Following the lower-than-expected inflation figures for October and November in the U.S., the market has been pricing in not only a slowdown in the pace of rate hikes by the Fed, but also a lower terminal rate and, quite simply, a “shift” toward rate cuts starting in the second half of 2023.

This contrasts with the intentions of the Fed itself and other central banks, which call for higher terminal rates that remain at elevated levels at least through all of 2023.

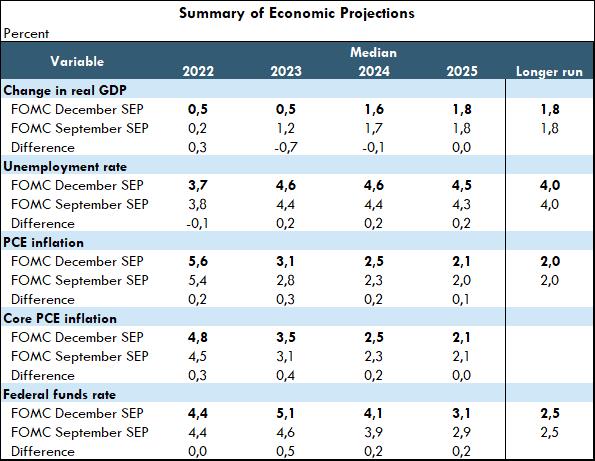

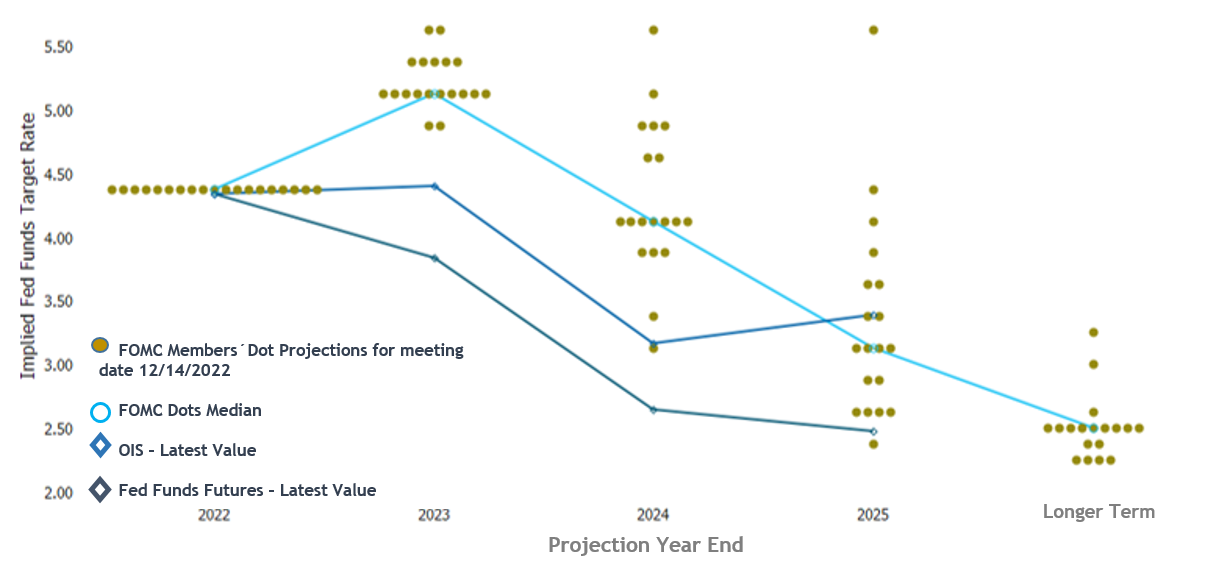

We saw evidence of this at this week’s FOMC meeting, which raised the target range for the federal funds rate by 50 basis points to 4.25%–4.5%, as widely expected, but with the views expressed in the SEP (Summary of Economic Projections) decidedly aggressive, as the Fed intends to raise rates further to slow growth and increase the unemployment rate, in order to address the prospect of higher inflation for a longer period. (see table). The median federal funds rate rose for 2023, from 4.6% to 5.1%, with only two FOMC members projecting a rate below 5.0% for 2023 (see chart). The median rates for 2024 and 2025 also rose by 20 basis points. The Committee still sees a first rate cut in 2024 as the most likely outcome.

At the same time, there was a significant decline in GDP in 2023 and 2024, reflecting the impact of higher interest rates, while the Committee also raised its projections for core PCE inflation and the unemployment rate in 2023 and 2024, meaning that participants still see upside risks to inflation and downside risks to growth, a combination that is not favorable for risk assets.

Click on the image to view it in its original size

Click on the image to view it in its original size

But it wasn't just the Fed that took a more aggressive stance. Although the ECB (European Central Bank) also slowed the pace of tightening with a rate hike of “only” 50 basis points to 2.0%, it foresees “significant future increases” to control inflation, while announcing a plan to reduce its balance sheet by EUR15 billion per month starting in March 2023. Meanwhile, the Bank of England also raised rates by 50 basis points to 3.5% and indicated that it will continue to respond “forcefully” if necessary.

Both central banks find themselves in an increasingly difficult situation, as the emerging recession and concerns about financial stability are balanced against ongoing wage pressures that risk entrenching inflation.

So then, with the major central banks “insensitive” to the sharply downward trend in economic activity… How long can the logic that bad economic news is good news for the market hold up? In our view, bad news is simply bad news, given that corporate visibility for next year is becoming increasingly uncertain, while the likelihood of policy errors and a recession is rising.