So far this year, the markets have been able to cope with higher interest rates because the combination of economic data has been favorable, with upward surprises in economic activity and downward surprises in inflation, and upward revisions to companies’ expected earnings as recession risks recede have done the rest.

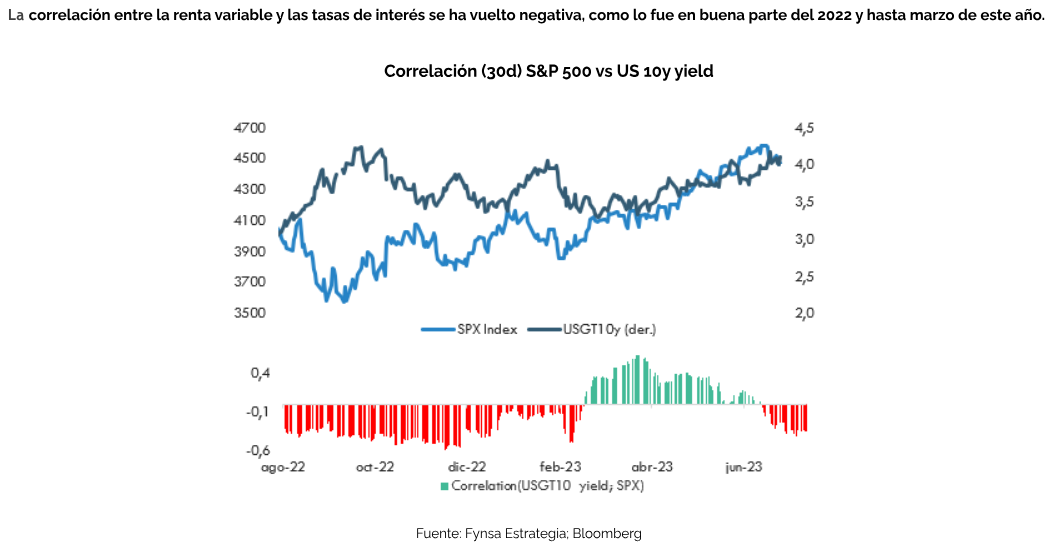

This has caused the correlation between interest rates and U.S. equities to turn positive since March, and helps explain the disconnect between historically stretched valuations and real interest rates trading at cycle highs.

But something has been changing in recent weeks. The markets have once again become more sensitive to rising interest rates, or, to put it another way, the correlation between equities and interest rates has turned negative, as it was for much of 2022 and through March of this year.

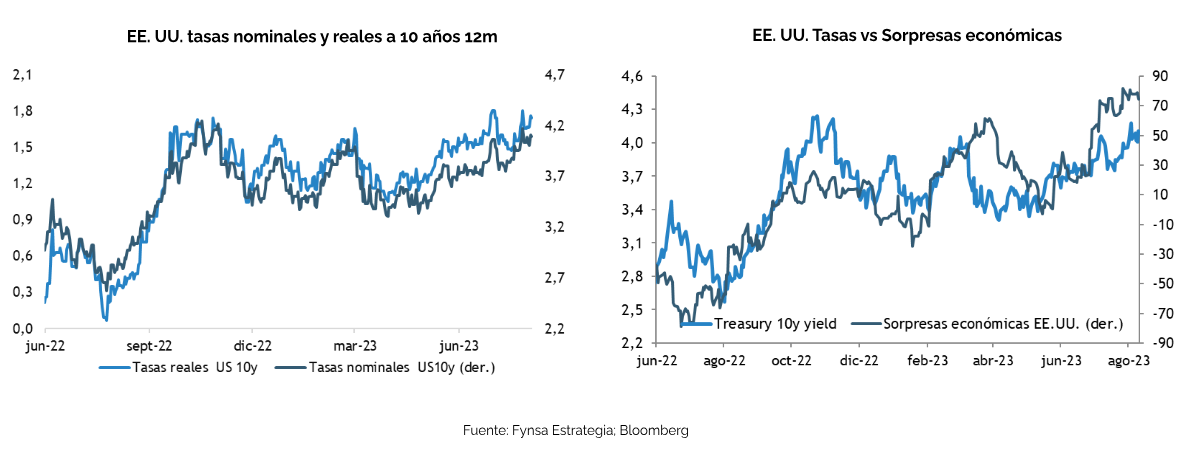

It has been a turbulent few weeks for bonds, with the 10-year U.S. Treasury yield reaching its highest level since November 2022, above 4.2%, while rates at the short end of the curve have remained fairly stable. While some of this renewed interest rate pressure at the long end of the curve reflects concerns over Fitch Ratings’ downgrade of the U.S. credit rating and a flood of Treasury bond sales to cover the federal deficit, it has also been driven by speculation that a resilient economy (the U.S. grew by 2.4% in Q2 2023, following 2.0% growth in Q1) will prevent inflation from returning smoothly to the Fed’s target, given the still-high levels of core indicators and longer-term expectations that remain more rigid.

In other words, what has been putting upward pressure on interest rates is an increase in the term premium, which also implies a steeper yield curve. With short-term inflation breakeven rates (up to 2 years) anticipating a more benign inflationary environment, longer-term inflation expectations tell a different story and remain elevated; as the charts below show, this generally leads to an increase in the term premium and, consequently, higher interest rates.

Furthermore, the moderate term premium levels also appear inconsistent with the degree of inflation uncertainty that still persists. Inflation volatility remains high.

Thus, Treasury bonds seem likely to fall again if it becomes clear that inflation isn't dead, but merely dormant. The same goes for stocks, as the rally continues to be driven by sectors and stocks with longer durations.

For now, the markets are in a delicate balance, and it will take some time to form a more definitive view on the future path of inflation, but the movements over the past two weeks serve as a good reminder that the U.S. market, in particular, has little room for error and is trading at near-perfect valuations (the S&P 500 is trading at a forward P/E of 20x and offers a premium of just 100 basis points over 10-year Treasury bonds).

A surprise uptick in inflation, a Treasury auction that isn't well received, Japan losing control of its yield curve, and a market correction that is still limited—it could turn out to be more severe.

If you're looking for guidance, just keep a close eye on interest rate trends.