| A couple of weeks ago, we argued that the market rally from June’s lows had gone too far and that unless the “peak inflation” narrative is confirmed by both the data and a moderate pivot by the Fed, We believed that the risk of another rate shock and fears of a recession could once again weigh on risk appetite. See HERE

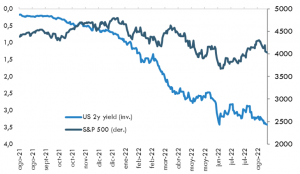

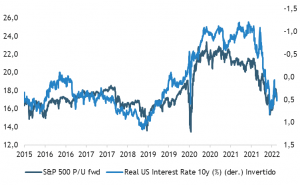

Market hopes were pinned on Powell’s message at Jackson Hole reaffirming a moderate shift in monetary policy, but none of that happened. The underlying logic behind expectations of a “Fed pivot” was based on the assumption that the focus of monetary policy would shift from inflation to growth, but in his speech, the Fed chair promised to do whatever it takes to protect the economy from excessively high inflation. “Bringing inflation down will likely require a sustained period of below-trend growth,”, Powell said. “In addition, it is very likely that labor market conditions will weaken somewhat,” which otherwise continues to be characterized as “particularly strong” and “clearly out of balance.” On the other hand, demand for workers substantially exceeded supply, leading to rapid wage increases that are incompatible with the Fed’s 2% inflation target. But what probably drew the most attention in his speech was when Powell noted that the pain that businesses and households will have to endure is preferable to the Fed failing to restore price stability now and having to inflict even more damage on the economy later. Incidentally, we share that assessment, but it also carries an implicit message that is not very friendly toward assets: “Don’t expect the Fed to prop up the market this time,” at least not without first experiencing “greater pain” (the S&P 500 has already lost nearly 7% since Jackson Hole). Without a “pivot” in monetary policy, economic activity will inevitably continue to slow down, given that the Fed’s goal is to reduce inflation by slowing growth below its potential, thereby increasing the risks of a recession. What does all this mean in terms of asset management? So far, most of the market’s weakness has been due to the Fed and tighter financial conditions. Higher interest rates have put pressure on equity valuations, especially in sectors with higher implied growth, and have also led to sharp losses in fixed-income markets, particularly for bonds with longer durations. We still see some downside risk in this regard, as the Fed’s goal would be to bring policy rates closer to 4%, a move that is not yet fully priced into asset prices. In the case of equities, the rally leading up to Jackson Hole pushed valuations to unrealistic levels. Although aggregate P/E multiples have fallen again, they do not appear particularly attractive by historical standards (average levels), and there is still some divergence from interest rate levels. (See Charts No. 1 and No. 2) Charts No. 1 and No. 2. S&P 500: We still see valuations as a downside given the higher interest rates.

But as growth prospects begin to weaken, the focus should shift from interest rates to corporate earnings, especially now that we are entering the seasonally weakest time of the year for earnings revisions, and inflation is beginning to put even more pressure on margins and demand—which should also put pressure on corporate spreads, which have remained relatively resilient so far. (See Charts No. 3 and No. 4)

Charts No. 3 and No. 4. S&P 500: Corporate earnings remain positive but are losing momentum. Seasonal trends are somewhat unfavorable.

Source: Fynsa Estrategia, Morgan StanleyThe current environment calls for a much more selective asset allocation, while still maintaining some overweight position in equities, given that, historically, stocks have outperformed other asset classes during periods of inflation. We recommend maintaining portfolios that are well diversified across regions, styles, and sectors, with a greater overweight in value sectors, particularly energy. Fixed-income portfolios should consist of very high-quality (IG) bonds with average duration. And finally, consider holding some cash, which is no longer a significant drag on a portfolio’s current returns. Here are some figures on this: Yields on 6-month U.S. Treasury bills (3.3%) are the highest since late 2007 and offer 170 basis points more than S&P 500 dividends (currently at 1.6%), 18 basis points more than 10-year U.S. Treasury bonds (currently at 3.15%), and only 60 basis points less than the U.S. Aggregate Bond Index (3.91% YTM).

|