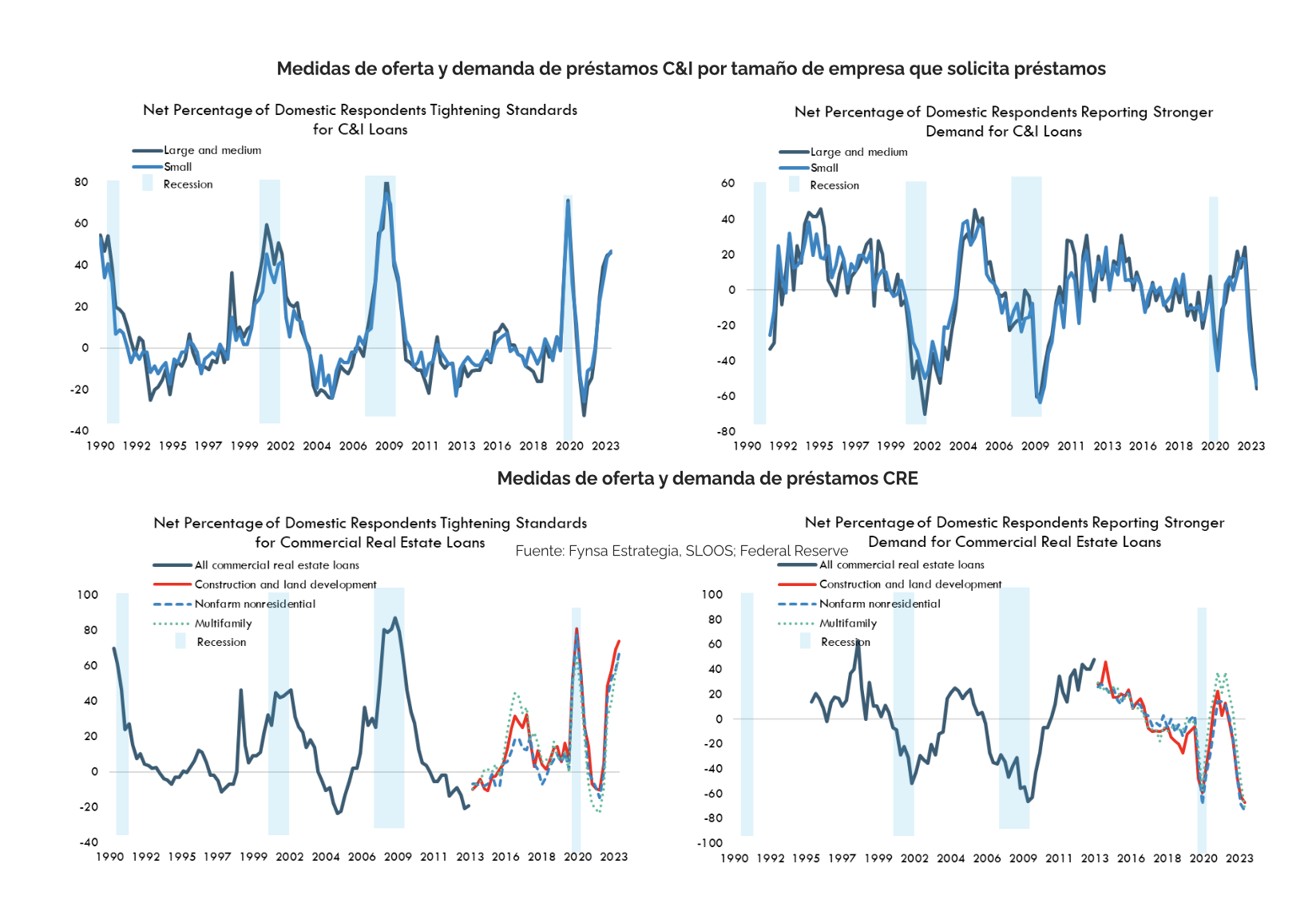

The U.S. Federal Reserve's Senior Loan Officer Opinion Survey (SLOOS) conducted in April (see more) provides information on bank lending activity during the first quarter of this year. According to the results, credit standards tightened on a net basis, and demand for commercial and industrial loans, as well as commercial real estate loans, weakened for businesses of all sizes.

With regard to households, banks reported stricter standards across all categories of consumer loans. In addition, demand for auto loans and other consumer loans was weaker, while demand for credit card loans remained largely unchanged.

The banks cited various reasons for this tightening of standards and the weakening of demand. These include a less favorable or more uncertain economic outlook, reduced risk tolerance, a decline in the value of collateral, and concerns about funding costs and banks’ liquidity positions.

Although, overall, the report does not show a significant deterioration compared to the previous report (since credit standards were already at near-record levels), the details are slightly worse (for example, in the multifamily residential and CRE [Commercial Real Estate] categories).

In particular, demand for C&I (commercial and industrial) loans from large and medium-sized companies weakened considerably in the first quarter. On a net basis, 56% of banks reported weaker demand for C&I loans from large and medium-sized firms in the market, compared with 31% in the previous survey. Fifty-three percent of banks reported weaker demand for commercial and industrial loans from small businesses, compared with 42% in the previous quarter.

As for lending standards for commercial real estate (CRE) loans, they tightened in the first quarter. On a net basis, 74% (+5 pp) of banks reported stricter credit standards for construction and real estate development loans, while 65% (+8 pp) reported stricter credit standards for loans secured by multifamily residential properties. In addition, the number of banks reporting stricter standards for loans secured by nonresidential, nonagricultural properties rose to 67% (+9 pp).

Finally, regarding the special questions, none of the banks expected their credit standards for C&I loans (and most other types of loans) to ease for the remainder of 2023, while 33% expected them to tighten further, suggesting that credit standards may continue to tighten.

At the most recent monetary policy meeting in the U.S., the Fed made it clear that it now views the credit crunch as a reality, which adds to the likelihood of a pause in rate hikes at upcoming meetings. (read more)

Recent tensions in the banking sector are leading to stricter credit standards. Although banks’ liquidity problems (due to deposit outflows) could slow the rise in interest rates, an “accommodative” monetary policy is less likely to support the markets if financial conditions tighten.

The risk going forward is that the uncertainty caused by deposit movements will make banks even more cautious about lending. This risk is potentially exacerbated by the fact that small and medium-sized banks play a very important role in U.S. bank lending. To provide some context, small and medium-sized banks in the U.S. account for about 80% of total commercial real estate loans (see more)