The September Consumer Price Index (CPI) data in the United States exceeded expectations. The overall index rose 0.4% month-over-month and 8.2% year-over-year (one percentage point below August’s 8.3%). Meanwhile, the core CPI rose 0.6% month-over-month and 6.6% year-over-year (up from 6.3% in August), hitting a new multi-decade high. The persistent strength in inflation data (combined with continued tightness in the labor market) is keeping pressure on the Fed to continue tightening monetary policy.

Among the underlying components, September’s strength was concentrated in the services sector, with prices for basic services rising by +0.8%—the largest monthly increase for this aggregate since 1982—led by shelter (+0.7%), health care services (+1.0%), and transportation services (+1.9%).

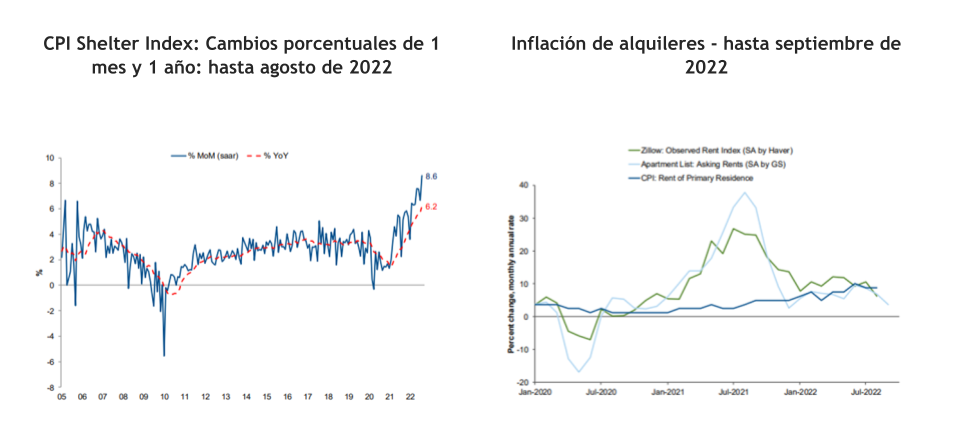

In particular, housing categories continue to strengthen (rent +0.84% vs. +0.74% in August; OER (owners’ equivalent rent) +0.81% vs. +0.71%). However, separate data reported by Zillow suggest that rent inflation will moderate at some point (at least relative to the particularly strong recent pace), but we may not see noticeably softer CPI data for at least a couple of months given the lag between these measures.

Housing inflation has risen significantly, but the pace of rent increases has slowed since the peak in mid-2021

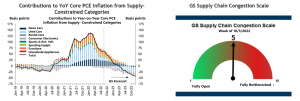

Meanwhile, prices for basic goods remained low in September, and this is where we will likely see the greatest relief from inflation as a result of the easing of supply chain constraints, falling energy prices, and a stronger dollar. The CPI for core goods remained essentially unchanged between August and September, and although the year-over-year change in the CPI for core goods remained strong in September (6.6% annually), this represented a sharp slowdown from the recent peak of 12.3% annually recorded in February. The moderation in auto price inflation has helped the broader core goods aggregate ease recently.

Meanwhile, prices for basic goods remained low in September, and this is where we will likely see the greatest relief from inflation as a result of the easing of supply chain constraints, falling energy prices, and a stronger dollar. The CPI for core goods remained essentially unchanged between August and September, and although the year-over-year change in the CPI for core goods remained strong in September (6.6% annually), this represented a sharp slowdown from the recent peak of 12.3% annually recorded in February. The moderation in auto price inflation has helped the broader core goods aggregate ease recently.

Excluding core components, energy prices fell 2.1% in September, while food prices rose +0.8%

Inflation will ease for goods with limited supply, and the significant appreciation of the U.S. dollar will also exert downward pressure on U.S. inflation

And while actual inflation—especially core inflation—shows no signs of letting up, consumers’ inflation expectations have declined, as have inflation breakeven rates

Finally, how will this affect interest rate expectations and the Fed's response?

Last week we noted that the problem facing monetary policy is that actual inflation—and especially core inflation—is proving to be far more persistent than expected, and this has forced the Fed to stand firm on the need to continue tightening in order to reduce inflation. SEE .

Of course, the September inflation data only reinforce the need to continue raising interest rates and offer little relief to the market, but given that there is a reasonable expectation of some moderation in inflationary pressures in the coming months, we continue to believe that we may be closer to a “peak” in terms of policy (prices today already price in a federal funds rate of close to 5% in Q1 2023).