The IPSA is trading at a discount to its 10-year average forward price-to-earnings ratio, against a backdrop of slower-than-expected economic growth and a challenging external environment due to geopolitical conflict. However, we remain highly confident in local equities over a six- to eighteen-month horizon.

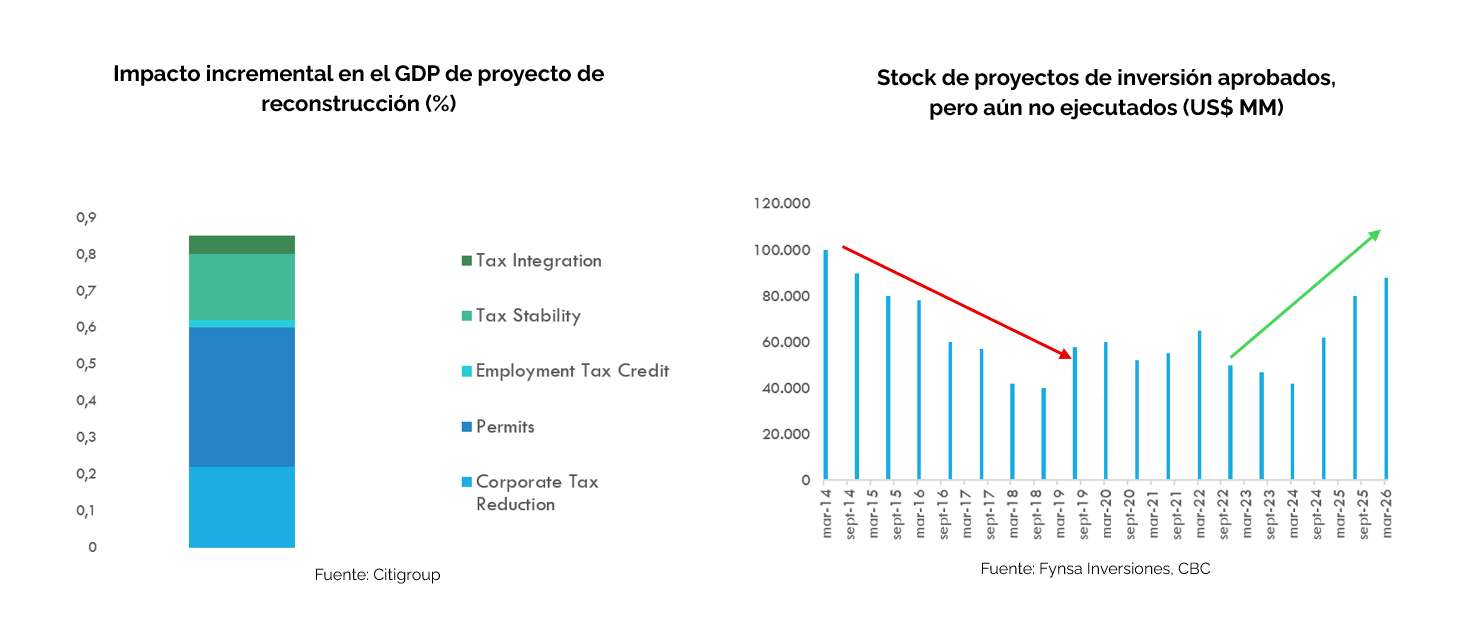

For years, the debate over long-term growth in Chile has been dominated by regulatory uncertainty and stagnant investment. That landscape is changing. The Reconstruction Act, currently in the final stages of the legislative process in the Senate, could provide one of the biggest boosts to investment in decades.

As a point of reference, corporate tax cuts, tax simplification and stability, along with the streamlining of permitting processes and other measures to stimulate the labor market, could add up to one percentage point of GDP growth, in addition to the positive effects of pension reform on the capital market.

However, following the weak growth expected in the first half of 2026—due to one-time supply-side factors and lower domestic demand resulting from the conflict in the Middle East—economic activity is projected to improve in the second half of 2026 and in 2027, driven by an increase in the investment portfolio and a gradual recovery in private consumption.

For the stock market, the implications are clear. In addition to lower corporate tax rates and tax simplification, there is the potential for increased investment, which will have a direct impact on companies in the construction and commodities sectors, for example. Furthermore, the effect on private consumption—especially in regions with a high concentration of projects—adds a second layer of benefit for the consumer sector (which must be accompanied by measures to stimulate the labor market) and for banks, through increased lending.

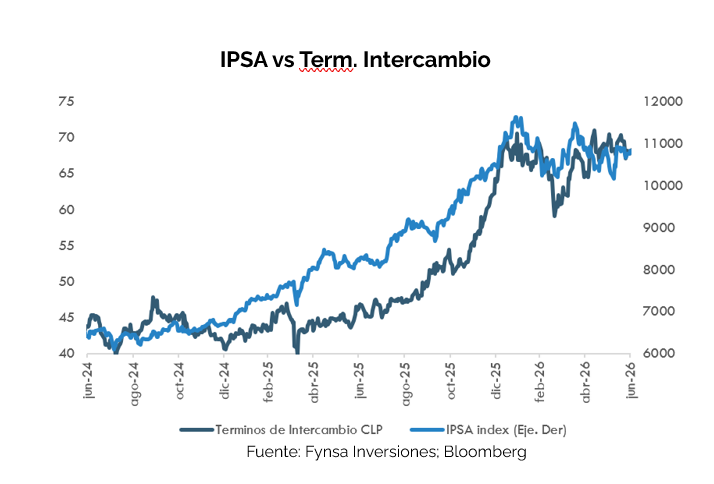

On the international front, Chile is one of the world’s leading copper producers and, at the same time, a major importer of oil. Progress in geopolitical negotiations in the Middle East and the recovery of supply are leading to a sustained normalization of energy prices.

A normalization in energy prices has a direct impact on sectors such as retail, airlines, manufacturing, and logistics operators, which may have been affected by higher operating costs. The realization of wider margins due to lower energy costs has the potential to generate positive surprises for earnings.

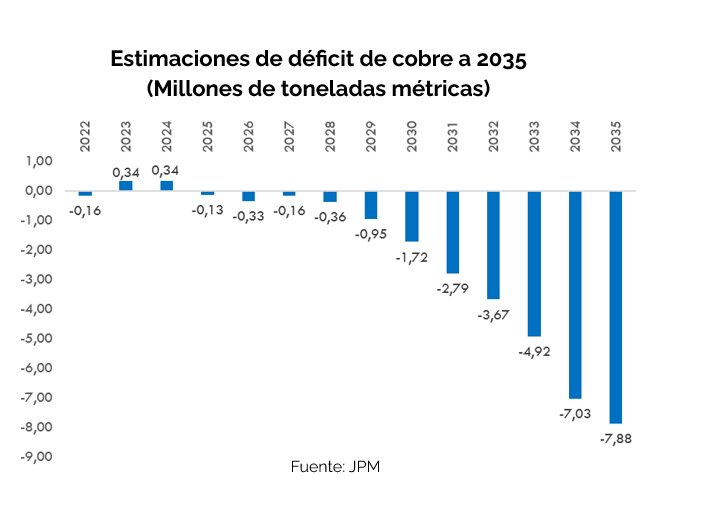

At the same time, copper prices are trading near their all-time highs, driven in part by structural demand linked to the energy transition and the expansion of technology infrastructure. The simultaneous rise in the price of our main export and the decline in the price of our main import have improved Chile’s terms of trade, with direct effects on the exchange rate, international reserves, and fiscal sustainability.

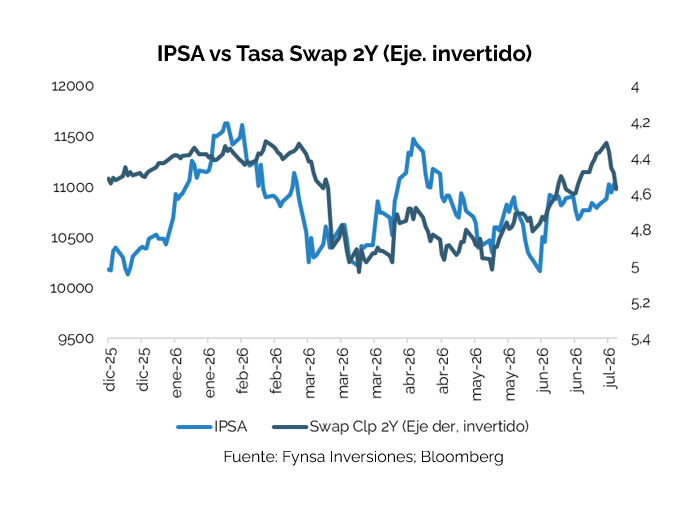

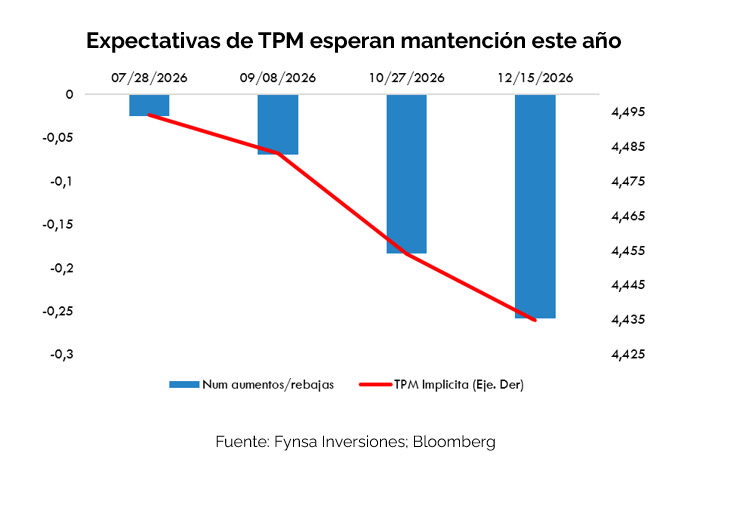

The Central Bank of Chile (BCCh) is keeping its monetary policy rate at 4.5%, a level that is just one or two cuts away from the estimated neutral rate of between 4.0% and 4.25%. With inflation gradually converging toward the 3% target and economic activity slower than expected, we believe that, as the geopolitical conflict continues to de-escalate, the BCCh will have more grounds to implement the remaining rate cuts needed to reach neutrality.

It is important to view continued monetary easing as a positive catalyst for the IPSA, since the discount rate applied to companies’ future cash flows is the denominator in valuation models.

On the other hand, the impact of the pension reform is leading to greater allocation by the AFPs to domestic assets. Effective April 1, 2027, the system of five funds categorized by risk type (A–E) will be replaced by ten generational funds differentiated by age groups. The change entails new investment benchmarks for each fund, with different limits on exposure to foreign and domestic assets, in both equities and fixed income. On balance, these changes are driving capital flows toward domestic assets.

Added to this is the gradual rise in stock prices, which by 2027–2028 begins to inject increasing capital into the capital markets and bolsters demand for local assets.

In conclusion, the four drivers described above—economic recovery, an improvement in terms of trade, monetary easing, and social security cash flows— offer Chilean stocks high potential for medium-term returns.

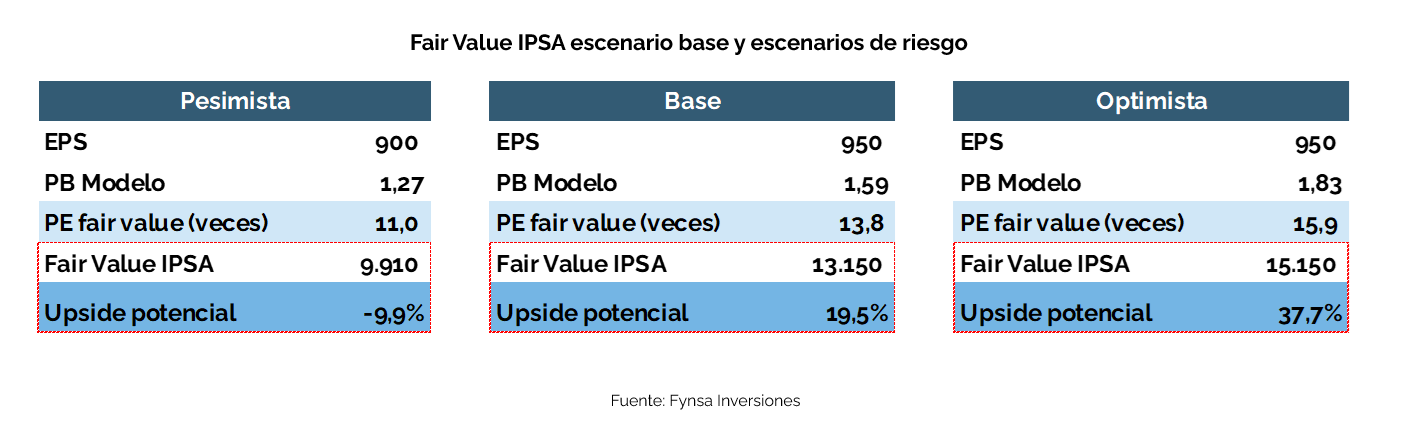

Within this framework, the target price (TP) we have set for the IPSA in the base case scenario is 13,150 points, representing a potential upside of 19.5% from current levels. This result incorporates EPS growth for the index’s constituent companies of between 10% and 15%, driven by the recovery in economic activity and improved terms of trade, along with a multiple expansion toward a P/E ratio of around 14 times, according to our valuation model.

In the optimistic scenario, where the IPSA returns to its average levels prior to the social unrest and the pandemic (close to 16 times), the target price would reach 15,150 points, equivalent to a potential upside of 37.7%.

Tomas Fernandez

Portfolio Management Analyst, Finance and Business, Stock Brokerage Firm