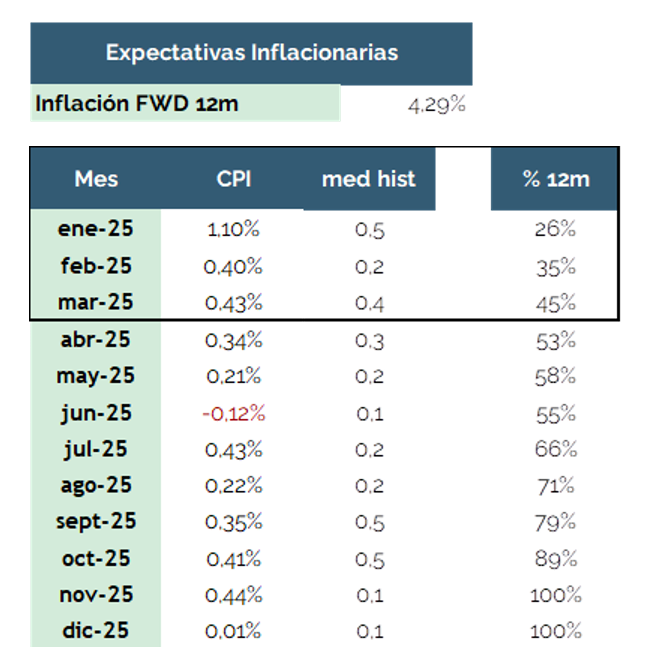

At its most recent meeting, the Central Bank of Chile decided to maintain the Monetary Policy Rate (MPR) at 5.0%. to maintain the Monetary Policy Rate (TPM) at 5.0%, meeting market expectations.in line with market expectations. This decision reflects a cautious stance, given that, although inflation has shown signs of moderation, it is still above the target range, remains above the target range.. The most recent projections of the BCCh's most recent projections put inflation at 3.6% for the end of 2025while the swaps market swaps place it at around 4.3%, reflecting still latent inflationary risks.reflecting still latent inflationary risks.

The CPI for January (+1.1%) CPI for January (+1.1%), higher than expected (0.9%), reinforces this view.higher than expected (0.9%), reinforces this view. Moreover, 12-month inflation expectations have risen from 3.6% to 4.3% so far this year. 3.6% to 4.3% so far this year, reflecting a higher inflationary impact.reflecting a higher short-term inflationary impact. Much of the projected inflation for 2025 will be concentrated in the first quarter of the year, implying that a higher inflationary impact in the short term is expected.which means that UF-indexed UF-indexed instruments continue to be the best option to face this inflationary environment..

Now, the most recent most recent inflation figure, corresponding to February, stood atstood at 0,4%in line with market expectations. However, despite being in line with expectations, remains well above its historical average for the month.. On this occasion, 10 of the 13 divisions recorded increases, with leasing the product with the highest incidence in the the product with the highest incidence in the. Its variation of 1,1%in line with the previous month's CPI, reflects its "indexation" to the UF.indexation" to the UF. This trend should persist throughout the year and, in the coming months, it could even register increases higher than the variation of the UF.

High UF Exposure: A Key Factor

Given the current scenario, we consider it fundamental to maintain a strategy with a high indexation to the UF (ideally between 90-100%). high indexation to the UF (ideally between 90-100%), which allows forwhich allows:

Optimal Duration: Two to four years

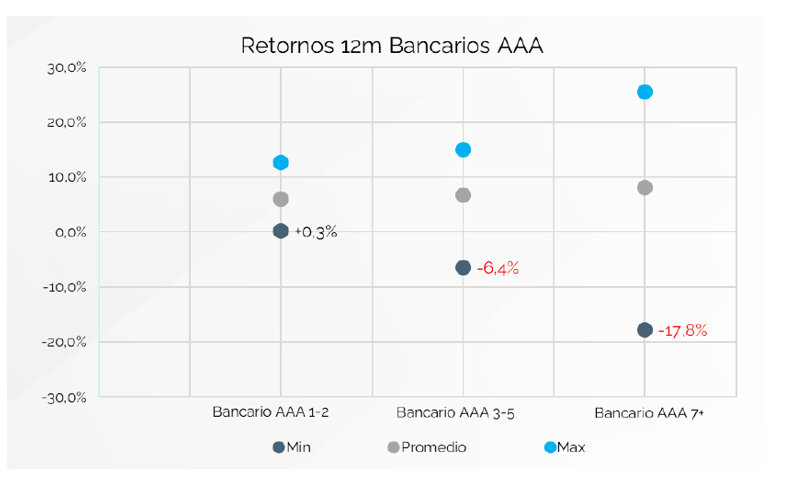

While the long end of the nominal curve shows attractive capital gain attractive capital gainswe believe that its high correlation with U.S. monetary high correlation to U.S. monetary policy and tight rate spreads versus U.S. Treasuries can add additional volatility. may add additional volatility. In this context, we recommend:

Seizing opportunities

The current environment of high high inflation in the short term and imminent tariff adjustments reinforces the convenience of to maintain strategies with high UF exposure and short durations.. With inflation more persistent than anticipated and breakevens breakevens still unanchored, this strategy remains the most remains the most efficient strategy for capturing returns, especially in the first half of 2025..

Therefore, for investors who still have exposure to term deposits or time deposits or money market, the transition to short-duration, high credit quality (AA+) UF-indexed strategies represents a clear risk-return decision in the current context. in the current context.

In this scenario, it is particularly important to have alternatives that combine inflation protection, a limited duration structure and attractive returns. inflation protection, a structure of limited durations and an attractive yield.. An example of this is Fynsa Deuda Chilewhich currently offers a YTM of UF+2.06% with a duration of 2.2 years, a flexible exposure to the UF (now UF+2.06%), a flexible exposure to the UFa flexible exposure to the UF (currently at 95%) and a portfolio with a predominance of bank bonds and DAP (81%), which reinforces its liquidity and stability.

In addition, it maintains a high high level of credit quality (AA+), differentiating itself by its balance between profitability and risk control.differentiated by its balance between profitability and risk control.

Compared to similar funds, it has achieved superior performance, with lower average duration, similar UF exposure and the same level of credit risk. shorter average duration, similar exposure to the UF and the same level of credit risk, making it an efficient option in the current market context.This makes it an efficient option in the current market environment.

For more information on FI Fynsa Deuda Chile, click on this link.

At the end of February:

Felipe de Solminihac

Investment Analyst Finance and Business Finance Brokerage Brokerage Firm

{kind=link}