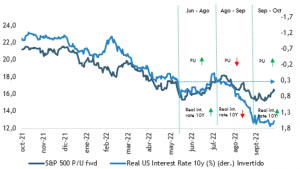

The stock markets remain caught in a delicate balance between interest rates, valuations, and corporate earnings. And if you look at the attached charts, the market has essentially gone nowhere since June, with downward pressure on valuations—due to higher interest rates—being partially offset by the resilience of corporate earnings.

Stock markets remain caught in a delicate balance between interest rates, valuations, and corporate earnings

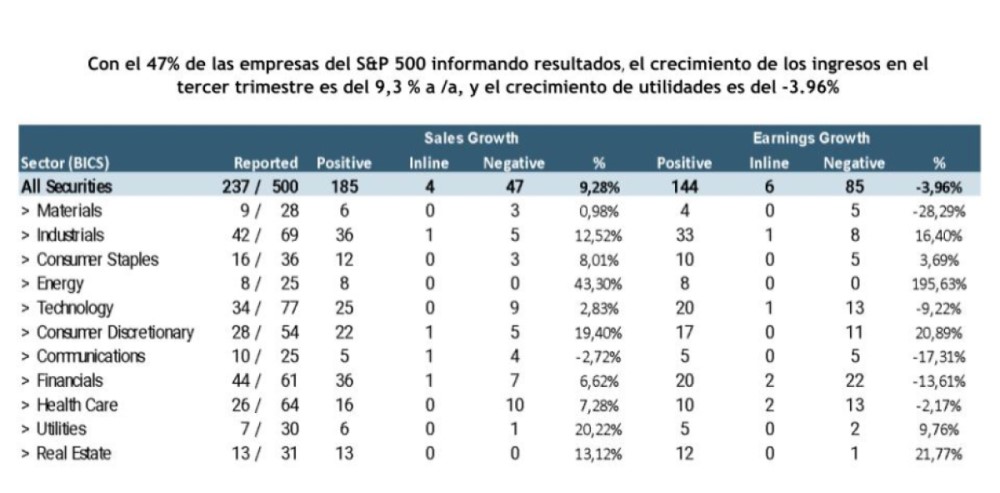

Most recently, the rise in stock prices may reflect a certain rotation toward value sectors and anticipation of a future “Fed pivot,” which has led to some expansion in valuations, but has very little to do with corporate earnings for Q3 2022, which, until last week, had mostly been beating expectations, but which this week have delivered major negative surprises, especially among large technology, communications, and consumer discretionary companies. Here are some related figures:

These tech companies thrived during the pandemic as life and work shifted further online, boosting sales and encouraging companies that were already growing rapidly to accelerate hiring and investment. Now, one by one, the drivers of that growth are being called into question. Sales of personal computers and other devices are falling. Consumers, hit hard by inflation, are cutting back on spending, while companies are tightening their budgets for everything from digital advertising to IT services.

We have identified two issues underlying this trend in corporate earnings: (1) The continued weight of these sectors in the overall index (technology, consumer discretionary, and communications together account for nearly half of the S&P 500) and that (2) with the exception of communications, which is trading at a discount to its long-term averages, technology and consumer discretionary are still trading at a 20% premium as measured by forward P/E multiples.

Thus, as the macroeconomic environment becomes much more challenging in the coming quarters, it seems unlikely that we will see further support from corporate earnings, leaving the market entirely dependent on a potential “policy pivot,” which no longer has much to do with a pause, much less potential interest rate cuts, but rather with a more gradual pace of rate hikes.

In this regard, just as was the case this week with the BoC (Bank of Canada) and the ECB (European Central Bank), which, beyond continuing to raise interest rates, adopted a rather moderate tone, the Fed in the U.S. also appears interested in slowing the pace of tightening following unusually large interest rate hikes, given the focus on financial risks and lagging indicators of inflation, although disappointing inflation data could quickly dash those hopes. If the economy remains out of recession in the coming months—which we believe is likely—this would increase the risk of a more gradual Fed tightening cycle, but one that extends into 2023.