In July, when headlines about a possible recession in the U.S. were dominating the news following the economy’s contraction in the second quarter, we organized a webinar to discuss how likely it was at that time that the U.S. economy was on the brink of a recession (see HERE). Our conclusions at the time pointed to a low risk of recession (even though the market decline—primarily in equities—suggested a high probability), given that economic and corporate evidence was scarce, with consumers in good shape, a strong labor market, and robust corporate balance sheets.

Similarly, the evidence from the yield curve—a fairly effective predictor— did not provide any strong signs of an imminent risk of recession, with the curve remaining fairly flat and monetary policy far from restrictive.

Fast forward to today, and several things have changed

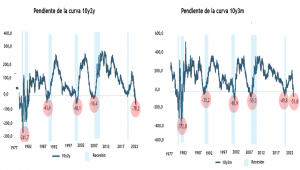

And as shown in the accompanying charts, a yield curve inversion has preceded every recession since the 1970s. So the question that follows is: Why should this time be any different?

Beyond the signals from the bond market, equity markets have not shown any significant stress, based on the assumption that the expected “moderation” in the pace of rate hikes by the Fed would be enough to avert a recession. This can also be explained by the lag between the yield curve inverting (remember that this is a warning sign, not a full-blown recession) and the economy actually entering a recession—a lag that averages around 12 months, during which time the markets may still be profitable.

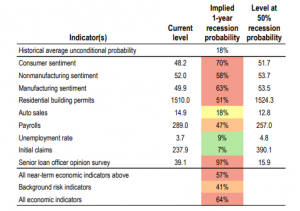

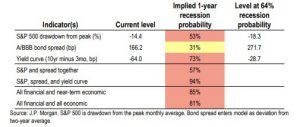

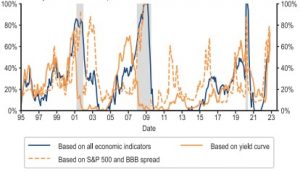

Statistics aside, what we want to highlight is that the risks of a recession have been increasing and that, unlike the situation in July—when the one-year probability of a recession in the U.S., as measured by various (economic and financial) models, pointed to a relatively low probability that, on average, did not exceed 30%— Those figures now exceed 50%, as shown in the attached tables from JPM.

Finally, most baseline scenarios for 2023 assume either a soft landing or a mild recession, based on the assumption that inflation will slow significantly and that the terminal policy rate will be in the range of 5.0%–5.25%—a scenario that is already largely priced in (therefore, anything much more restrictive than that would push the economy toward a hard landing). The problem is that, even in a soft-landing scenario, the potential upside for risky assets appears limited. In other words, the risk-return ratio from current levels is unattractive, which is one of the reasons why last week we recommended increasing exposure to fixed income and cash (short-term Treasuries yield over 4.5%) looking ahead to 2023, which, at first glance, appears quite uncertain (vsee HERE ).