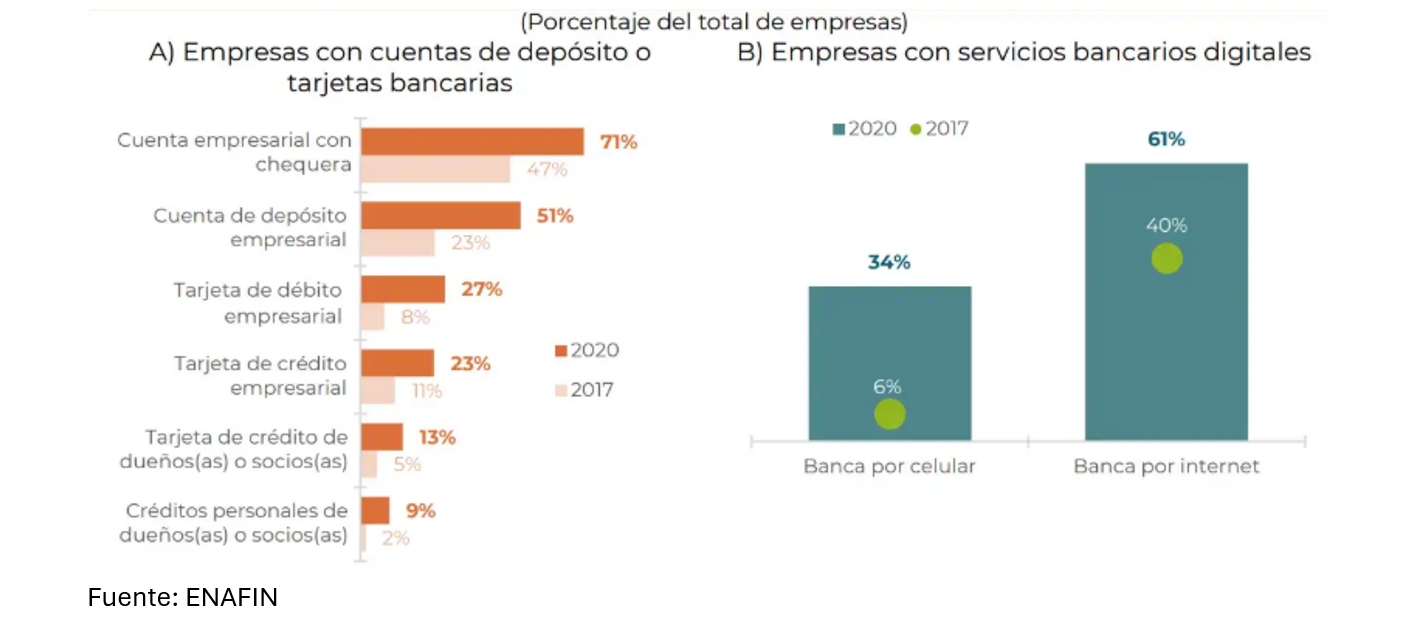

The use of digital platforms has made it easier for companies to access factoring more quickly and efficiently. According to official data in Mexico, 61% of companies already use internet banking and 34% use mobile banking, which could drive greater adoption of digital factoring, as companies are already familiar with the use of digital tools for money management.

On the other hand, Fintechs have simplified the application and approval of factoring through digital platforms. Today, SMEs can access liquidity in less than 72 hours, without excessive paperwork or complicated procedures.

In addition, the automation of processes, such as risk assessment and accounts receivable management, has made factoring more accessible and efficient than ever before. The use of digital platforms for factoring is expected to grow 30% annually over the next three years, according to a study by Statista.

Factoring in Mexico has its legal framework mainly in the General Law of Credit Instruments and Operations, the Law of Credit Institutions and the General Law of Credit Organizations and Auxiliary Credit Activities, as well as the Code of Commerce.

The institutions that provide this service are subject to the same laws that govern other financial organizations, such as the Law of the National Banking and Securities Commission, the Law for the Protection and Defense of Financial Services Users and the Law to Regulate Financial Groupings.

In terms of regulatory institutions, factoring practices and the institutions that offer this service are monitored by the Ministry of Finance and Public Credit (SHCP), Banco de México, the National Banking and Securities Commission (CNVB) and the National Commission for the Protection and Defense of Financial Services Users (Condusef).

In conclusion, financial factoring in Mexico presents an invaluable opportunity for SMEs seeking to maintain a healthy cash flow and boost their growth. With the combination of technology and sector specialization, Fintechs are positioned as a strategic ally for those companies that want to maximize their potential and remain competitive in the market.

Cristián Rodríguez

Country Head Mexico