"Don't put all your eggs in one basket". It is a typical cliché phrase when it comes to investing, but it has a practical logic behind it. Its origins go back to Harry Markowitz and his modern portfolio theory, for which he won a Nobel Prize in Economics in the 1950s.

The idea is that, by diversifying in different assets, the risk of each investment is reduced, since some can compensate for the losses of others. This makes it possible to create an efficient portfolio that minimizes risks. If the assets are not very closely related to each other, i.e., they have a low correlation, this risk can be better managed. Even if the assets are negatively correlated, a strategy with almost zero risk can be created.

The problem is that, in practice, things don't always work exactly as the theory says.

There are many factors that complicate investments: assets change over time, there are barriers to access certain markets, taxes and -of course- each investor has his or her own needs and objectives. This makes risk exposure vary from person to person.

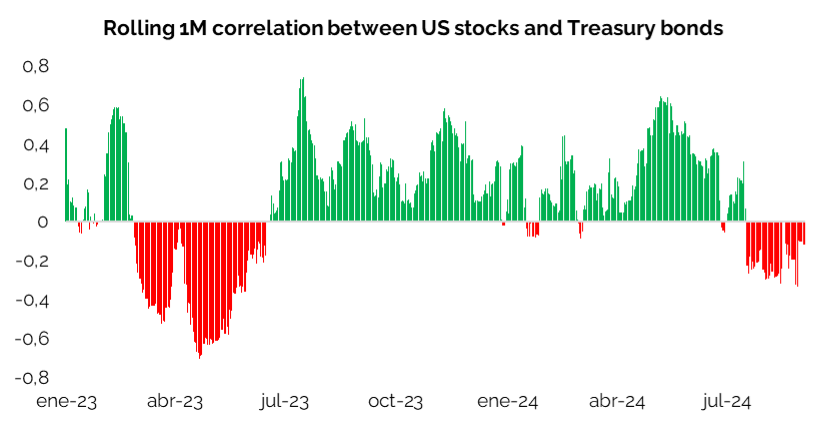

But despite the above, one principle remains clear: the lower the correlation between assets, the lower the risk. And if well managed, this can lead to better returns with an acceptable level of risk. An interesting example is the correlation between the U.S. stock market and Treasury bonds, which have a negative correlation in the latter, as shown in Figure 1, which can be very beneficial.

Figure 1: one-month moving correlation between stocks and U.S. treasury bonds.

In summary, including both types of assets, beyond individual preferences, can improve risk-adjusted returns, making them good candidates to be part of a portfolio. Obviously, it is also important to look at the return parameters.

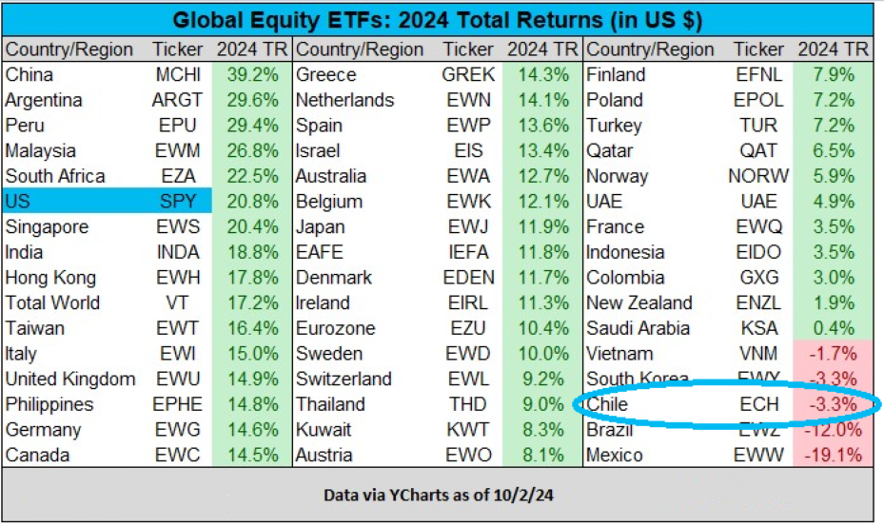

Image 2 shows the performance of the main stock indexes in various markets.

Figure 2: return of stock indexes around the world, measured in US dollars.

It is interesting to highlight Chile's position, compared to other selected markets. And this point, together with those previously mentioned in other newsletters, makes national equities a very interesting entry point ad-portas -in addition- to a significant choice.

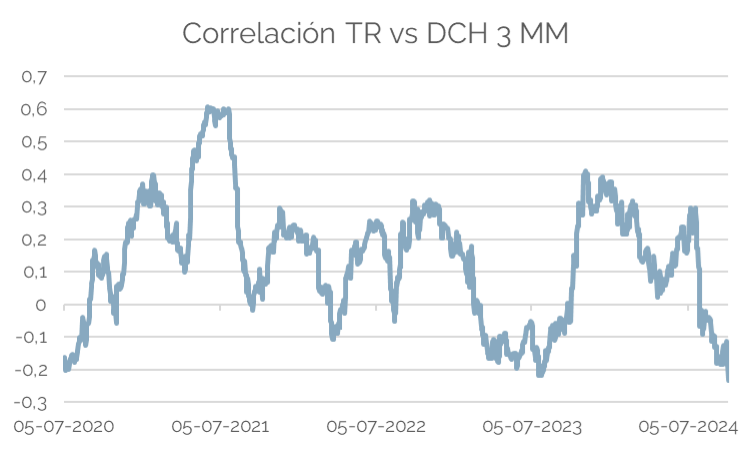

In this context, and in light of the above, we reviewed how we could apply these principles to our local market. We did so through our domestic fixed income (Deuda Chile, denoted as DCH) and equity (Total Return, denoted as TR) funds. Figure 3 shows the results.

Figure 3: Correlation between Deuda Chile and Total Return funds (domestic fixed income and domestic equities)

Finally, we can observe which correlation is at minimum levels, being in the valuable negative zone and being able to generate attractive strategies by combining both assets.