In recent days, an agreement between the government and part of the opposition has pushed forward an eventual pension reform in Chile. This reform considers multiple changes in the structure of the Pension System, such as the ownership of contributions, implicit labor costs and its general administration, including the transition from multifunds to Generational Funds (GF).

This represents a significant structural transformation for the way in which pension funds are managed, as the DGs, similar to the "Target-Date Funds", have been able to provide a more efficient way of managing pension funds.Target-Date FundsThe FGs, similar to the "Target-Date Funds" in the U.S., dynamically adjust the composition of portfolios according to the age of the members, better aligning investments with the life cycle and risk profile of the individual.

A new model

The Generational Funds focus on dynamic investment strategies that evolve over time, progressively reducing exposure to equity assets as contributors approach retirement age, thereby optimizing the risk-return ratio and reducing the sub-optimality of the current Multifunds scheme.

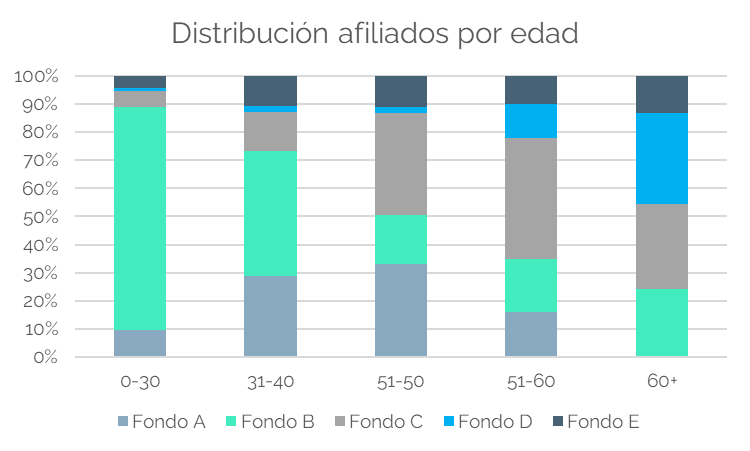

This new approach responds to a central problem identified by the Superintendence of Pensions, which estimates that about 51% of members are in funds that do not fit their risk profile or investment horizon (see Figure 1). (see figure 1).

Figure 1: Distribution of affiliates, Superintendency of Pensions.

Figure 1: Distribution of affiliates, Superintendency of Pensions. The transition to this model implies significant adjustments in the composition of investment portfolios. In this regard, it is important to look at the distribution of funds: only 30% are invested in conservative funds (D and E), despite the fact that almost 60% of the funds correspond to people over 50 years of age (see Figure 2).

This structural change will increase demand for local fixed income assets, especially Treasury bonds. In contrast, a disinvestment in foreign equity assets is expected, reflecting a shift in focus towards greater investment stability. Some estimates indicate that the magnitude of these changes would be close to US$50 billion, i.e. 16% of GDP..

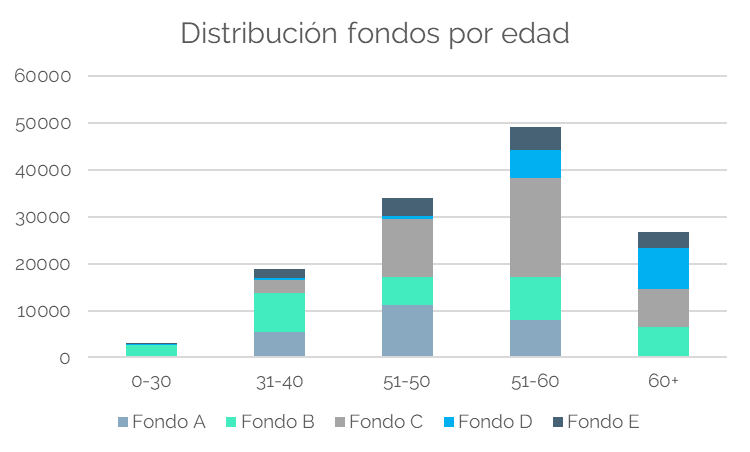

Figure 2: Distribution of investment in funds, Superintendency of Pensions.

Figure 2: Distribution of investment in funds, Superintendency of Pensions. International experience, such as the transition in Mexico, offers valuable lessons for Chile. In Mexico, the retirement fund managers (Afores) managed 16% of GDP, while in Chile it is over 50%. In the Aztec country, 10 generational funds were established, with spaces for alternative assets, and the concept of tracking error was introduced. The assets were mostly invested in fixed income and there was not such a relevant sub-optimality regarding the investment of the funds, as in Chile (see Figure 3).

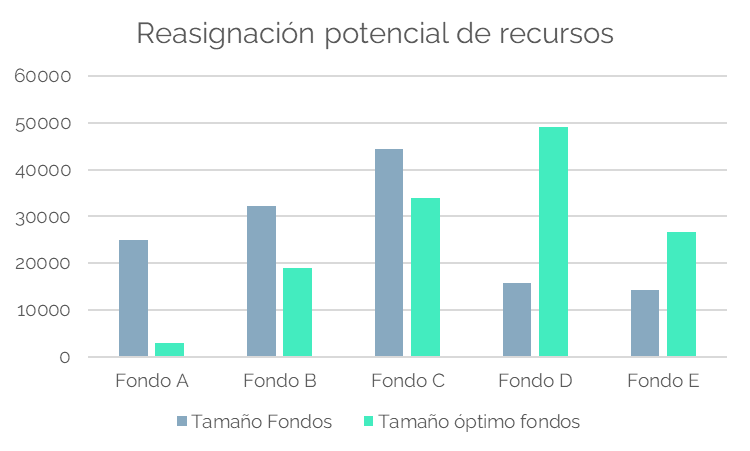

Figure 3: Estimated reallocation of funds to optimum according to distribution.

Figure 3: Estimated reallocation of funds to optimum according to distribution. In addition to the initial adjustment in the portfolios, the annual flows derived from the contributions will also play a fundamental role in the consolidation of this new scheme. With the increase of 4.5 percentage points to mandatory contributions, together with the restructuring, the magnitude of flows to fixed income would increase to a greater extent.

Gradual implementation and rigorous oversight will be key to minimize risks and maximize benefits. Aspects such as the definition of asset transfer pricing, the effect on sovereign interest rates and exchange rates, and the potential increase inhome bias will be critical issues for regulatory authorities to consider.

Likewise, the introduction of mechanisms for the transfer of ownership of financial instruments without directly affecting the secondary markets will be a determining factor in guaranteeing an efficient and stable transition.

However, this represents opportunities and challenges for improving the pension system, aligning investments with the risk profiles and horizons of contributors, including adjustments in investment portfolios, impacts on asset prices and the need for rigorous supervision.

In the long term, this change could strengthen the financial system and generate greater stability for members, contributing to greater sustainability of the pension system. It is important to consider that this analysis focuses exclusively on the contribution to the individual accounts, without reviewing the public aspects of the reform and the percentage decrease that this will bring about in the pension system.It is important to consider that this analysis focuses exclusively on the contribution to individual accounts, without reviewing the public aspects of the reform and the percentage reduction that this will bring about in the individual contributions of the contributor, which, since they are invested in a government loan, will already represent a percentage of investment in fixed income, which may mitigate the mobility effect.

***Disclaimer: The graphs and data used correspond to an extrapolation of the 5% sample of random members provided by the superintendence of pensions, so the values should be considered as a reference.

Gabriel Haensgen

Senior Analyst Fynsa Financial Funds AGF

{kind=link}