Core inflation in the U.S. slows more than expected

The "more positive" news on inflation has been well received and will revive trade based on a "policy pivot".

Share

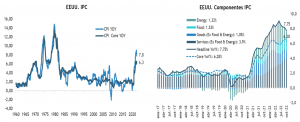

The U.S. Consumer Price Index (CPI) for October came in lower than expected. The overall index rose 0.4% (vs. an estimate of +0.6%), despite a 1.8% increase in energy prices and a 0.6% increase in food prices.

But even more significant was the downward surprise in core inflation, which rose by only 0.3% (versus an estimate of +0.5%), with the year-over-year rate falling by three-tenths of a percentage point to 6.3%. In particular, services inflation also slowed more than expected, with housing costs rising at their slowest pace since May and moderation in some wage-sensitive service categories, including hospital services, daycare, and personal care.

Prices for basic goods were particularly weak, falling 0.4% in October, and it appears that some of the factors that drove inflation over the past year have begun to ease or reverse. Two areas that stand out in particular are vehicle prices and healthcare service prices. An increase in the supply of vehicles has likely helped ease price pressures recently, and the CPI for new and used vehicles fell by 0.9% in October after an average monthly increase of 0.8% over the previous twelve months.

Overall CPI at 7.7%, down from 8.2% in September and the “lowest” level since January. Core CPI also slowed slightly.

The slowdown in core inflation is good news for the Fed. Policy makers have indicated that their preferred next step would be to slow the pace of rate hikes to 50 basis points at the December FOMC meeting. Indeed, the futures markets are pricing in 50-25-25 basis points for the next three meetings. Thus, the market believes there are about 100 basis points left before the Fed concludes the tightening cycle with a terminal rate of around 5%.

The interest rate market has lowered expectations for the terminal rate to just under 5%. Inflation expectations are falling

Market Reach

Incidentally, the market’s reaction to the “more positive” news on inflation has been well received and will reignite trading based on a “policy pivot.” Market rates have responded with a 25-basis-point drop, and the 10-year Treasury yield is back below 4%; this is good news for fixed-income investments on the margin, although for now we continue to favor a more conservative strategy in terms of credit risk and duration.

For equities, lower interest rates mean less pressure on valuations at a time when corporate visibility has been somewhat called into question following the Q3 2022 earnings reports, with more downward revisions to expected earnings for 2023. In this regard, while the recovery is likely to be stronger in the segments most sensitive to interest rates—the Nasdaq, technology, and consumer discretionary sectors— we continue to favor a more value-oriented strategy from a fundamental perspective.

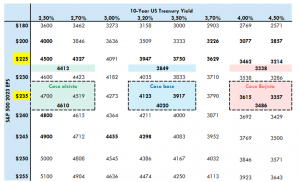

We are maintaining our fair value estimates for the S&P 500 at around 4,000 points

Lower interest rates mean less pressure on stock prices at a time when expected earnings have begun to be revised downward further

S&P 500 forecast for the end of 2022 based on estimated earnings per share for 2023, the 10-year Treasury yield, and a yield gap of 2.5%

Humberto Mora

Investment, Finance, and Business Manager; Stockbroker