Markets remain optimistic about a soft landing for the U.S. economy and that further progress on inflation would pave the way for the Fed's long-awaited rate cuts. and that further progress on inflation would pave the way for long-awaited rate cuts by the Federal Reserve.

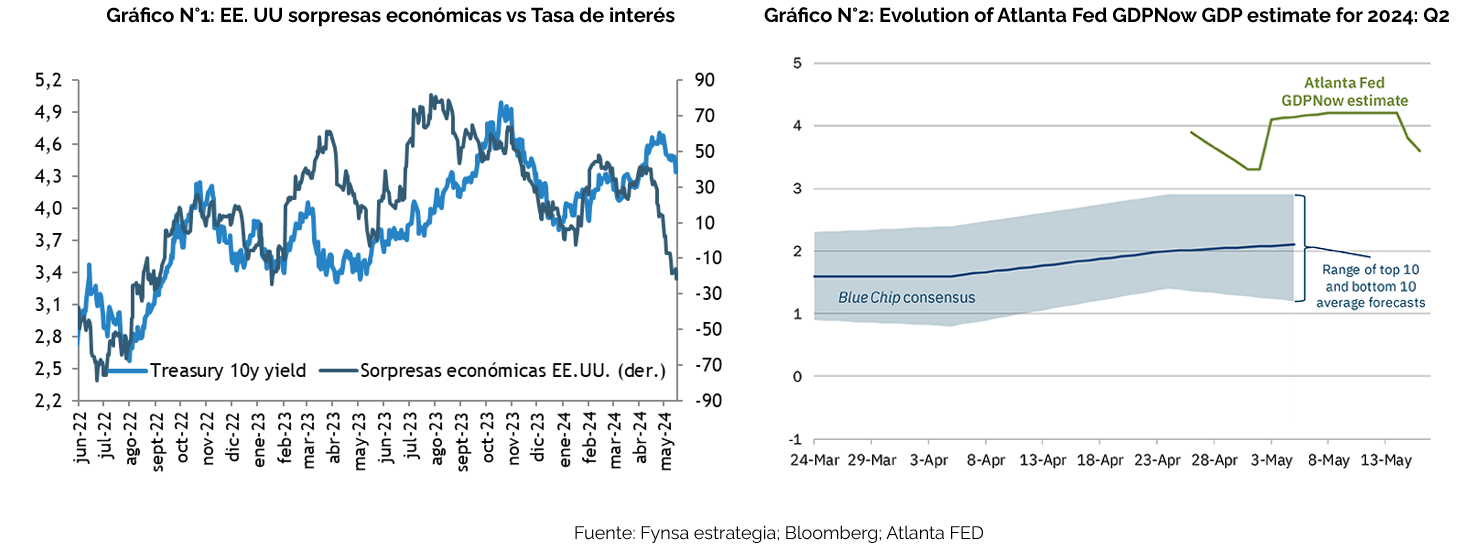

But at this point, how much are the economy and inflation cooling? True, in recent weeks U.S. economic data has been surprisingly generally downward in the U.S. and that has taken interest rate pressure off the market, but negative economic surprises are not synonymous with weak activity.

In contrast, recent activity data continue to show solid growth, and while labor market indicators show greater balance, recent inflation readings suggest that risks to the inflationary part of the Fed's mandate remain high.

Note, for example, the Atlanta Fed's estimate for second quarter growth (which, by the way, incorporates the recent "negative economic surprises"). With incoming data for the quarter, U.S. GDP growth is running at a 3.6% rate (well above potential), led by consumption growing at a 3.4% rate.

And during this week we released April inflation data, which was generally in line with market estimates on a year-over-year basis, with headline inflation coming in at 3.4% year-over-year and core inflation at 3.6%. Of course, these readings were interpreted positively by the market, given that we were coming from a couple of months with upside surprises in inflation and that the year-on-year readings were slightly lower than in March.

But the underlying question is: Is inflation really improving enough to justify lower rates? Something on the margin, but nothing spectacular. The deflationary trend continues in goods and little progress even in services. The super core (core inflation of services minus housing), in monthly terms was "only +0.5%", less than last month's 0.7%, however, the year-on-year change remained above 5.0%.

Thus, we believe that the incoming economic data indicates that it will take longer for the Fed to gain confidence about inflation convergence and, therefore, it seems prudent to maintain a tight stance for longer. and, therefore, it seems prudent to maintain a restrictive stance for longer.

Does this mean the market will forgo some rate cuts for this year? Probably not, but at best we believe it would be no more than 2 and the likelihood that none will materialize has been increasing.

Does this mean that the next rate move by the Fed could be upward rather than downward? Further rate hikes are not part of our baseline scenario and the need for further tightening would be channeled into higher current rates for longer.

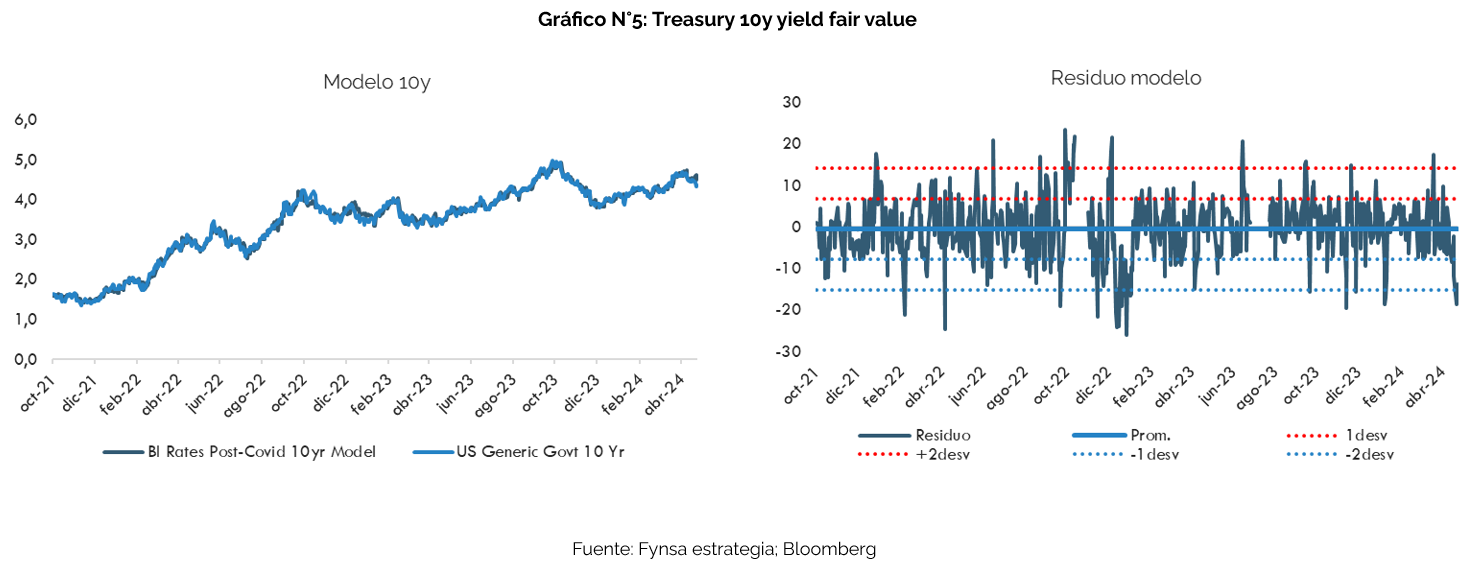

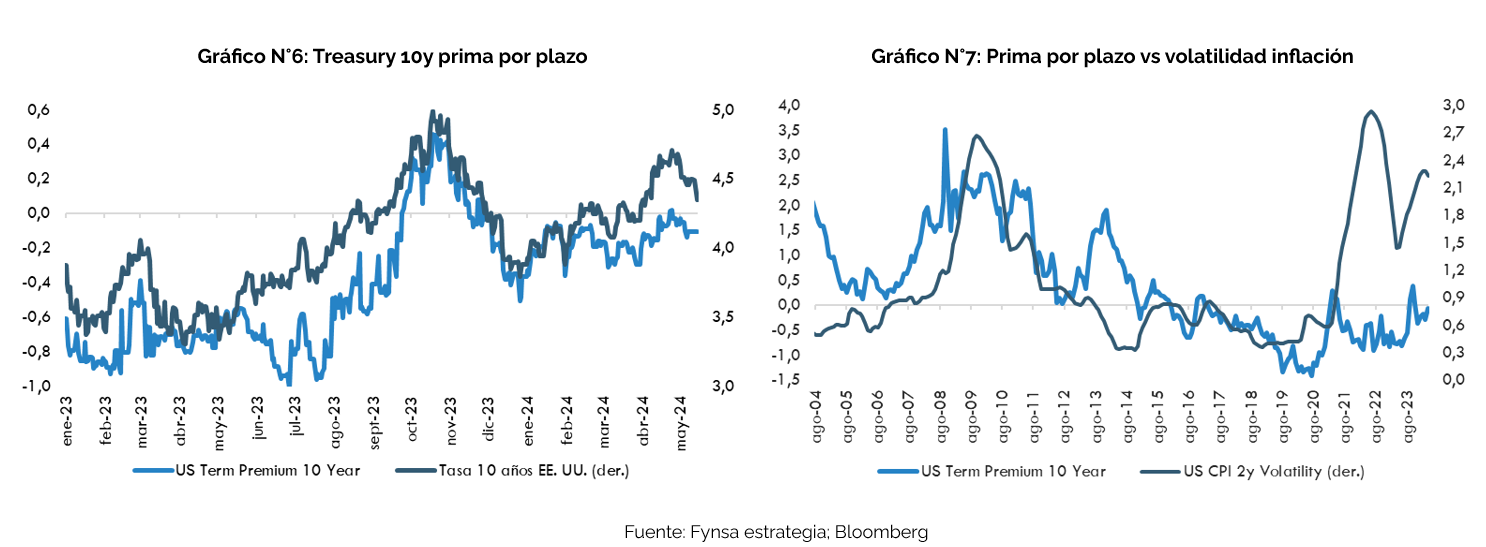

In this context, we believe that volatility will remain in the long end of the rate curve amid higher fiscal pressures and high inflationary volatility that do not justify negative term premia at this stage.. The 10-year Treasury fell this week to levels close to 4.30%, after having traded at 4.75% at the end of April, and with the information available we do not see much room for further falls in the short term. In any case, what has been re-validated after this new rate turn is that the market becomes quite sensitive to duration as we approach 5% (which is the zone where rates are considered "cheap").

Finally, in terms of duration, it seems prudent to continue to maintain a fixed income strategy in the short/mid part of the curve (between 3 and 5 years), until there is more evidence of inflation convergence and a "friendlier" monetary and fiscal policy.

Why not just a short duration? Because in a more medium/longer-term context, we believe intermediate maturities may offer a sweet spot between cash, where yields will decline as central bank rate cuts begin, and long-duration bonds, which could face pressure from the increased supply of bonds needed to finance growing sovereign debt.