Last week, we argued that the “more positive” news on U.S. inflation would reignite trading based on a “policy pivot” on the understanding that lower interest rate pressures mean less pressure on valuations at a time when corporate visibility has been somewhat called into question following the Q3 2022 results, with more downward revisions to expected earnings for 2023 (See HERE)

We also reaffirm our projections that U.S. equities were once again approaching levels closer to fair value—which could, of course, be overvalued—but this limits the potential for further recovery, given that valuations—both absolute and relative to bonds—are not particularly attractive.

The S&P 500 is trading at 17.3x future earnings (+1 standard deviation above its long-term averages), while the premium offered by stocks over bonds has narrowed to 200 basis points—100 basis points below its long-term averages and the lowest level in 15 years.

The current recovery, just as in July and August, is driven by the hope that U.S. inflation “has peaked” and the view that the Federal Reserve will soon share this assessment. Past experience has shown this to be more of a good opportunity to sell and reassess risk exposure, and while we acknowledge the progress made in terms of monetary tightening and lower inflationary pressures on the margin, we cannot rule out the possibility that history will repeat itself.

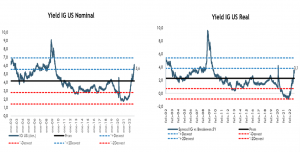

That said, where we do see things starting to look more attractive is in the bond market. U.S. investment-grade (IG) debt currently offers a yield of 5.5% (it reached 6.0% just a few weeks ago), the highest level in 15 years; when adjusted for expected medium-term inflation, this translates to a real yield of 3.0%.

Look at what happens when you compare this to the implied yield that stocks offer today. It’s practically the same yield! In other words, the spread between the implied yield offered by stocks (the inverse of the P/E ratio) and the yield offered by investment-grade debt is practically zero—the lowest level since before the financial crisis. In the deflationary environment prior to the pandemic, stocks had virtually no competition; “today, they’re starting to face some competition,” and while stocks have a relative advantage over bonds in a more inflationary environment, as inflationary pressures begin to ease, an intermediate step in risk-taking should be taken through investment-grade fixed income, especially for moderate investment profiles.