We see greater opportunities in a defensive strategy in terms of duration and credit risk, with an overweight position in UF

Share

OVERVIEW SUMMARY

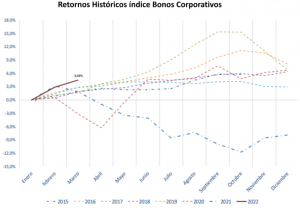

After a year to forget in 2021, it has been a good start to the year for the local fixed-income market. During the first quarter, the major fixed-income indices posted positive returns above their historical averages.

The attractive interest rate differentials that have drawn foreign capital inflows, the perceived shift by the new government toward prioritizing “fiscal responsibility,” combined with the attractive returns offered by this asset class following the rate hikes observed in recent months, have contributed to this trend.

Looking ahead, we project high inflation rates, which will increase the appeal of UF-indexed instruments. The real yield curve with a duration of around 2 years is where investors should position themselves to hedge against inflation.

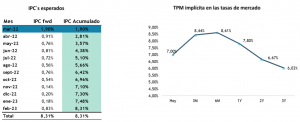

Market rates already reflect the expectation that the Central Bank will continue to raise the TPM over the next three months, but we are likely nearing the end of this tightening cycle.

Among the risks, the constitutional reform process—which has been more radical than expected—stands out. Added to this today is a proposed fifth withdrawal from the AFPs. Given this, the political landscape will continue to be one of the key factors for this asset class moving forward.

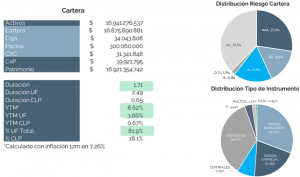

Our Fynsa Deuda Chile fund maintains an attractive risk-return profile, through a defensive strategy that prioritizes a shorter duration (1.7 years) and high-quality issuers to reduce volatility, while maintaining YTM levels (around 8.6%).

RETURNS

During the first quarter of the year, returns on the major fixed-income indices have posted positive returns above their historical averages.

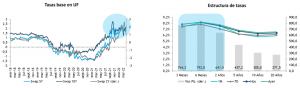

LOCAL TAXES

Local rates in 2022 have regained some of the historical correlation they had with their counterparts in the U.S. economy. Domestic rates remained under slight upward pressure during the first quarter, in line with international rates.

Over the past 12 months, the yield curve has risen sharply, especially for maturities close to 1 year, creating opportunities for attractive risk/return positioning.

INFLATION AND TPM

The market is forecasting high inflation rates for the coming months, which increases the appeal of UF-indexed instruments.

Market rates already reflect the expectation that the Central Bank will continue to raise the TPM over the next three months, but we are likely nearing the end of this tightening cycle.

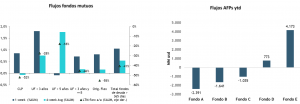

INVESTMENT FLOWS

Increased institutional and retail demand

INVESTMENT DRAWDOWN: Fynsa Chile Debt Fund

Defensive strategy, prioritizing shorter duration (1.7 years) and high-quality issuers to reduce volatility, while maintaining YTM levels (around 8.6%). For more details, see HERE

Humberto Mora

Investment, Finance, and Business Manager; Stockbroker