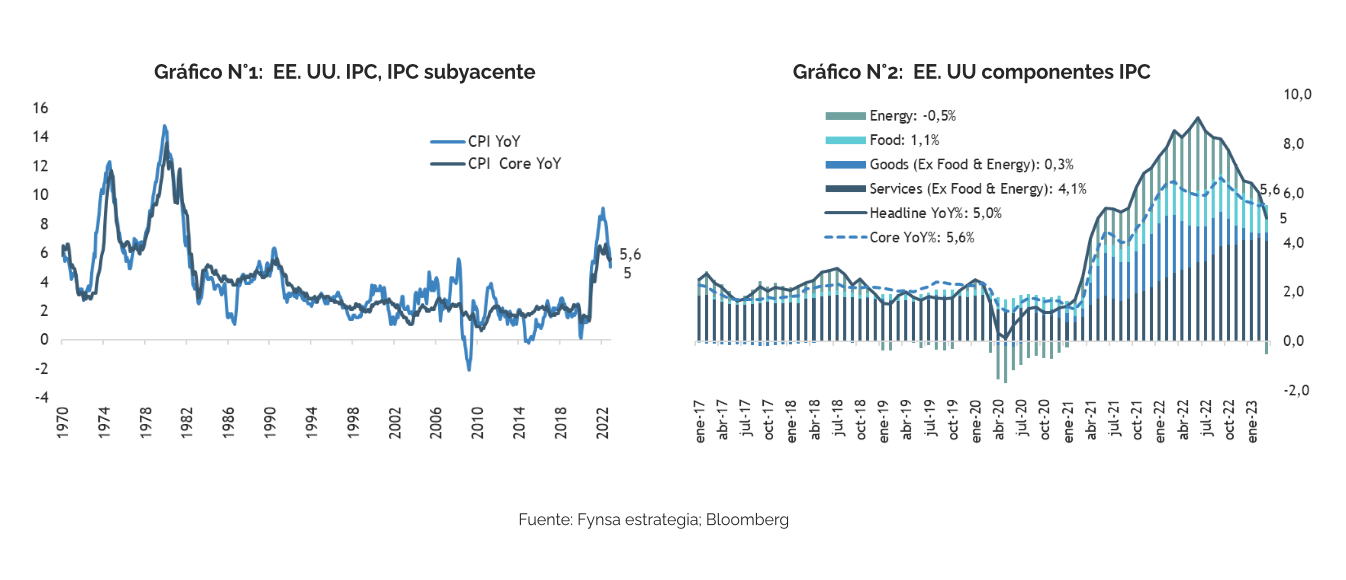

U.S. headline inflation for March came in below expectations, although core inflation was more in line with market forecasts. The CPI for March rose by only 0.1% (or 0.053%), 0.1% below expectations, bringing the year-over-year figure down from 6.0% to 5.0%. The CPI excluding food and energy rose 0.4% (or 0.385%), bringing the year-over-year figure from 5.5% to 5.6%. The softer overall figure was driven by flat food prices—the lowest reading since mid-2020—while energy prices fell by 3.5%. (see Charts 1 and 2)

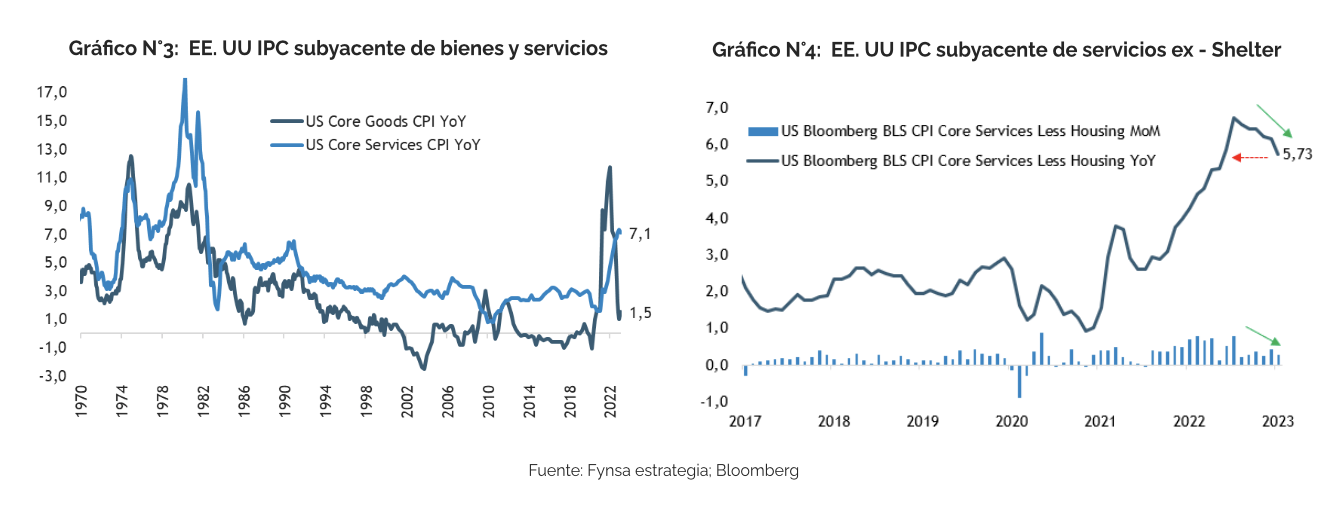

As for goods inflation, it rose in March after seven months of decline (+0.2% MoM; +1.5% YoY), while services inflation slowed modestly from +7.3% year-over-year to +7.1% year-over-year, But this slowdown is a significant sign, as it comes after nine months of strong growth. (see Figure 3).

As for goods inflation, it rose in March after seven months of decline (+0.2% MoM; +1.5% YoY), while services inflation slowed modestly from +7.3% year-over-year to +7.1% year-over-year, But this slowdown is a significant sign, as it comes after nine months of strong growth. (see Figure 3).

Perhaps the most encouraging sign is that housing inflation may have begun to peak:

The inflation indicator currently most closely watched by the Fed—the so-called “Super-Core”: Core Services Excluding Housing—slowed to a year-over-year rate of 5.73%, the lowest level since July 2022 (see Chart 4), offering some evidence that the trend in core inflation is shifting in a more comfortable direction, so it would be reasonable to conclude that the Fed could adopt a wait-and-see approach at its next meeting, which would effectively end the tightening cycle.

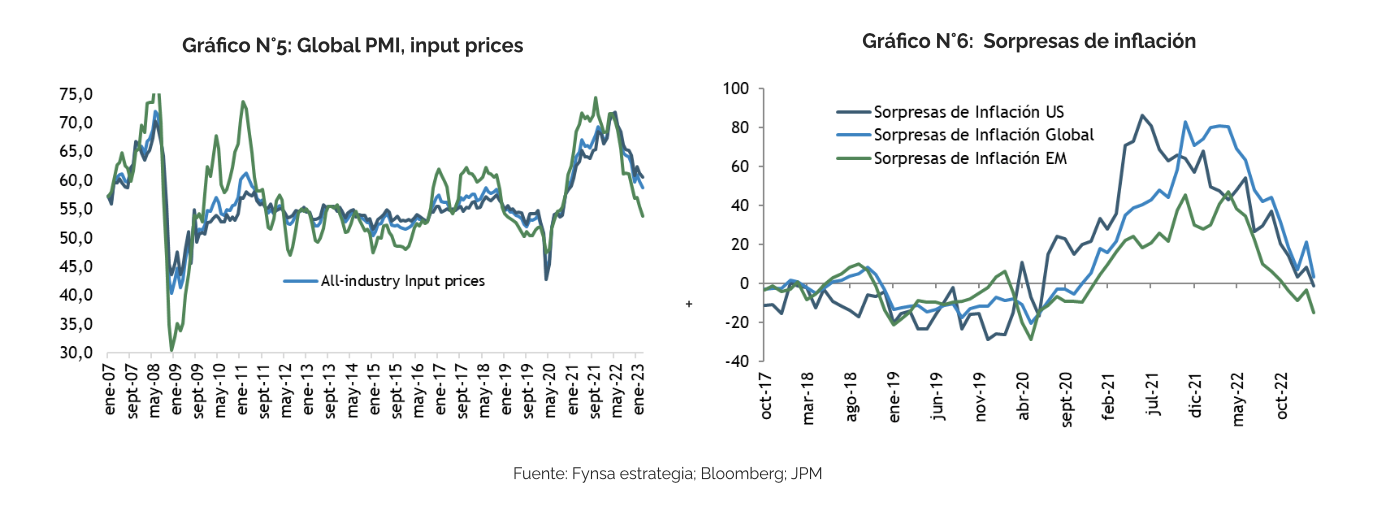

In addition, a key finding from the latest PMI (Purchasing Managers’ Index) surveys is that companies’ pricing power is waning this year compared to the multi-decade-high core inflation rates observed last year. The PMIs show that last year’s extreme price pressures are fading rapidly. However, the decline in services is occurring at a much slower pace than in manufacturing. Overall, the all-industry price PMI remains above the highs recorded during the previous expansion.

In addition, a key finding from the latest PMI (Purchasing Managers’ Index) surveys is that companies’ pricing power is waning this year compared to the multi-decade-high core inflation rates observed last year. The PMIs show that last year’s extreme price pressures are fading rapidly. However, the decline in services is occurring at a much slower pace than in manufacturing. Overall, the all-industry price PMI remains above the highs recorded during the previous expansion.

This is consistent with the view that core inflation will ease this year but will not fully return to the central bank’s comfort zone, keeping monetary policy rates high for longer—assuming the Fed achieves a “soft landing.” However, the combination of higher borrowing costs and the tightening of credit conditions that will inevitably result from the fallout of recent banking tensions increases the risk of a “hard landing.” This would make it even more likely that inflation will return to the 2% target sooner than expected. See more.

And take a look at what Figure 6 shows, which measures inflation surprises across different regions. The market underestimated overall inflation for virtually all of 2021. Well, headlines aside, what we have in practice is that over the past 12 months the market has overestimated inflation, and will likely continue to do so based on the logic of “more resilient demand” given that labor markets are still in good shape.

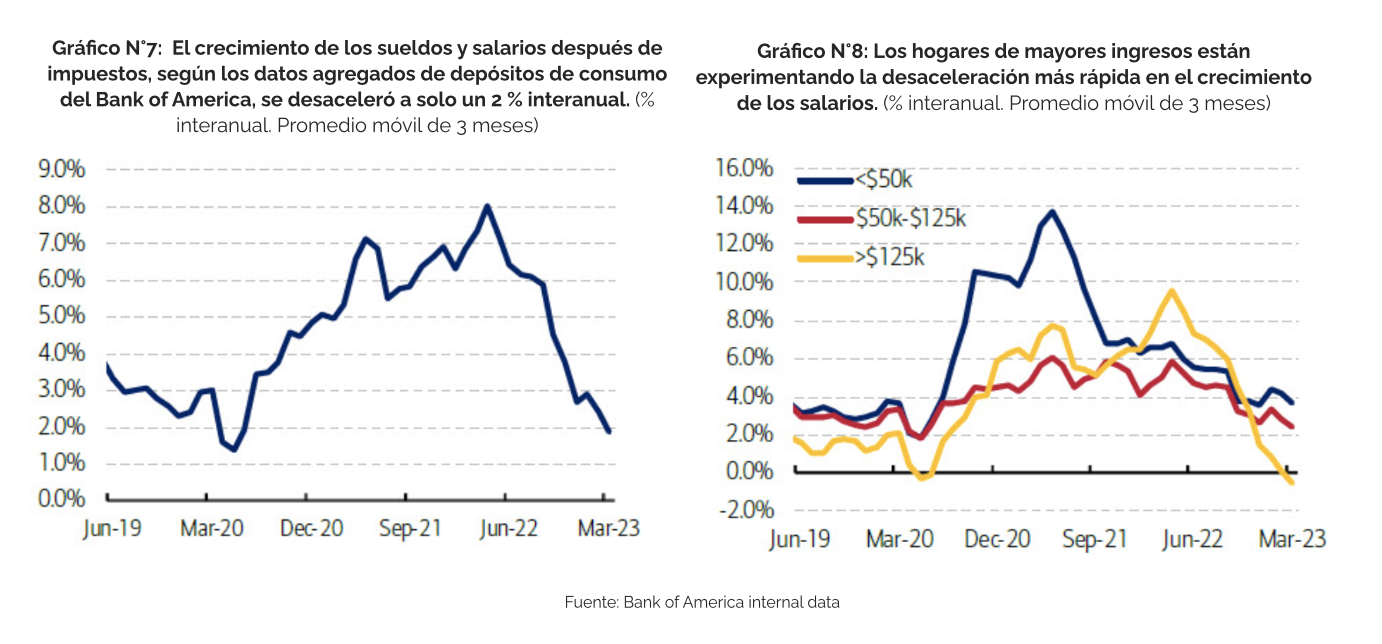

We’ll save a discussion of just how strong the labor markets are—particularly in the U.S.—for another time, but since today’s focus is on inflation, here are some wage data from a recent Bank of America study, which differ from the official figures in U.S. employment reports, and which show that wage growth, like real wages, is in free fall: “Growth in after-tax wages and salaries, according to BofA deposit data, slowed to just 2% year-over-year in March, on a 3-month moving average basis, down from a peak of 8% in April 2022—the lowest level since June 2020.” (see Figures 7 and 8)

We’ll save a discussion of just how strong the labor markets are—particularly in the U.S.—for another time, but since today’s focus is on inflation, here are some wage data from a recent Bank of America study, which differ from the official figures in U.S. employment reports, and which show that wage growth, like real wages, is in free fall: “Growth in after-tax wages and salaries, according to BofA deposit data, slowed to just 2% year-over-year in March, on a 3-month moving average basis, down from a peak of 8% in April 2022—the lowest level since June 2020.” (see Figures 7 and 8)