The industrial warehouse market in Santiago has been characterized as relatively stable, and historically linked to logistics and trade activity. However, this industry changed as a result of the pandemic, the acceleration of e-commerce and adjustments in supply chains, which accelerated demand, reduced vacancy to historic lows and encouraged the rapid development of new supply. Today, with demand beginning to moderate and supply growing, the sector is entering a stage of greater balance and normalization.

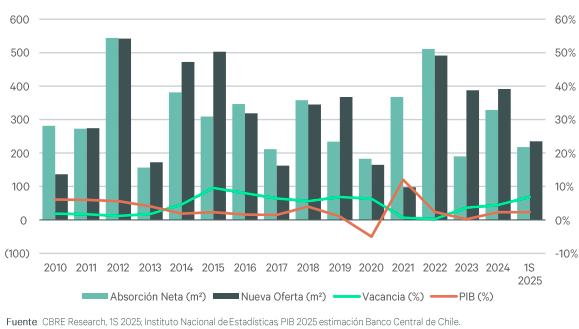

According to the latest CBRE report, during the first half of 2025, 235,160 m2 of available stock were added to the available stock, distributed in 9 new projects and 1 expansion of an existing center.

Net absorption for the period was 69,167 m2, a drop of 53% compared to the previous semester, and 62% compared to the first half of 2024. Forty-seven percent of net absorption was located in the West zone, followed by the South zone, with 36% of the total.

Despite this, average lease prices remained relatively stable at around 0.164 UF/m2 , with a slight decrease of 3.04% compared to the previous semester. It is worth noting, however, that average prices fell after 3 consecutive semesters of increases, which is mainly attributed to spaces becoming available again after long periods under contract.

The vacancy rate reached 6.89%, 2.44 percentage points above the previous half year and 2.1 percentage points above the same period of the previous year. This figure represents its highest point since 2022, driven by a low pre-placement of new developments that have entered the market, which are entering with pre-placement levels of around 60%, whereas previously this indicator reached almost 100%.

Analyzing the behavior of the different submarkets of Santiago, we note that the Poniente and Norte submarkets stand out for their high concentration of new supply, which has contributed to higher-than-average vacancy levels. On the other hand, the Norponiente submarket maintains low levels of availability, confirming its attractiveness for users who value logistical access and competitive conditions. The South submarket continues to show healthy vacancy levels, while Central-East, despite its lower volume, retains a strong demand for its premium profile, which is why it shows the highest average lease levels.

Looking ahead to the second half of the year, the market faces a challenging scenario: the total pipeline exceeds 1,000,000 m2 between projects under execution and those with approved permits. The market's absorption capacity and the quality of the projects that come into operation will be key, and in this sense, well-located developments with flexible design and modern technical characteristics will be the best positioned to face this new cycle.

In summary, the warehouse market in Santiago shows clear signs of stabilization after years marked by accelerated growth, driven by e-commerce and the reorganization of post-pandemic logistics chains. This stabilization, which translates into higher levels of availability, has generated a more favorable environment for end users, who can now choose from a wider and more varied offer in terms of space size and characteristics.

Sebastian Mahave

Portfolio Manager Real Estate Fynsa AGF