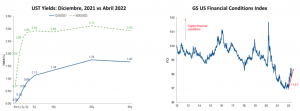

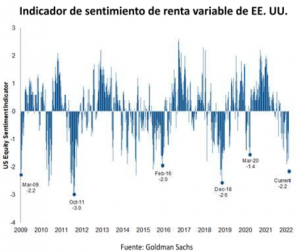

La narrativa que prevalece en los mercados financieros es que la Reserva Federal (Fed) está significativamente retrasada en su política monetaria y que, al acelerar su ritmo de alza de tasas, provocará casi inevitablemente una recesión en EE.UU. Esto explica que el S&P500 haya bajado aproximadamente 10% en el año.

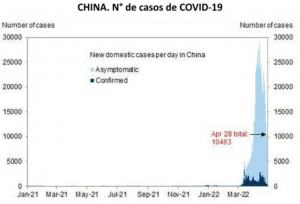

Por supuesto estos temores se han visto retroalimentados por los riesgos geopolíticos y más recientemente por la expectativa de que la demanda china se derrumba debido a los bloqueos.

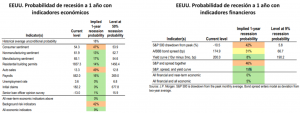

Esta semana queremos destacar varios puntos que contradicen la visión dominante en el mercado:

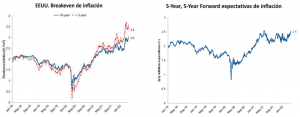

Entre tanto, las medidas de expectativas de inflación también respaldan la opinión de que la Reserva Federal no se percibe tan “retrasada” como sugieren algunos observadores del mercado. Las tasas de inflación de equilibrio, medidas por el diferencial entre los valores del Tesoro protegidos contra la inflación (TIPS) y los bonos del Tesoro con vencimientos comparables, se sitúan en 3,4 % para los bonos a 5 años y en 3,0 % para los bonos a 10 años.

Otra medida a largo plazo, la estimación de los mercados de cuáles serán las tasas de equilibrio de 5 años, 5 años forward, muestra las expectativas de inflación en 2.5%, que es solo modestamente superior al objetivo de 2% de la Reserva Federal considerando que el IPC ha superado históricamente la medida de inflación PCE preferida por la Reserva Federal en unos 30 puntos base.

Los detalles de una reunión del Politburó esta semana, compromete más apoyo político para cumplir con el objetivo de crecimiento económico del país para el año.i) fortalecer los ajustes macro, ii) apoyar el crecimiento saludable de las empresas de plataforma, iii) planificar herramientas de políticas incrementales, iv) hacer esfuerzos para impulsar el consumo interno y v) impulsar un desarrollo saludable del mercado inmobiliario. Los líderes chinos también se comprometieron a garantizar “cadenas de suministro en sectores clave” y una logística de transporte fluida, comprometiéndose a “responder positivamente” a las demandas de las empresas con inversión extranjera para un entorno operativo comercial más fluido.

La última promesa de estímulo se produce solo unos días después de que el presidente de China, Xi, destacara la infraestructura como un gran enfoque para el gobierno a medida que el crecimiento está bajo presión.

Con todo, si se evita una recesión (caso base por ahora), la historia nos demuestra que permanecer invertido en acciones es la estrategia correcta. Sin embargo, incluso si se produce una recesión en los próximos años, es demasiado pronto para reducir la exposición accionaria.