Our biggest question mark is that a soft landing scenario is already largely built into prices and we don't see much reason for risk assets to continue to rise, amid higher rates and still hawkish language from several FOMC members.

Share

Qué duda cabe, los mercados vienen operando en los últimos meses en modo “soft landing”, que básicamente es un escenario que podemos resumir como:

Los indicadores líderes se estabilizan antes de mejorar en la primera mitad del año.

Las preocupaciones sobre una recesión mundial resultan demasiado pesimistas, ya que los mercados laborales siguen siendo sólidos.

La inflación subyacente avanza hacia los objetivos de los bancos centrales a medida que disminuyen los precios de la energía y los alimentos y los efectos de base reducen las comparaciones interanuales.

China se recupera a medida que se levantan las restricciones de COVID, se intensifica la política (monetaria y fiscal) y se dejan de lado los desafíos del mercado inmobiliario.

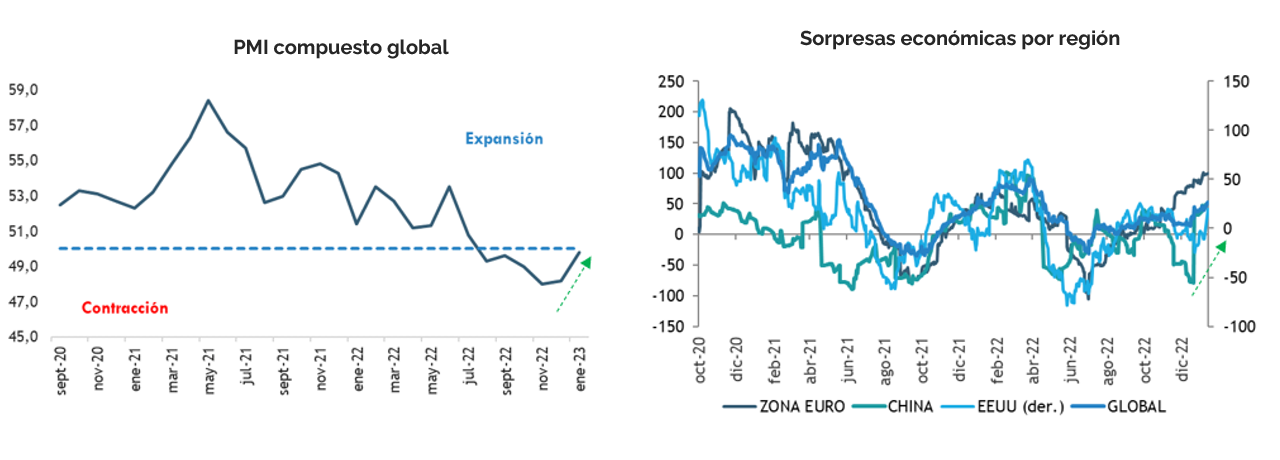

Los datos recientes respaldan una disminución de los riesgos de recesión a corto plazo, que son visibles, por ejemplo, a través de las encuestas de PMIs, con una mejora en los pedidos complementada por un aumento del empleo y una caída de la inflación, así también en que los datos económicos en las distintas regiones han estado sorprendiendo en general al alza.

En este escenario, la respuesta de política se caracteriza por bancos centrales que adoptan un tono menos agresivo y el mercado adelanta el peak esperado en las tasas de política. (VER MÁS)

Por cierto, este es un escenario positivo para los activos de riesgo:

Propicia un repunte del mercado accionario, donde los activos emergentes funcionan particularmente bien y los activos ex US superan a los activos US.

El posicionamiento es más cíclico y los sectores de crecimiento superan a los sectores de valor.

Los spreads corporativos se comprimen y la deuda HY supera a IG.

El dólar se debilita y los commodities se aprecian.

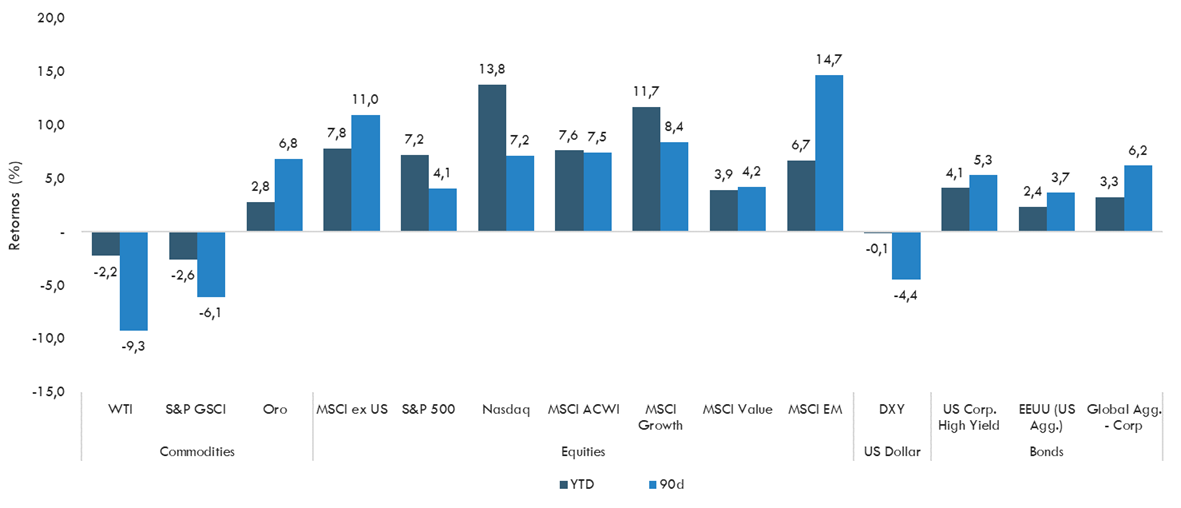

Y si observan el desempeño de los distintos mercados en los últimos 3 meses y en lo que va de 2023, es justamente lo que hemos obtenido, con la notable excepción de las materias primas, que han sorprendido a la baja.

Desempeño distintas clases de activos 3m; YTD

Fuente: Fynsa Estrategia; Bloomberg. Datos al 08 de febrero de 2023

Hasta ahora parece una muy buena historia para contar, pero permítanme hacer algunos contrapuntos:

El buen desempeño de los mercados se sustenta casi exclusivamente (el resto es la reapertura de China), en la expectativa de una “desaceleración sustancial” de la inflación en adelante y por tanto una postura más acomodaticia de tasas de interés, así también en que todo eso se logra dentro de un contexto económico de “soft landing”.

El nuevo concepto de moda en los mercados es el de “desinflación”, incluso algunos hablan de “immaculate desinflation”, después de que el presidente Jerome Powell en la conferencia de prensa post comunicado de política monetaria de este mes, sugiriera un ligero cambio en la función de reacción de la Fed, que parecía volverse más optimista sobre un aterrizaje suave (solf landing) y una disminución de la inflación sin dolor en el mercado laboral.

Estos mismos dichos fueron reafirmados en una entrevista de Powell en el Club Económico de Washington durante esta semana, donde afirmó claramente que cree que el proceso de desinflación ha comenzado, pero que será un largo camino por recorrer, que no será suave ni exento de riesgos y que es probable que se necesiten más aumentos en las tasas de interés, advirtiendo además que el peak de la tasa de fondos federales podría ser mayor, particularmente si el mercado laboral se mantiene fuerte.

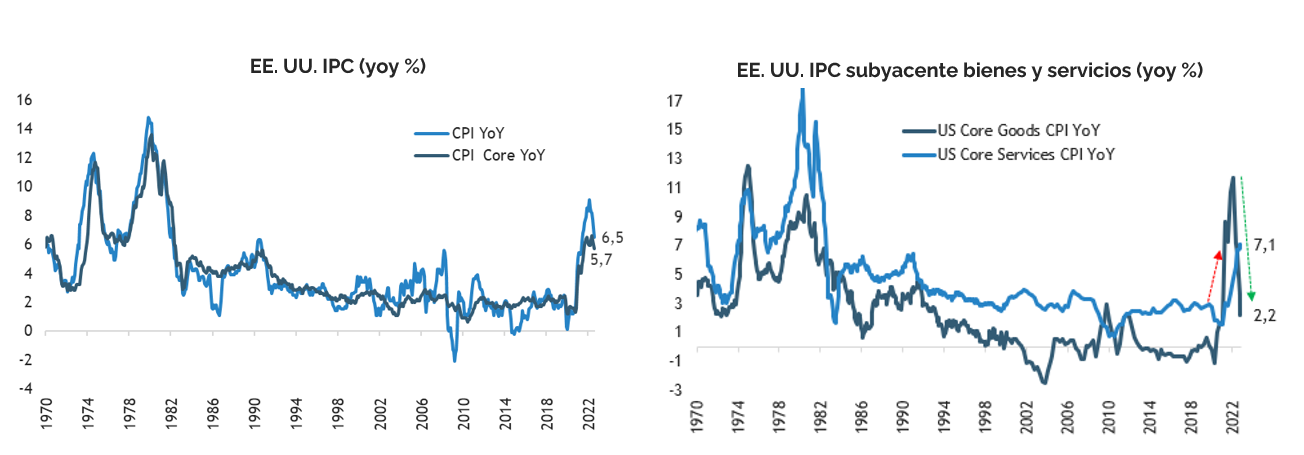

También enfatizó que el proceso desinflacionario es solo claro en los precios de los bienes, que son solo el 25% del IPC subyacente, mientras que el proceso aún no se muestra en la inflación de los servicios. Dijo que sigue esperando que la inflación de los servicios de vivienda se desacelerará “en la segunda mitad de este año” y que la inflación de los servicios que no son de vivienda se enfriará cuando se enfríe el crecimiento de los salarios. Además, dijo que la inflación de los servicios que no son de vivienda (algo más del 50% de la inflación subyacente) es su “mayor preocupación” en lo que respecta a las perspectivas de inflación.

En efecto, si bien la inflación interanual viene moderándose, la inflación subyacente se mantiene alta y la fortaleza de la inflación de servicios plantea un desafío mayor para la FED. Una trayectoria de inflación más rígida en los servicios conjuntamente con la fortaleza del mercado laboral también dificultará que la Fed reduzca las tasas y así evitar una recesión.

Source: Fynsa Estrategia; Bloomberg

En resumidas cuentas, parece que los mercados “solo escuchan lo que les conviene” y han decidido “comprarse la desinflación” sin mayores cuestionamientos.

Pero convengamos que lo que pretende hacer la FED es un trabajo muy difícil: desacelerar la economía a través de aumentos de las tasas de interés y evitar que caigamos en una recesión, que tal vez lo logre. Pero nuestro mayor cuestionamiento es que un escenario de soft landing ya está en buena medida incorporado en los precios y no vemos muchas razones para que los activos de riesgo sigan subiendo en medio de tasas más altas y el lenguaje todavía agresivo de varios miembros del FOMC durante esta semana.

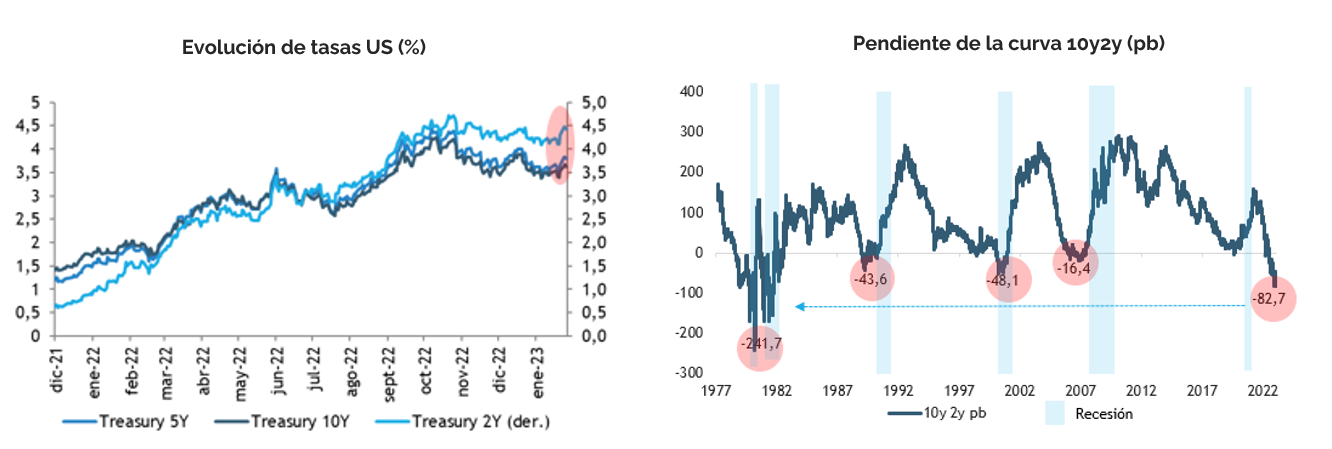

En efecto, las acciones han seguido subiendo cuando las tasas de interés en la parte corta de la curva han subido cerca de 40 puntos base en los últimos 7 días (el rendimiento de la nota a dos años alcanzó el 4,5%) y cerca de 30 puntos base en la parte larga de la curva, lo que ha acentuado la inversión de la curva al nivel más amplio desde la década del 80.

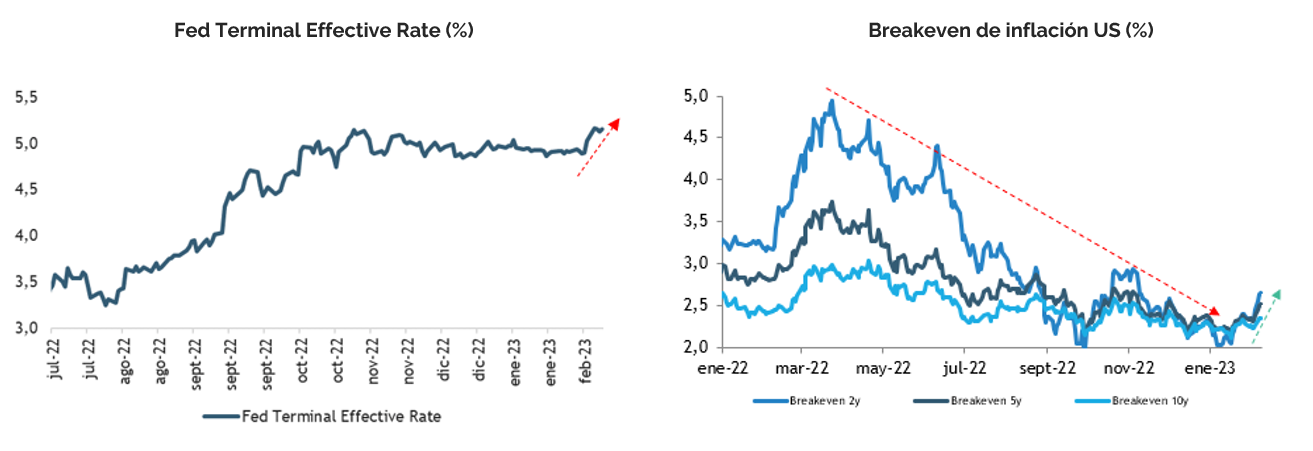

Es más, la tasa terminal de fondos federales ya se empina sobre el 5% y los operadores de opciones han estado acumulando apuestas con un objetivo del 6%.

Y las expectativas de inflación implícitas en el mercado de bonos están comenzando a recuperarse nuevamente.

Source: Fynsa Estrategia; Bloomberg

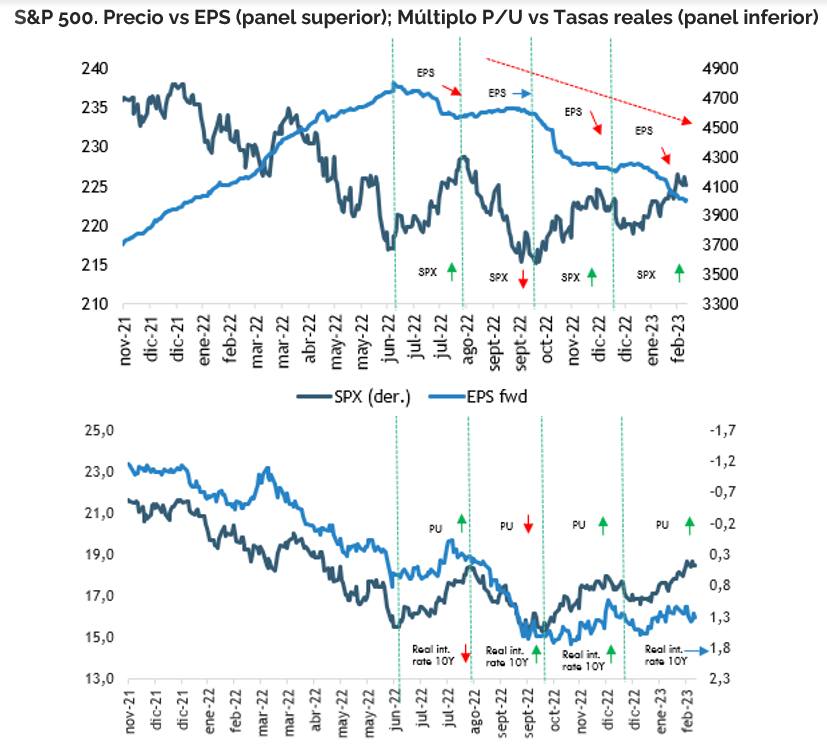

Finalmente, ¿cuánto puede sostenerse la recuperación de la renta variable, con revisiones más a la baja en las utilidades esperadas y mayores tasas de interés que ponen presión sobre valorizaciones que no son particularmente atractivas?

Source: Fynsa Estrategia; Bloomberg

*Immaculate Disinflation: Se refiere a la idea de que la inflación puede reducirse de alguna manera sin un impacto material en la demanda y, por lo tanto, en el crecimiento del PIB. O bien que el crecimiento de los precios se desacelera a la normalidad, pero sin daños colaterales en el mercado laboral

Humberto Mora

Investment, Finance, and Business Manager; Stockbroker