Market narratives change rapidly. Just a couple of months ago, headlines pointed to an increasing likelihood of a recession not only in the U.S. but also globally. Against this backdrop, following an aggressive tightening of monetary policy, central banks were expected to pause soon… We were close to a “pivot” in policy.

The underlying logic behind expectations of a “Fed pivot” was based on the assumption that the focus of monetary policy would shift from inflation to growth—a dilemma that the Fed chair himself was supposed to have resolved in his Jackson Hole speech, where he promised to do whatever it takes to protect the economy from excessively high inflation, even if that comes at the cost of slower economic growth. READ MORE.

But if anyone still had any doubts that the U.S. Federal Reserve is focused above all on meeting its inflation target, those doubts were dispelled this week. Following the conclusion of the September FOMC meeting, it is now very clear that if the cost of bringing inflation back to target is economic pain, it is a cost the Fed is willing to accept.

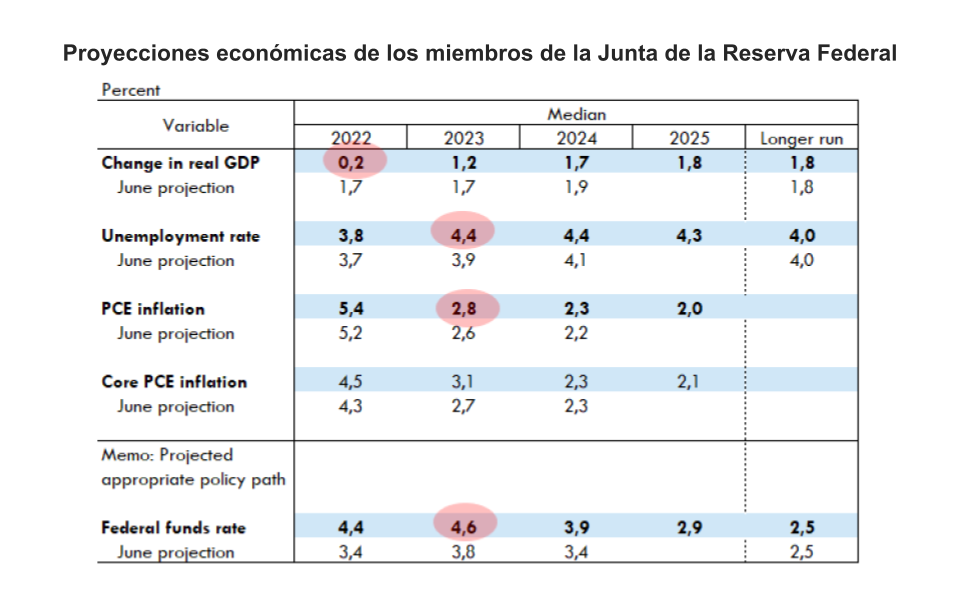

Furthermore, this is a cost that policymakers are increasingly factoring in. The median FOMC member now estimates that U.S. GDP growth for 2022 will be just 0.2%. In June, the median forecast was 1.7%. However, the deteriorating growth outlook and the prospect of rising unemployment did not deter the Fed from implementing another 75-basis-point rate hike and proceeding with plans to reduce its balance sheet.

But even more important than the 75-basis-point hike was the shift in the committee’s views regarding the future path of interest rates. Nearly two-thirds of the members now expect rates to peak next year, even higher than the 4.5% that markets had anticipated, and monetary policy is projected to be “restrictive” throughout the projection horizon.

The FOMC’s revised projections yielded two key takeaways from the September meeting. The dot plot showed a median projection of another 125 basis points of tightening this year and 25 basis points next year, implying that a 75-basis-point increase is the baseline for November, and the economic projections showed a higher peak unemployment rate, indicating a greater willingness to continue raising rates amid a weakened labor market if inflation remains high.

Ultimately, the path of the federal funds rate in 2023 will, of course, depend on how quickly growth, hiring, and inflation slow down. While there are risks in both directions, it seems more likely for now that a higher peak rate will be needed to cool the economy, rather than the Fed pausing sooner.

Asset Price Ranges and Strategies

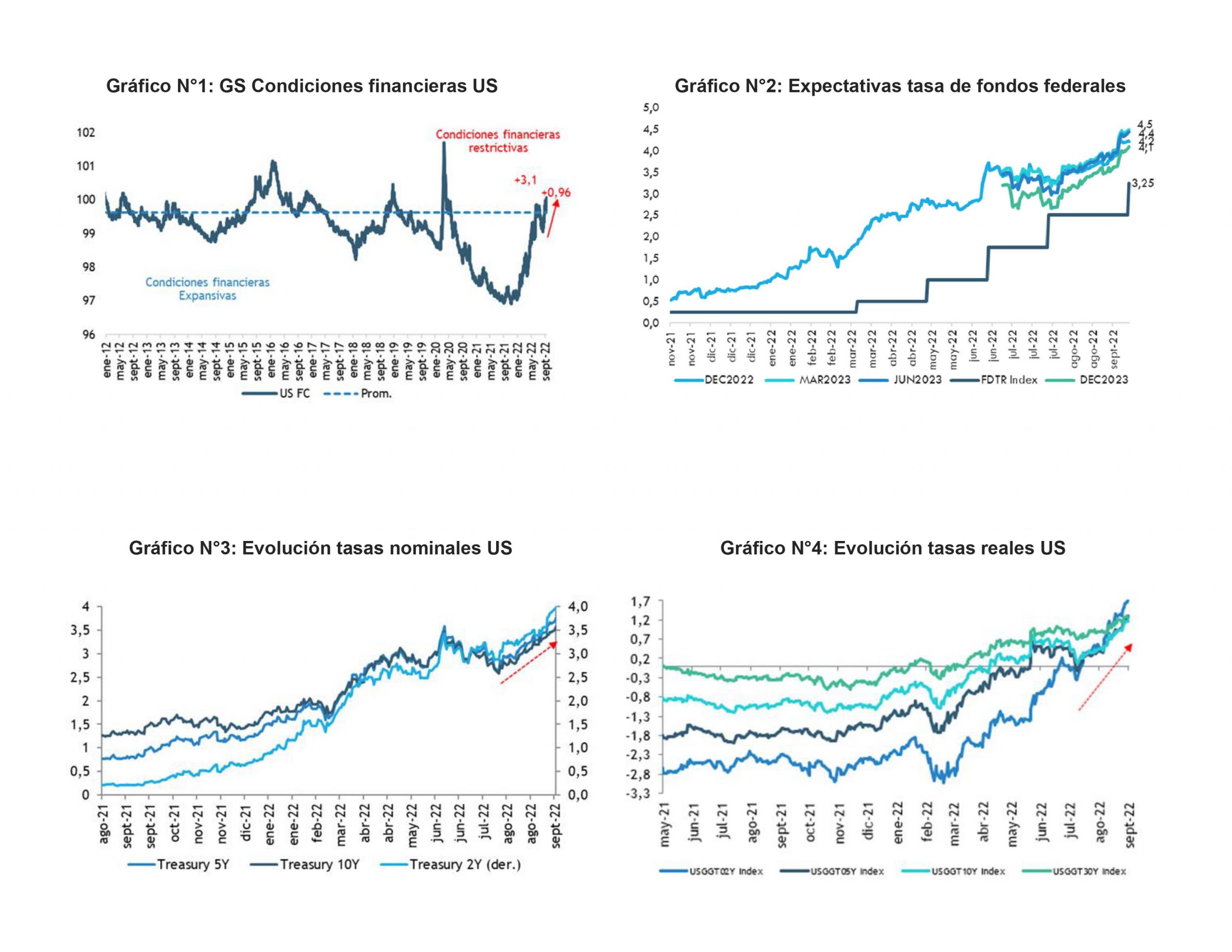

Financial conditions, after a temporary easing (which is what the Fed has been trying to correct) have tightened substantially again since Jackson Hole and will likely continue to do so going forward.

Expectations for the federal funds rate have been aligning with the Fed’s projections, and market rates have risen across the board over the past 30 days (10-year UST +50 bp, 2-year UST +74 bp). We still see at least a 50-bp tightening ahead, which would put the 2-year UST on track for 4.5% and the 10-year UST at 4.0%, keeping the yield curve inversion at around 50 bp. Meanwhile, real rates are firmly in positive territory.

Financial conditions will continue to tighten

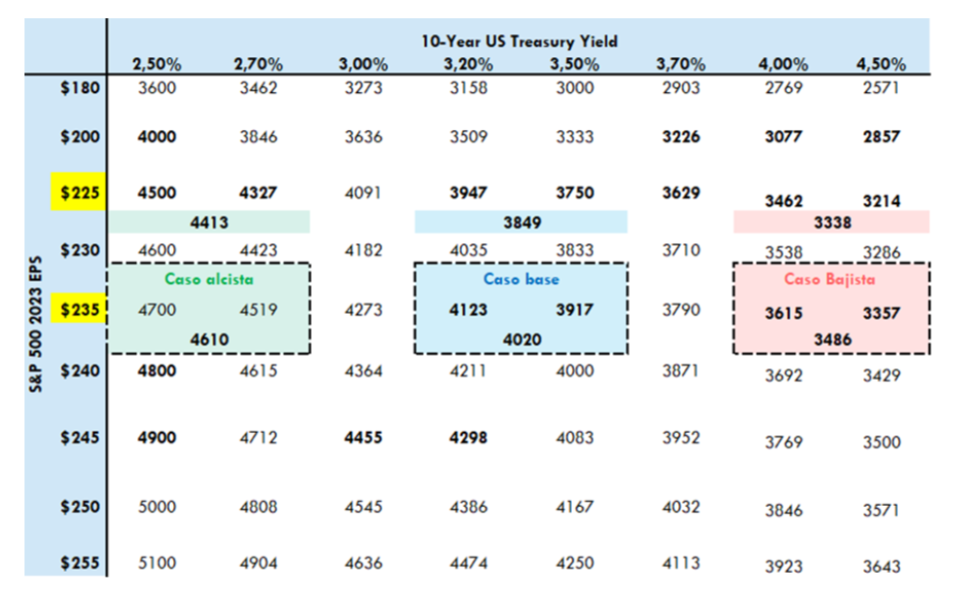

These higher interest rates would continue to put pressure on equity valuations, at a time when there remains some divergence in interest rate levels and equity market performance.

In this context, the risks of further sell-offs have increased. For valuations to appear truly attractive, the S&P 500 would need to fall another 10% to trade at 14x forward P/E (bearish scenario).

S&P 500 forecast for the end of 2022 based on estimated earnings per share for 2023, the 10-year Treasury yield, and a yield gap of 2.5%

In a more complex environment for risky assets, the market today offers a range of high-yield, low-volatility alternatives for diversifying portfolio risk. Cash and short-term fixed-income securities increasingly offer lower volatility and high returns for risk diversification. Six-month U.S. Treasury bills yield approximately ~3.8%, and U.S. credit yields for 1- to 5-year maturities stand at ~4.9% (2.5-year duration), compared with the S&P 500’s earnings yield of ~6.0%. However, over the past 30 days, the S&P 500 has been nearly six times more volatile.

In a more complex environment for risky assets, the market today offers a range of high-yield, low-volatility alternatives for diversifying portfolio risk. Cash and short-term fixed-income securities increasingly offer lower volatility and high returns for risk diversification. Six-month U.S. Treasury bills yield approximately ~3.8%, and U.S. credit yields for 1- to 5-year maturities stand at ~4.9% (2.5-year duration), compared with the S&P 500’s earnings yield of ~6.0%. However, over the past 30 days, the S&P 500 has been nearly six times more volatile.

Finally, we believe these dynamics will continue to support the USD (where sovereign rates are higher).