With high inflation, the Federal Reserve’s accelerated rate-hiking cycle, and the inversion of the U.S. yield curve, investors are increasingly concerned about the risk of a recession.

Predicting recessions is difficult: while the yield curve has historically inverted before recessions, it has been less useful for timing them. Current high inflation could trigger an earlier and deeper inversion. Since the late 1980s, the lag between yield curve inversion and U.S. recessions has averaged 20 months, so it can serve as an early warning sign. That said, false signals are common. In periods of high inflation, the yield curve has inverted by between 100 bp and 200 bp before a recession, and even a mild inversion can generate a false signal.

Monitoring a broader range of market indicators—including cyclical versus defensive valuations, credit spreads, and federal funds rates—could help gauge the risk of a future recession.

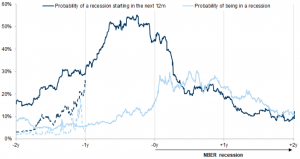

Some indicators based on market-based indicators are leading indicators—the most well-known being the yield curve—while others, such as risky assets, react primarily during or at the onset of recessions. (see footnotes)

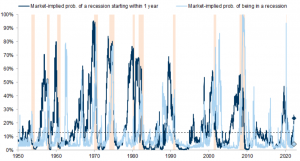

As Goldman Sachs notes, the combination of indicators could provide a better signal: So today andn average, both leading and coincident indicators have risen so far this year, but they are not currently placing much weight on the risk of a recession.

Source: Goldman Sachs

Source: Goldman Sachs

Source: Goldman Sachs

Source: Goldman Sachs

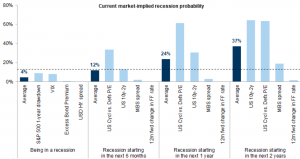

The current market-implied probabilities of a recession are still below the levels that would normally signal a recession. When combining different segments of the yield curve, the market is pricing in a low probability of a recession over the next 12 months, but a 38% probability over 24 months. Historically, cyclical versus defensive valuations have given some false signals; recently, they have likely also been affected by rising commodity prices and supply chain disruptions, rather than just the risk of a recession.

All in all, based on the average of leading and coincident indicators, the current risk of a recession implied by the market does not appear to be very high, especially following the recent strong recovery in risk assets; coincident indicators suggest that markets have priced in a lower risk of an imminent recession.

Source: Goldman Sachs

Source: Goldman SachsNotes: