The May inflation figures and second-quarter corporate earnings point in the same direction: the fundamentals underpinning the appeal of local assets have not changed. In fixed income, UF-denominated rates have returned to historically high yield levels. In equities, valuations have become more attractive, and the medium-term catalysts—geopolitical de-escalation and pro-investment reform—remain in place.

The May inflation data sent a significant signal: for the time being, there is no evidence that inflationary pressures are spreading to other categories in the basket, and the food component actually contributed to deflation. This is a positive outcome, as it tempers arguments for monetary tightening and suggests that the shock in energy prices may be more transitory than structural. At the same time, inflation have shown a downward trend over the past month, in line with progress in the Middle East negotiations and domestic demand that is more moderate than projected.

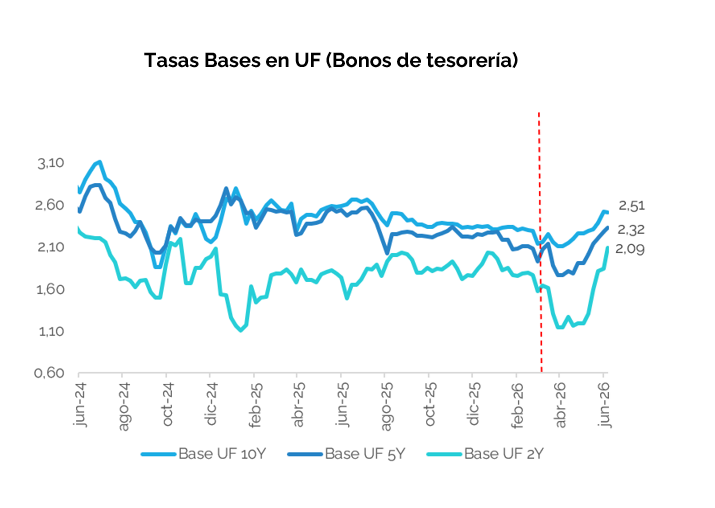

Following the increases in real interest rates (UF) in recent weeks—particularly at the shorter end of the curve— the inflation premiums implied by the bond market are below 3%, levels we consider attractive for maintaining a position in UF. We do not expect persistent inflationary pressures stemming from energy prices, nor do we expect deflationary pressures. The track record of recent years has shown that buying inflation below 3% has been a good bet.

Given this, we maintain a positive outlook on inflation-linked strategies, which offer protection that is difficult to replicate with nominal instruments.

Rates in UF have returned to accrual levels that are above the 10-year average, making it an attractive entry point for this type of strategy.

As for the MPR, the most likely scenario is that the Central Bank will adopt a more cautious stance, waiting for global uncertainty to ease before resuming the easing cycle. The labor market remains depressed, growth continues to fall short of expectations, and inflationary pressures should gradually normalize as negotiations in the Middle East progress. The balance of risks does not justify monetary tightening.

In the equity market, we continue to view recent pullbacks as buying opportunities. Over the past month, we have faced an external environment marked by tighter financial conditions, rising sovereign bond yields, and a strong global dollar—factors that tend to dampen appetite for emerging market assets. Added to this are weak consumer spending in China and adjustments in lithium prices.

All in all, these factors should begin to ease in the coming weeks or months as geopolitical risks subside, which, in turn, should reduce the pressure on the U.S. Federal Reserve (Fed) to tighten monetary policy.

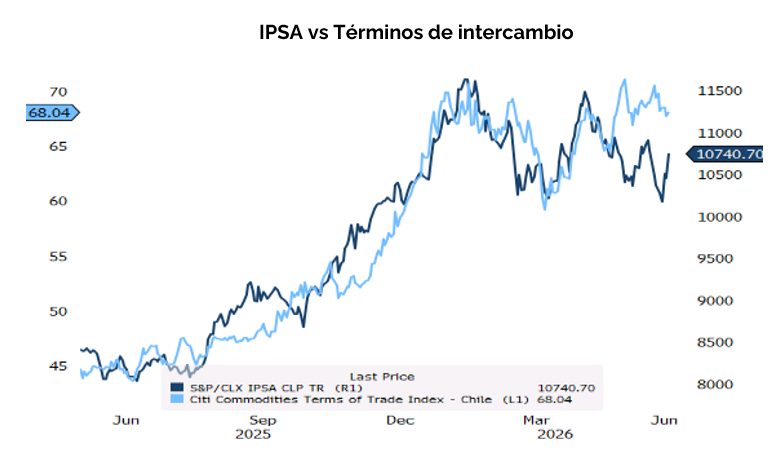

In addition, we maintain a positive outlook for copper prices, given a market that is projected to be structurally in deficit. As oil prices moderate and copper prices remain at high levels, this should translate into an improvement in the terms of trade.

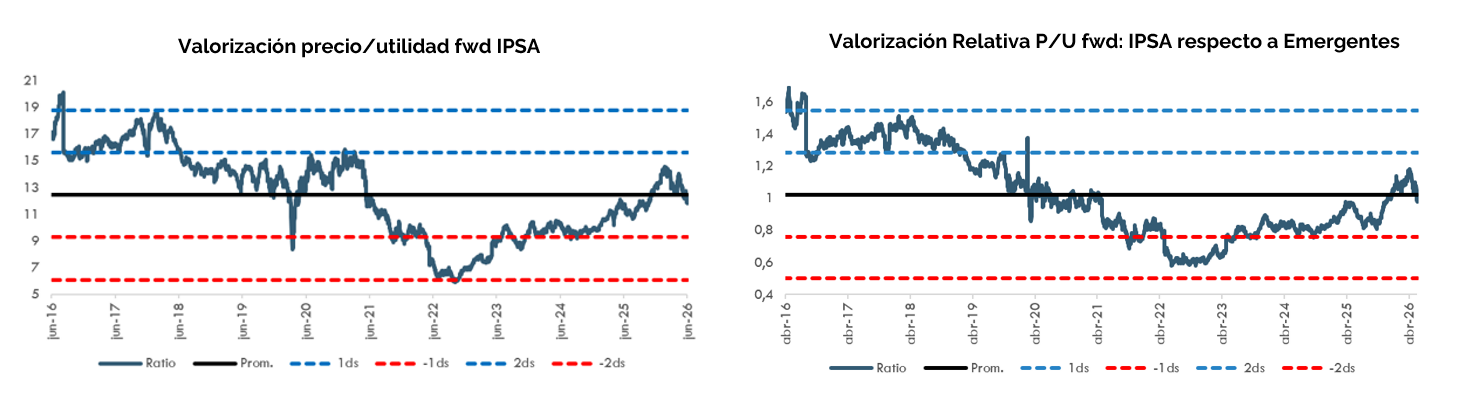

The second quarter has been a strong earnings season for IPSA companies. EBITDA figures show no deterioration in corporate fundamentals, which has left valuations at even more attractive levels.

In terms of valuations, the index is trading below its 10-year average in terms of P/E ratio forward, presenting an attractive entry point for a medium- to long-term horizon. We conservatively target a valuation of around 13 times, and around 16 times as an optimistic scenario if the current government’s pro-investment reforms materialize.

Where are the biggest opportunities by sector? We continue to see significant value in the banking sector.

In the short term, the banking sector has managed to offset the weaker domestic demand with higher inflation, which has resulted in a significant improvement in the net interest margin (NIM) in the current quarter. High inflation favors banks, given the natural mismatch in their balance sheets, and this effect should be clearly reflected in second-quarter results.

Inflation data for April and May show a total increase of over 2%, suggesting that this could be the best quarter of the year for the sector. Preliminary results for May confirm this: Banco de Chile reported an ROE of ~29% (up from 19% in 1Q26), driven by stronger net interest income (+39% year-over-year); Santander posted a strong ROE of ~35% with a net interest margin that rose +22% year-over-year; meanwhile, BCI posted a solid ROE of ~20%, above its guidance of 14%. The exception is Itaú, with a weaker ROE of ~8%, given its lower exposure to UF and higher expenses.

In the medium term, we have identified three additional catalysts for the sector:

Tomas Fernandez

Portfolio Management Analyst, Finance and Business, Brokerage Firm