As widely expected, the Fed raised the federal funds rate by 25 basis points to a current range of 4.5% to 4.75%. That move was another step toward greater moderation following the previous 50-basis-point increase and the four 75-basis-point increases at the four FOMC (Federal Open Market Committee) meetings prior to that.

In its statement, the “committee anticipates that further increases in the target range will be appropriate to achieve a monetary policy stance that is sufficiently restrictive to return inflation to 2% over time.” That was essentially a repetition of the language it has used in previous statements.

Signaling that the end of the cycle is approaching, the language regarding inflation in the statement was toned down, noting that inflation “has declined slightly,” reflecting growing confidence that inflation has peaked and is now more of a “thing of the past,” a message that was reinforced at the press conference, where Chair Powell spoke favorably of the ongoing or expected “disinflation”.

The Fed remains concerned about “the risk of doing too little,” while “the risk of tightening too much” seemed less of a concern, since it has tools that would work in that scenario.

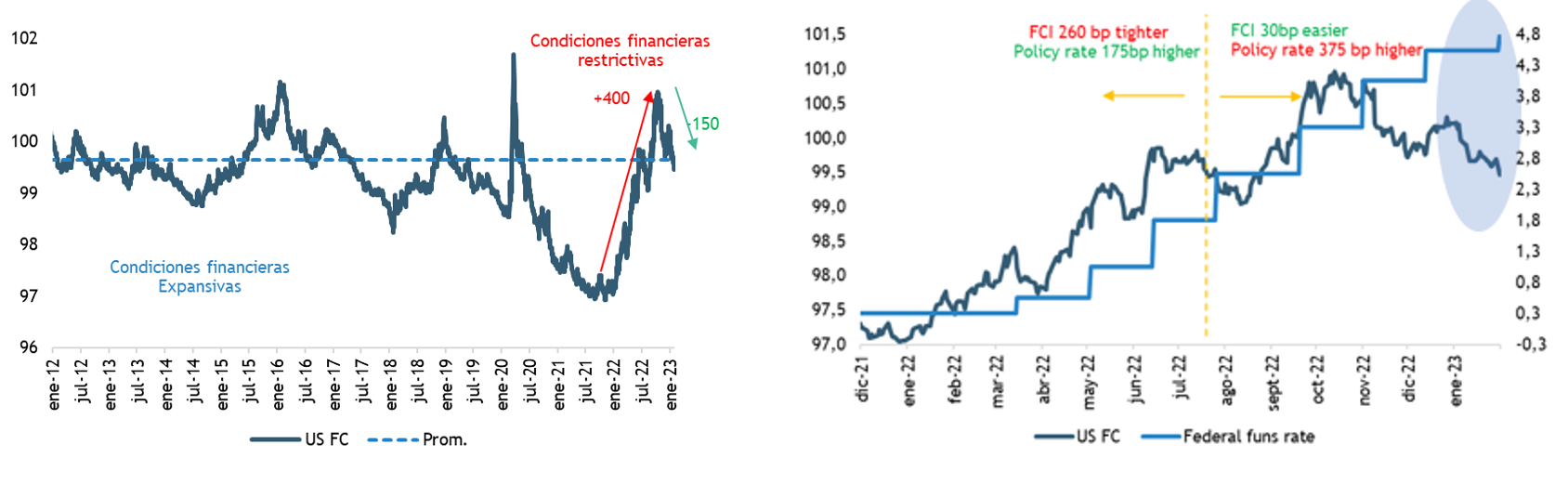

However, when asked about the recent easing of financial conditions, Powell did not seem overly concerned. In fact, he did not believe that conditions had changed much over the past six weeks and continues to believe that they have “tightened significantly” over the past year, a claim that is quite questionable when looking at any chart of financial conditions, which show that they remain at the same levels as in July even though the Fed has raised interest rates by an additional 375 basis points since then.

Financial conditions in the U.S. remain at the same levels as in July, even though the Fed has raised interest rates by an additional 350 basis points since then

Federal Funds Rate vs. Financial Conditions

View full-size chart

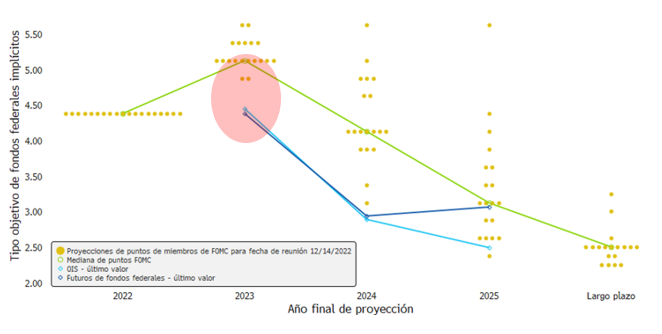

Similarly, he was not concerned about the divergence between the dot plots* and market prices (interest rate forwards), saying that it reflected a “difference in perspective” and, more importantly, that the market has a more benign outlook on inflation than the Fed.

On this point, we believe that what could ultimately tip the scales and dissuade the market from pricing in rate cuts in the second half of this year is the continued strength of the labor market, which is still classified as tight.

The markets are not only pricing in a more moderate pace of rate hikes by the Fed, but also a lower terminal rate and, in fact, a shift toward rate cuts starting in the second half of 2023.

Federal Funds Rate Dot Plot vs. the Market

View full-size chart

Looking ahead, we expect any further increases to be in increments of 25 basis points; but the Fed will likely have more work to do to convince the markets that rate cuts are unlikely by the end of the year, unless there is a more significant deterioration in the economy and/or the labor market.

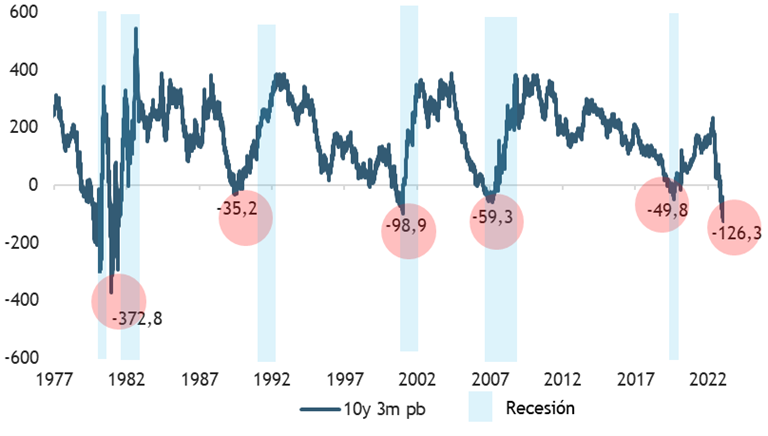

For now, the U.S. economy remains in the midst of a sharp slowdown in the consumer goods and housing markets, but increased spending on services is offsetting this for now. A recession remains a risk given the signals coming from a deeply inverted yield curve. However, the key point to remember is that the stock market is a leading indicator par excellence and, as is often the case, should lead the economy as it eventually stabilizes. That’s not to say the bear market is over, but rather that much of the “economic pain” and inflation already experienced has been reflected in the market correction that has been underway over the past 12 months.

An inverted yield curve has preceded every recession since the 1970s

Pending the 10y3m curve

As expected, Powell’s “more moderate” tone was well received by the markets. That said, when it comes to equities, we continue to believe that the upside is limited (especially in the U.S.), given unattractive valuations and increased risk to corporate earnings outlooks. Where we do see a diminishing downside is in the bond market (see more here).