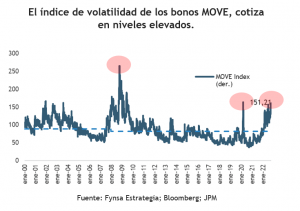

U.S. Treasury yields continue to rise amid a resilient labor market, an aggressive Fed, another inflation surprise (SEE MORE) and ongoing volatility in other DM government bond markets (especially the UK). Add to that a backdrop of low liquidity and limited demand, and you’ll find little evidence of market normalization.

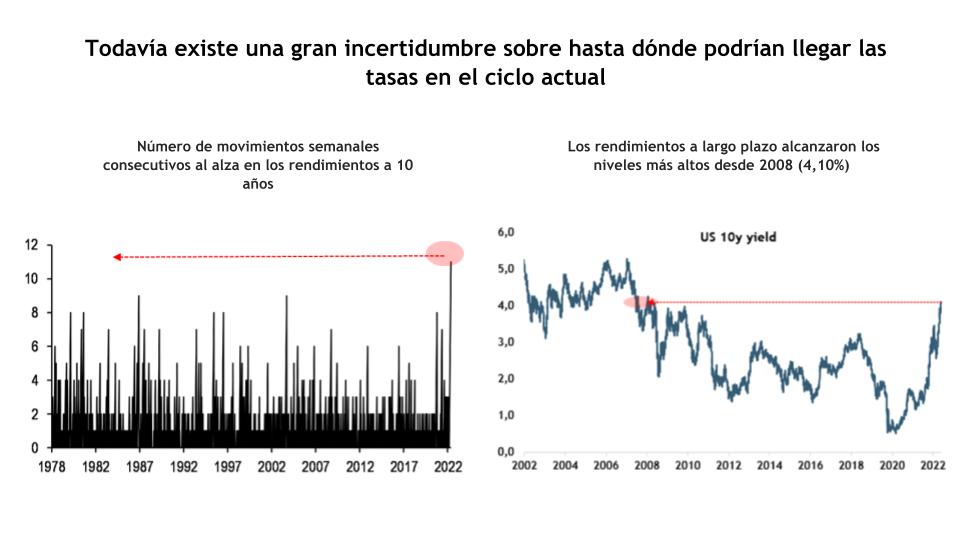

And given the way things are shaping up this week, the fixed-income markets are set to reach a new milestone, with 12 consecutive weeks of rising intermediate-term yields—the longest streak of increases in more than four decades; and there is still significant uncertainty about how high rates might go in the current cycle, which does not encourage risk-taking, particularly as we approach year-end. In fact, given the high level of uncertainty surrounding macroeconomic policy, it is not surprising that risk appetite remains low and that investors are unwilling to anticipate the shift toward higher yields amid high volatility.

Our base case continues to assume that the FOMC could slow the pace of tightening at some point in the future, and we believe that inflation will eventually moderate. However, the available data suggest that the Fed still has more work to do to ensure that inflation returns to target.

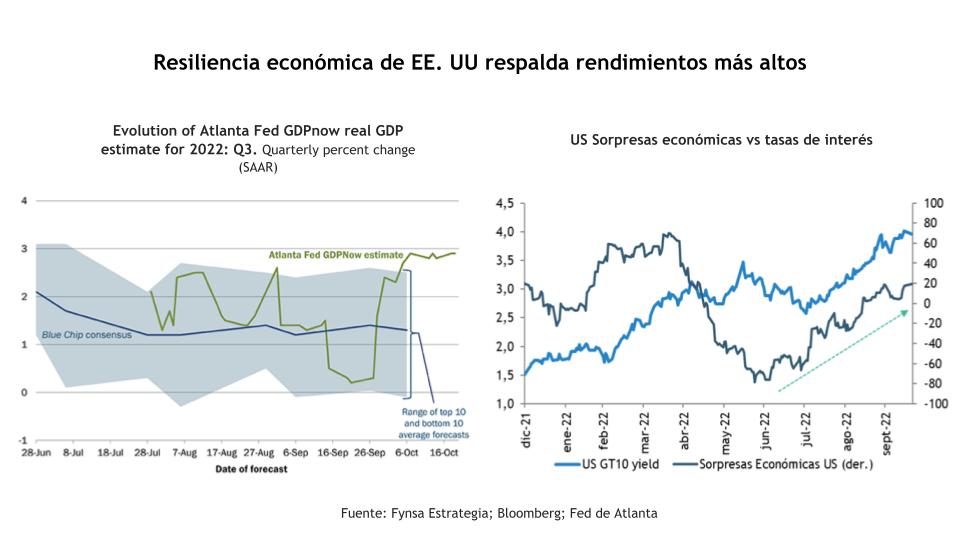

If anything has been surprising so far, it is the resilience of the U.S. economy, which appears to be gaining strong momentum as the year comes to a close, (Data recently released by the Atlanta Fed suggests that growth in Q3 2022 is likely to be closer to 3%), and aggregate economic data has generally been better than expected, which, all else being equal, supports higher yields.

On the flows and liquidity front, the lack of demand from buyers who have traditionally been price-insensitive by nature—including U.S. banks and foreign official investors—along with continued outflows from bond funds, and the Fed’s ongoing balance sheet reduction, all contribute to the reasons why Treasury bonds could become even cheaper relative to current valuations.

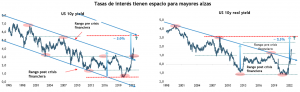

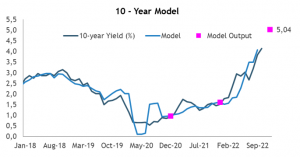

The technical indicators do not look promising either. During this adjustment cycle, key technical levels have been breached time and again, leaving behind the trading ranges that dominated interest rates during the deflationary period following the financial crisis up until the pandemic. The relevant reference levels on the upside are closer to 5% for 10-year nominal rates and 2.5% for 10-year real rates.

Those levels are consistent with a more fundamental model that takes into account inflation, growth, the federal funds rate, and the Fed’s balance sheet, which points to levels of 5% for the nominal 10-year rate, given current economic conditions and federal funds rate expectations.

Thus, for fixed-income investors seeking some relief, there is little evidence of market normalization, especially given the duration risk that still persists. That said, the short end of the sovereign yield curve is trading at its highest levels in 15 years (a 3-month Treasury is approaching 4% and a 6-month Treasury is approaching 4.5%), and we believe this part of the Treasury yield curve offers value, particularly in a world where equities and fixed income have experienced losses of 15%–20% this year.

Finally, how do these interest rate risks interact with equities? As we have noted on several occasions, much of the equity market’s losses so far this year can be attributed to the compression of multiples resulting from higher discount rates. In this regard, if real rates were to trade in the 2.25%–2.50% range, that would be consistent with a forward P/E multiple closer to 14x for the S&P 500—a valuation level we have cited as evidence that this bear market is beginning to run its course.