According to GFK's report at the end of the fourth quarter of 2024, the real estate market for new housing in the Metropolitan Region showed a sharp contraction in the start of new projects. During the year, there were only 109 projects that started their sales phase, the lowest figure since 2009 and 22% lower than in 2023, when 140 projects were recorded at this stage.

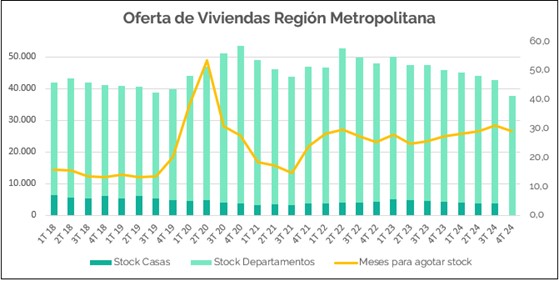

On the supply side, we see that the stock at the end of 2024 is 41,744 units (or 211.7 million UF), 2.3% lower than the previous quarter, and 8.8% lower than the same period of 2023.

Analyzing the breakdown, we can see that the number of departments in stock is 37,766 units, which are mostly concentrated in the districts of Santiago, La Florida and Ñuñoa. In the housing market, the available units correspond to 3,752, mostly concentrated in Colina, Puente Alto and Lampa.

By delivery period, both in houses and apartments, the highest percentage of the supply is with immediate delivery, representing 26.2% of the total number of apartments and 32.6% of the total number of houses available.

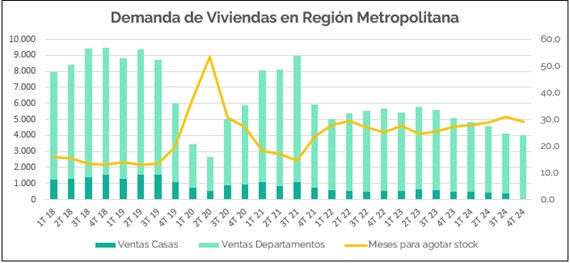

Regarding sales, in the last quarter of 2024, 4,368 units (20.6 million UF) were marketed, 5.7% more than in the previous quarter, but 13.6% less than in the same period of 2023.

Now, going to detail, in 4Q 2024, 4,035 apartments and 333 houses were sold. In the case of apartments, the districts with the highest volume sold were Santiago, La Florida and Ñuñoa, while in the housing market, they were concentrated in San Bernardo, Puente Alto and Lampa. By delivery term, immediate delivery has the highest percentage at the quarterly level, both in apartments and houses, with 37.1% and 42.9% of total sales, respectively.

The average speed to market per project was 1.5 units per month (1.7 apartments and 0.6 houses), so the months to deplete stock were 1.5 units per month (1.7 apartments and 0.6 houses). stock the total market (28 months for apartments and 36 months for houses).

In summary, we can see that during 2024 the stock of new housing starts in the Metropolitan Region contracted, moving away from its historical maximum, but still at high levels, above the average of the last decade. This decrease is due to the low inflow of new projects -the lowest in 15 years-. This decrease is due to the low number of new projects -the lowest in 15 years-, reflecting the low interest of real estate companies in developing new initiatives due to the multiple difficulties faced by the sector.

On the demand side, new home sales recorded an 18% drop compared to 2023, reaching the lowest level since 2020. This is largely explained by high real property prices, which have shown little variation in the period, and by restrictions in access to mortgage financing, despite the drop in interest rates on loans observed in recent months.

In view of this scenario, the government has decided to intervene in access to financing by means of the Dividend Subsidy Bill, announced on Tuesdayannounced last Tuesday, January 29. This initiative, promoted by the Ministries of Finance and Housing and Urban Development, in conjunction with the Chilean Chamber of Construction and the Association of Banks and Financial Institutions, proposes a subsidy to mortgage loan rates of up to 60 basis points for new homes of UF 4,000 maximum. In addition, together with the extension of the State Guarantee Fund (FOGAES) until the end of 2025, it seeks to stimulate the real estate market, encouraging demand and helping to reduce the over-supply of housing. stock not only in the Metropolitan Region, but also throughout the country.

Sebastian Mahave

Senior Real Estate Analyst Fynsa AGF